Despite another year of flat performance from the S&P GSCI, it was a roller-coaster year with energy holding up the broad index while gold had its worst year since 1981. Below are the top 13 stories from 2013:

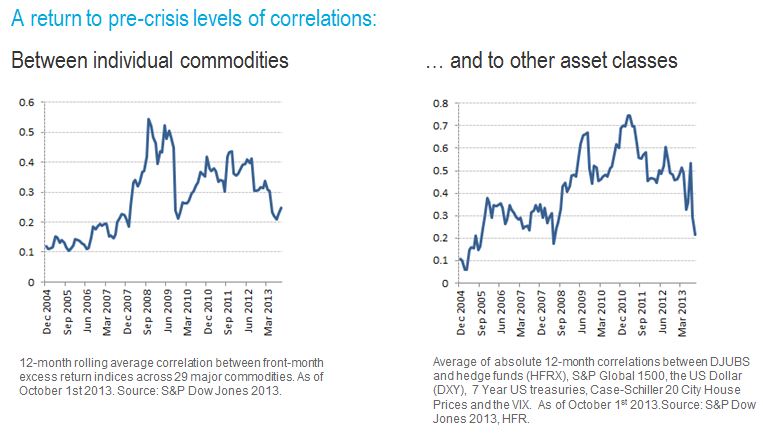

13. Risky Assets, Safe Havens or Lost Identities? All commodities in the S&P GSCI and the DJ-UBS CI crashed on June 20, 2013, losing 3.1% and 3.0%, respectively, after the Fed declared the U.S. economy was expanding strongly enough for the central bank to begin slowing the pace of its bond-buying stimulus later this year. This is generally bad news for commodities since historically as the U.S dollar strengthens, goods priced in dollars become more expensive for other currencies. The historical negative relationship between the U.S. dollar Read more […]

12. S&P GSCI Precious Metals Hits Lowest Since October 2010 On April 15, 2013 the S&P GSCI Precious Metals dropped 9.6% in one day, entering a bear market from the 2013 high occurring on January 23. Since then, the index has fallen further to hit its lowest level of 1733.52 since October 1, 2010 when it was at 1717.53. The precious metals index is down 20.1% YTD, and is off 21.3% from its 2013 peak of 2202.41. Uncertainty ahead of the Federal Reserve meeting may be causing gold investors to fear whether the Fed will signal the end or a reduction Read more […]

11. Strong as Steel: Impacts of New Futures This morning I was interviewed for CCTV2 on the impact of new futures markets with a focus on iron ore. Although Iron ore is not in the major indices, the DJ-UBS and S&P GSCI, it is an economically significant commodity that is the main input for steel. I thought you might be interested in the questions and answers, 1. What can we take-away from the launch of China’s Dalian Commodity Exchange’s new futures market? It is exciting when there is a new futures market launch. Generally, Read more […]

10. Paying Too Much at the Pump?! Why are gas prices so high? I know I’m not alone as “a commodity lady” wondering this as I pull out my credit card to pay at the pump. (Which is not often since I ride my bicycle to work most days) Gasoline prices typically rise in the summer because more people travel to take vacations. However, this July, the S&P GSCI Unleaded Gasoline gained 12.0%, which was the 4th highest increase in July in the history of the index (since 1988,) and the biggest rise in July since 2005 when the Read more […]

9. Ready to Roll or Need to Weight? In the past few years a number of indices have been launched with a goal of minimizing the impact of contango. The first indices launched with this goal were the simple (1-5 month) forward indices and the relatively static S&P GSCI Enhanced. In the time period from Aug 2004-May 2011, mentioned in my prior post, these indices did the job of outperforming the front month contracts in the S&P GSCI by reducing the negative impact from contango as shown in the chart below. However, Read more […]

