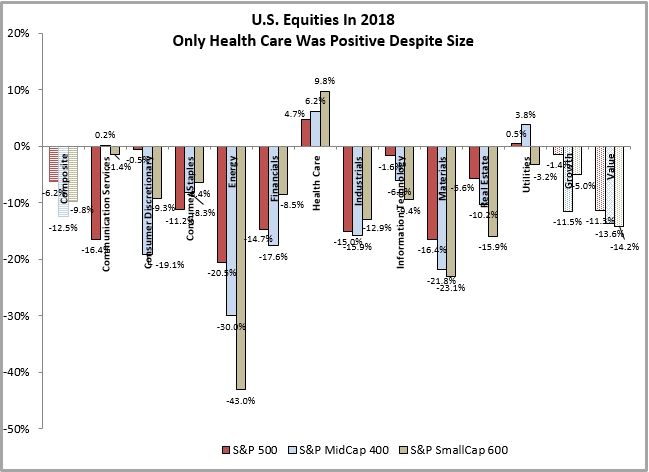

Equities have historically offered promising growth potential, but we have seen time and again how suddenly and severely the equity markets can be affected by events that are difficult to predict, and 2019 is not likely to be an exception. Losses can have a greater impact on portfolios than gains because the money remaining after the loss must work hard to recover just to break even.

