If simple is beautiful, then value investing is the equity market’s Helen of Troy – the faith that launched a thousand funds. If a company’s assets or profits are high in relation to its share price, it does not require much imagination to suppose that such company might offer attractive long-term investment prospects.

Value is also a “smart beta,” having been indicized – the concept of overweighting companies whose stock price is relatively cheap compared to their fundamentals underlies a swathe of indices, many of which have gained a broad traction with investors.

Value – the theory goes – works most of the time in the long term, and some of the time in the short term. As far as the U.S. markets are concerned, at the very least, an increasing degree of patience may be required.

But is “value” still working?

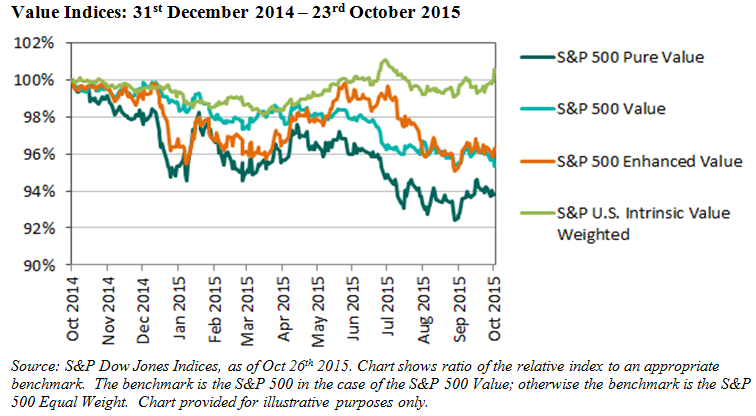

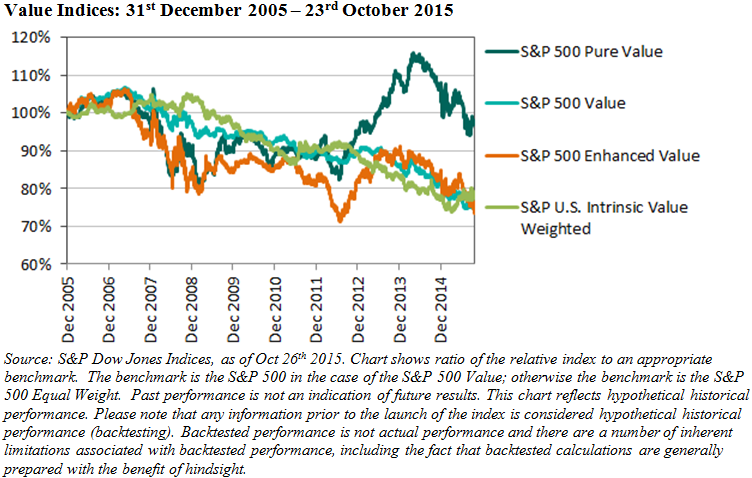

This is both an easy and a difficult question to answer. First, the easy answer. S&P Dow Jones Indices encodes value in several different U.S. based indices, reflecting the priorities of various different value investing schemes. We can examine the performance of these various value strategies, in comparison to an appropriate benchmark, over the long and short term. Such performance comparisons can also test the support for the various theses – such as the hope that value investments will weather crises more steadily – that are used in support of value investing as a style. The charts below show the relative performance of four value indices based on U.S. equities, over the past year and decade.

Note on reading the chart: if value is above 100%, the relevant index has outperformed its benchmark by a proportion equal to the chart level since the start date – if below, it has underperformed by that proportion. And note that the benchmarks for relative performance vary among value indices; as we’ve indicated previously in our research on value indices, an equal weight benchmark is a better indication of the value-added by the particular index methodology.

The result of such comparisons is conclusive: in both the short-term and long-term, value indices have been underperforming.

Of course, the harder question is whether value will “work” in the future. Value investing is typically supported, at the last, with the historical fact that – in the long, long term – value investing has outperformed. But there is always a disclaimer that the future may not reflect the past, and there is something different this time.

So, What’s New?

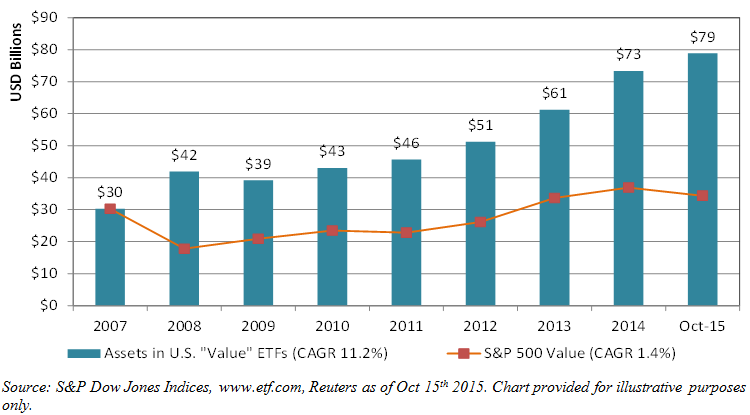

This difference is hinted already by the existence of our value indices: as a concept, value has become remarkably popular in recent times. A vast bank of academic literature has been published on the subject; systematic strategies have been encoded and funded to capture it. To give a sense of this growing popularity, the next chart shows the assets outstanding in U.S. listed ETFs that have the word “value” somewhere in their name; the growth in assets outpaces the investment growth (as proxied by the S&P 500 Value Index) by a close to a ten times multiple.

Growth in Assets in “Value” ETFs, Dec 2007 – Oct 2015

With so much energy directed to exploiting the excess returns available through value investing, maybe the only “value” stocks left are the value traps, those stocks whose prices are low as their prospects are determinedly poor. And, if the popularity of value strategies increases sufficiently to diminish future returns, investors may be better served focusing on other factors.

Like the topless towers of Ilium, investors can be burned by relying on the wrong factors. It remains to be seen whether the returns over previous decades attributed to a “value” premium are due a comeback. More broadly, the persistence of excess returns attributable to the kind of simple strategies that can be indicized – like value – are not guaranteed; careful analysis of persistence is a matter of great importance.

The posts on this blog are opinions, not advice. Please read our Disclaimers.