8. Fear Gauge Spikes: Let’s Play Hot Potato For what risk does the commodity investor get paid? At what point is the fear gauge so high the risk gets passed like a hot potato? The answers to these questions will help explain why post the global financial crisis there has been a link between VIX spikes and commodity losses. Let’s address the first question of what risk the commodity investor takes to be compensated. While there are five fundamental sources that drive the commodity asset class returns, the insurance risk premium is a major Read more […]

7. Stanley Cup Index: What happened to the holy grail? Congratulations to the Chicago Blackhawks on their awesome win last night! I must admit I was very excited watching the most amazing finish I have ever seen in hockey, but as a commodity lady my first thought was about the metal in the Stanley Cup and what is it worth, especially given the current environment of a strengthening U.S. dollar and rising U.S. bond yields. From the economic backdrop, silver and nickel, the two metals that form the cup, are the worst performing metals in their respective Read more […]

6. Not ALL Weights are EQUAL: Why Brent isn’t Heavier than WTI 2014 is just around the corner now and the new weights for both the DJ-UBS CI and S&P GSCI have been announced. While the index weightings follow the methodologies, there are questions around the weights of two particular commodities, Brent crude oil and WTI crude oil. The interest comes from the fact that they are the most heavily weighted commodities across the two indices and there has historically been a popular spread trade between the two, since theoretically they should trade similarly Read more […]

5. Skipping Dessert?! Coffee, Sugar, Cocoa OR Bear, Bear, Bull Sorry, grains and meats, you are not one of the four main food groups. Since this is the case, eating may have just become more expensive, especially for the high-end chocolate lover. Not me of course… but once again, as a commodity lady, when I consume goods (or goodies) and notice that prices are increasing or decreasing I think about the prices of the raw materials and how the indices are impacted. I have noticed the price of chocolate increasing, so decided a deeper dive into the softs Read more […]

4. Where’s the Beef? While I was eating at a well-known restaurant chain, I saw this sign in the front window: So of course as a commodity lady my mind doesn’t think about choices like chicken or veggies, but I wonder what happened to the price of beef in the shortage and why is there a shortage? The S&P GSCI All Cattle, which includes both the S&P GSCI Feeder Cattle and Live Cattle, has gained 4.4% since the end of May, after losing 8.6% from the beginning of the year. See the monthly returns in Read more […]

3. Commodities Crystal Ball: What do the FUTURES hold? What strategies will be the most profitable over the next 12 months? Which spread will have the greatest opportunity? These are just a few questions we asked the audience at our S&P Dow Jones Indices 7th Annual Commodities Seminar, and we thought you may be interested in their answers. As I mentioned in a recent CNBC interview, the three main factors influencing commodities currently are quantitative easing, Chinese demand growth and geopolitical tensions. This backdrop has been characterized Read more […]

2. Index Rehab: Is Backwardation Back In-Style? My colleague, David Blitzer, is discussing index construction in his blog series “Inside the S&P 500″, and so far has reviewed selecting stocks and the float adjustment. While the index construction principles of transparency, liquidity, and systematic rules-based methodologies are widely similar between equities, commodities and other asset classes, there are details that distinguish the asset classes. For example, market capitalization and style like growth or value may be associated with Read more […]

1. Keeping Up With Contango’s Twist As mentioned in an article today in the Wall Street Journal, there may be a shift taking place in the commodities markets. In simple terms, there may be more predominant shortages of commodities. Generally as inventories are abundant, there are higher storage costs, which reduce returns from a condition called contango where the longer-dated contracts are more expensive than near contracts. As the inventories deplete, shortages may prevail, giving no value to storage for commercial consumers Read more […]

The most popular commodities post from an external contributor:

US Energy Production & Its Growth Dividend The substantial increase in the supply of energy from the United States is providing the US with an economic growth dividend. Since 2005, which we use as our base year since it roughly represents the year before the energy revolution in the US started, crude oil production in the US has increased 29% and natural gas production has grown 33%. The numbers are impressive and they continue to grow. Quantifying the US energy boom’s contribution to economic growth is not easy, even though it is Read more […]

The posts on this blog are opinions, not advice. Please read our Disclaimers.