In case you missed them, we’ve compiled the most read blogs from the fourth quarter below.

Losing My Religion: Value in the USA

How have value indices performed and will value investing “work” in the future?

The Rieger Report: Munis Lead the Pack in the Final Lap

How did the municipal bond market perform in 2015?

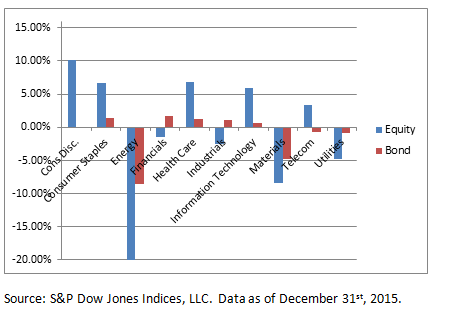

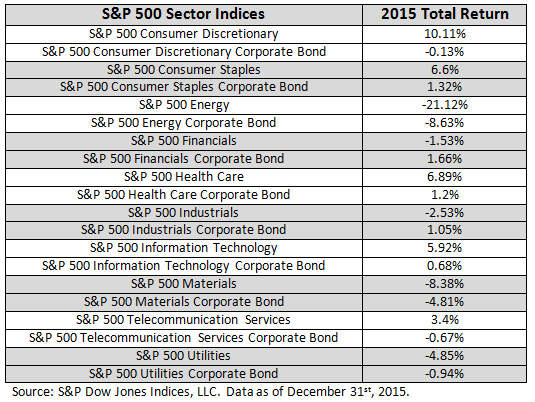

Energy Stocks and Bonds Say Oil May Have Bottomed

Has oil reached its bottom or is this just the market sentiment?

How Did European Active Managers Perform Over the Past 10 Years?

What were the results of the 2015 mid-year SPIVA® Europe Scorecard?

DJSI: A Journey Toward Sustainability and Beyond

How have the DJSI played a supporting role in leveraging sustainability as a key business driver for corporate success?

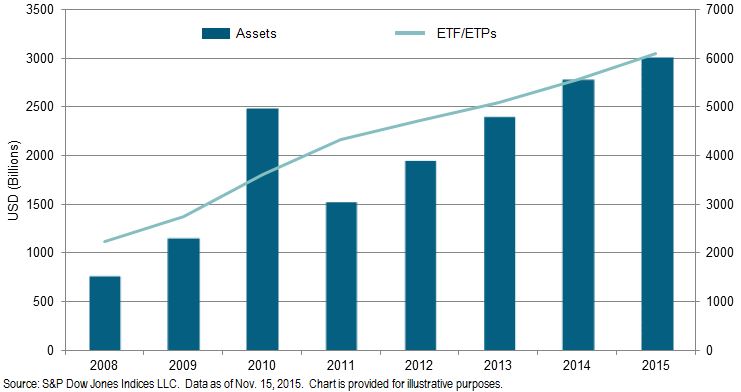

ETF Industry in India Over the Years

How has the ETF industry in India advanced over the years?