With the ZIRP world1 firmly in the rear view, the “income” in fixed income is back. As yields collapsed to record lows, income-starved investors sought alternative sources of income such as dividend strategies, which attracted record flows in related products throughout 2022. Now, with investment grade bond yields hitting as high as 6%, bonds are back to offering compelling income opportunities.

In addition to enhanced income, we analyze common risk signals such as credit spread, liquidity and interest rate risk to assess the current state of the bond market. Placing index attributes in a historical context, risk factors indicate stabilizing spreads and liquidity with declining interest rate risk in the broad indices. Lastly, we compare bond yields to alternative sources of income, with higher breakeven inflation yields offered in Treasury bonds compared to dividend yields in the S&P 500.

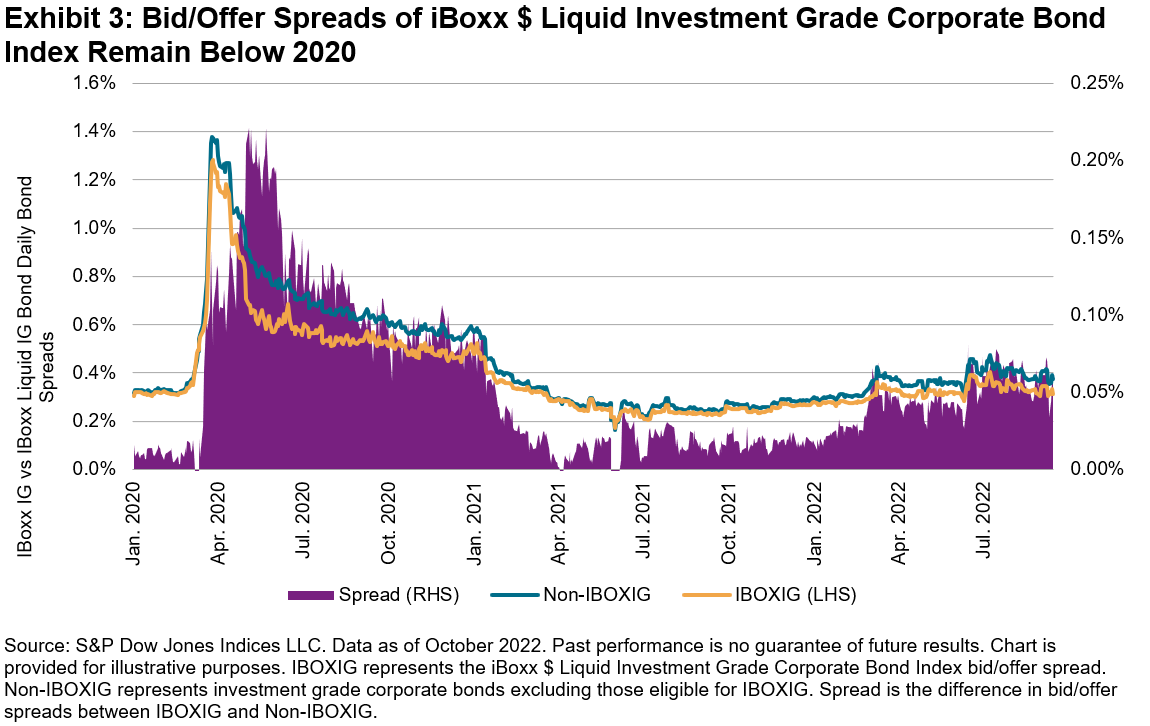

After more than a decade of investment grade corporations paying an average of 3.6%, and never more than 5%, yields on the iBoxx $ Liquid Investment Corporate Bond Index reached as high as 6.31% this summer, a nearly 4 standard deviation move from its 10-year average, before settling in the mid-5% range. While 3 standard deviation moves are rare, a move of 4 standard deviations enters “black swan” territory. Simply put, investment grade bond yields have not been this high since the aftermath of the credit crisis. Further, the spreads offered in excess of Treasuries by the iBoxx $ Liquid Investment Grade Corporate Bond Index are trading around the 10-year average of 150 bps and far from the 380 bps seen during the COVID-induced sell-off, suggesting historically high yields are not a result of degrading credit quality and the impact on rising rates is contained to the Treasury market.

During times of stress, volatility can adversely affect liquidity, particularly in fixed income. Treasury market liquidity has declined by an average of 0.1 bps of yield this year compared to 2021. The average bid/ask yields of the iBoxx Treasury Bond Index YTD rose to an average of 0.45 bps from 0.35 bps in 2021. Conversely, the liquidity of the iBoxx $ Liquid Investment Grade Corporate Bond Index has remained relatively stable by virtue of the index methodology selecting the most traded bonds, with the average bid/offer spread well below pandemic highs, an advantage magnified during stressed markets.

While current yields appear attractive on a historical basis and relative to dividends, potential risk remains inherent in fixed income. A bond’s sensitivity to rising rates is best measured through its duration, for every given unit of duration magnifies the negative impact on prices when yields rise. Throughout the pandemic, corporate officers took advantage of low borrowing costs to raise debt and extend the duration of their loans, thereby extending overall index duration and increasing sensitivity to interest rate increases. As borrowing dropped and debt supply dropped, duration fell back to historical levels. The iBoxx $ Liquid Investment Grade Corporate Bond Index duration has shed by over a year in 2022 and is now slightly below its long-term average. With a lower duration profile, the index is less sensitive to potential rate shocks going forward.

When compared on a real (inflation-adjusted) basis, it appears bonds are offering income well in excess of those offered by many stocks. The S&P U.S. TIPS 10-Year Index represents the real yield offered by the market. Indicative dividend yields of stocks in the S&P 500® are at their lowest level in at least a decade, while the yield premium of IBOXIG yields are their highest in at least a decade.

As the Fed combats inflation to stabilize the economy, assets including fixed income and growth stocks are adversely affected. While many have flocked to dividend strategies, fixed income remains attractive as a traditional, non-alternative, source of income. Improved liquidity through proper index construction, combined with declining interest rate risk, can potentially reduce risks that plagued previous time periods. Bonds may be back, and through an index lens, are looking better and better.

1 ZIRP refers to global central banks pursuing a zero-interest rate policy (ZIRP)

The posts on this blog are opinions, not advice. Please read our Disclaimers.