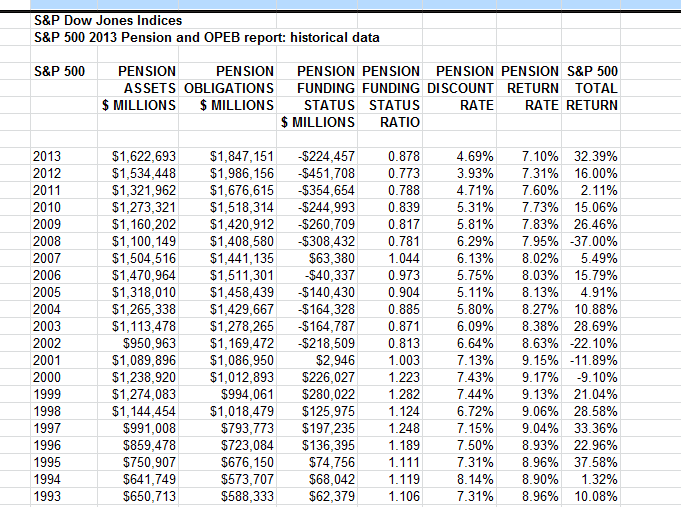

S&P has released their annual S&P 500 Pension report (which is available on its website at www.spdji.com or directly at bit.ly/1jPIDiE ). The short bottom line is that, in aggregate, pensions and OPEBs have become an acceptable and manageable expense for S&P 500 issues with respect to their underlying assets, earnings and cash-flow. For individuals, the additional responsibility has been shifted from corporations to them for pensions, and is already well underway for OPEBs, with the government, directly or indirectly, the ‘insurer’ of last resort – and individuals, directly or indirectly, the ‘insurer’ of the government. Some of the findings of the report are:

• Global equity markets continued to post double-digit gains in 2013, as the S&P 500 rose 29.60% (13.41% in 2012) and the S&P Global BMI Ex-U.S. posted a gain of 13.39% (14.05% in 2012). These gains, while significantly adding to assets, were insufficient to counter the increase in liabilities due to artificially low interest rates. Year-over-year comparisons from 2012 to 2013 indicate the following

• Pension underfunding was cut in half, decreasing to USD 224 billion (USD 218 billion deficit in 2002) from the record USD 452 billion

• The pension funding rate increased to 87.8% from 77.3%

• The discount rate increased to 4.69% from 3.93%

• The expected return rate declined to 7.10% from 7.31%, the 13th consecutive annual decline

• Funds tilted toward equities in their 2014 allocations, but they remained cautious of risk