Losses can happen more often than expected…

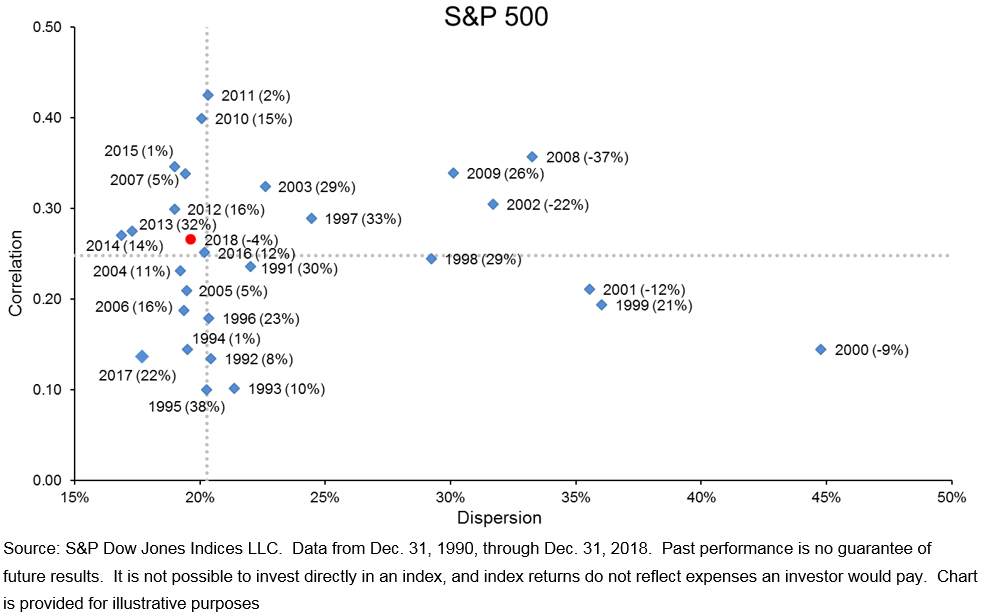

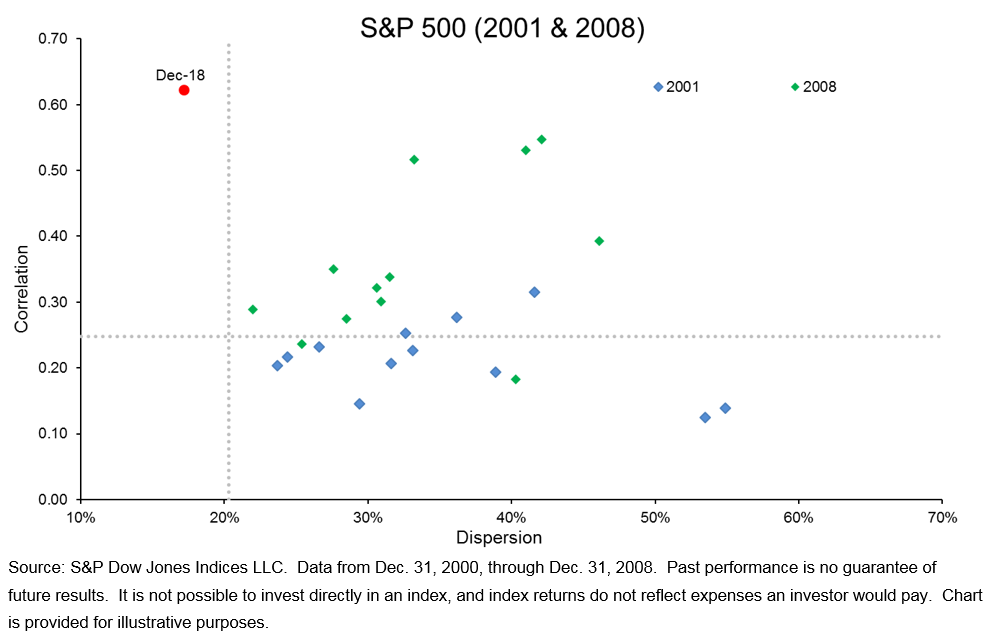

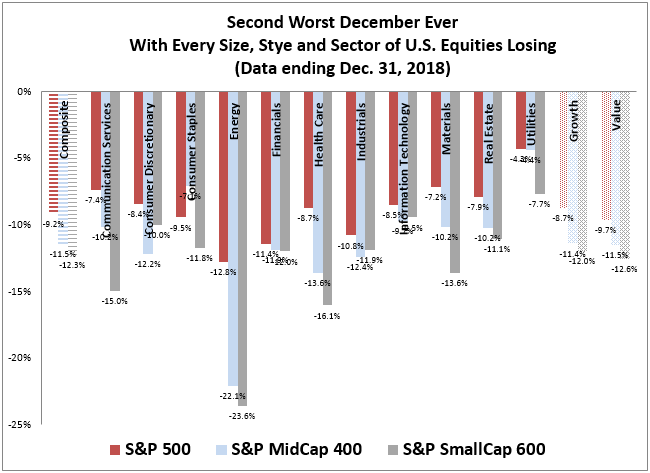

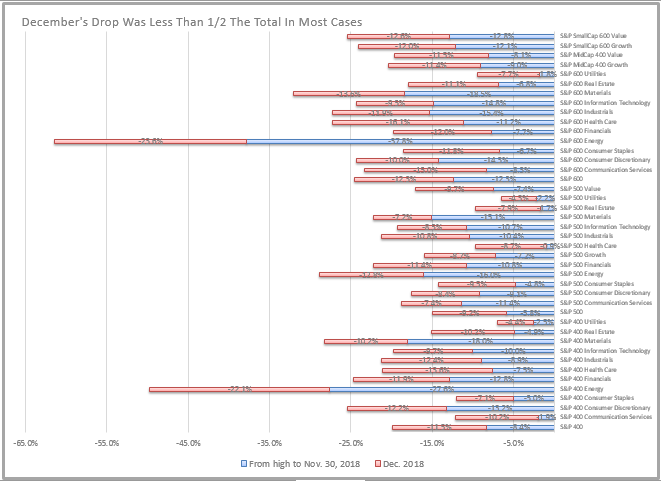

S&P 500 INDEX DRAWDOWNS[1]

…and it can take years to recover

YEARS TO RECOVER WITH ANNUAL RATE OF 5%[2]

Traditionally, investors have relied on diversifying equities with bonds, or market timing, to help minimize their risks from losses. But these strategies may be challenged in certain market environments.

60/40 may not be the answer

Many investors maintain a typical 40% allocation to fixed income investments to provide a counterbalance to equities during times of market volatility. However, bonds may decline at the same time as equities, as happened in October 2018, negating the expected counterbalance benefit. Fixed income may also be challenged when interest rates rise and lose purchasing power in an inflationary environment.

Being cautious does not mean being in cash

Investors who sell at the first sign of market downturns and wait on the sidelines in cash for the market to recover can miss out on top-performing days, which can have a big impact on returns. Further, like fixed coupon bonds, cash loses purchasing power in an inflationary environment.

A defensive options strategy can provide protection plus potential growth

An alternative approach that may help protect an investment involves the use of options—instruments that seek to provide a contractual level of certainty that other approaches lack.

A defensive “buffer protection” strategy, utilizing a combination of call and put options overlaid on an exposure to a given index, offers an alternative risk management solution. This type of strategy provides a “buffer” of protection against the first 10% of losses in the chosen index while capturing potential growth to a maximum capped gain (“cap”) over a period of approximately one year.

The cap level is set at the start of the period, such that the 10% downside protection is paid for by giving up potential returns above the cap. The returns of the strategy will be a function of the level of the index at the end of the period relative to its level at the start of the period.

Defensive buffer protection option strategies are typically implemented in structured notes and annuities with a single strategy of one-year maturity. However, the single strategy, one-year maturity creates acute timing risks, locking investors into one specific cap and buffer for an entire year. This prevents investors from capitalizing on new buffer levels or upside caps over the course of the year as the chosen index moves up or down.

The timing risks associated with a single strategy, one-year maturity can be mitigated through the same “laddering” technique used by bond investors. Equity investors seeking persistent defensive protection can build a laddered portfolio of defensive options strategies with maturities ranging from one to 12 months. In this manner, each month a defensive options strategy would mature and be rolled forward for another 12 months. This allows the downside protection and cap levels to reset and stay current to the prevailing market conditions for a portion of the investment, which can be an advantage in a rising or falling market environment.

The Cboe S&P 500 Buffer Protect Index (ticker: SPRO) employs such a strategy, using a laddered portfolio of 12 Buffer Protect Strategies designed to protect the first 10% of losses in the S&P 500 while capturing growth to a maximum capped gain.

[1] Calculated using Bloomberg data as the percentage negative return on a date from the highest level by the S&P Index prior to that date.

[2] Calculated using the formula TimeToRecovery = -Ln(1-OneTimeLoss)/Ln(1+RecoveryRate).

The posts on this blog are opinions, not advice. Please read our Disclaimers.