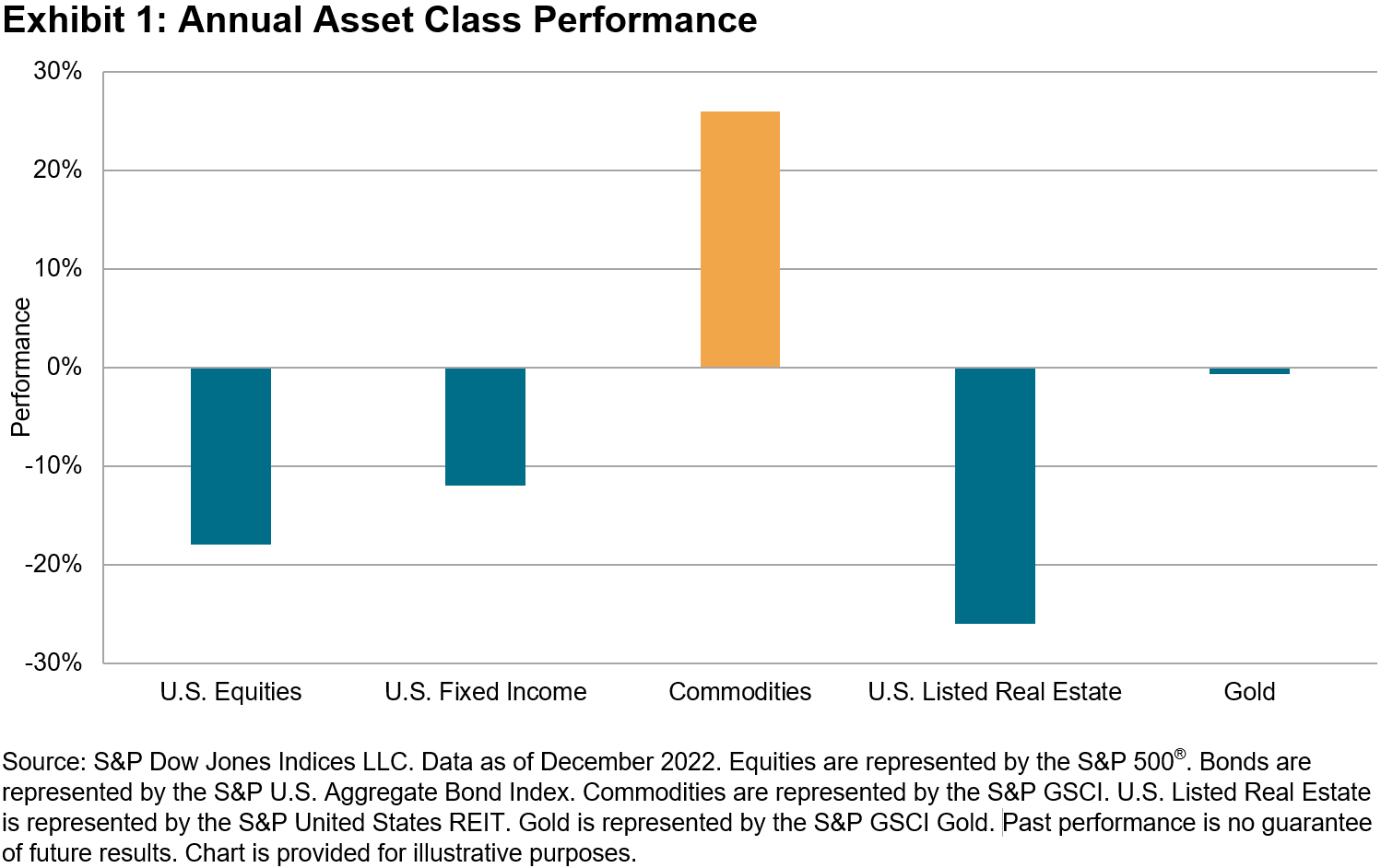

The market standard commodities benchmark, the S&P GSCI, performed admirably in 2022, rising 26%, outpacing other commodities indices and asset classes, as well as defying higher interest rates and growing fears of a prolonged global economic slowdown, while high inflation provided a solid backdrop for one of the most inflation-sensitive asset classes. Commodities has been the best-performing major asset class for each of the past two years.

It is not surprising that the energy complex enjoyed the strongest performance across commodities markets in 2022, with the S&P GSCI Petroleum rallying 44.6%. Oil prices surged in March as the Russia-Ukraine conflict disrupted global oil trade flows, but prices reversed in the second half of the year as recession risks multiplied. At the end of December, Russia delivered its long-awaited response to the Western price cap, announcing that it would ban the supply of oil and oil products for five months to countries that are party to the cap, starting on Feb. 1, 2023.

It was a wild ride for natural gas in 2022; the S&P GSCI Natural Gas ended the year up 19.8%, following a decline of 33.5% in December. Supply disruptions due to the Russia-Ukraine conflict sent global gas markets into override, but prices have more than halved since their mid-year highs, with stronger U.S. production and milder weather contributing to the reversal.

Despite starting the year with solid gains, industrial metals ended the year in negative territory, with the S&P GSCI Industrial Metals declining 7.6%. Inflation, COVID-19 lockdowns in top consumer China and coordinated interest rate rises hampered economic growth and weakened demand for industrial metals used in the power and construction industries, such as copper. 2022 will also be remembered as the year that the nickel market was rocked by a period of disorderly trade on the LME, leading to elevated periods of volatility and a slump in liquidity.

Performance across the agricultural markets was mixed. An ongoing drought in top soybean meal exporter Argentina and less competition from alternative oils such as sunflower and palm supported soybean prices, with the S&P GSCI Soybean ending the year up 28.9%. Wheat prices jumped to an all-time high following the Russian-Ukraine conflict (both major exporters of wheat). However, Black Sea exports picked up in the second half of the year, helped by a deal to create a safe shipping corridor for Ukrainian wheat and a record Russian harvest, ensuring that the S&P GSCI Wheat ended the year down 2.7%. Sugar racked up its fourth consecutive year of annual gains, while caffeine fans should be heartened by the fact that coffee was the worst performer in the S&P GSCI in 2022, falling 21.9%.

With the USD posting its biggest annual gain since 2015 and interest rates rising, it was no surprise that the yellow metal had a lackluster year. The S&P GSCI Gold ended 2022 down a little less than 1.0%. That said, gold performed admirably in the final few months of the year on expectations that the U.S. Fed could begin to scale back the pace of its interest rate hikes, strong central bank purchases and the ongoing challenges in the cryptocurrency ecosystem.

The S&P GSCI Livestock eked out a gain of 4.8% in 2022. Lean hogs were the best performer, benefitting from tight supplies and less competition from poultry.

To learn more about the S&P GSCI and related indices, check out our Commodities Theme Page.

The posts on this blog are opinions, not advice. Please read our Disclaimers.