The substantial increase in the supply of energy from the United States is providing the US with an economic growth dividend. Since 2005, which we use as our base year since it roughly represents the year before the energy revolution in the US started, crude oil production in the US has increased 29% and natural gas production has grown 33%. The numbers are impressive and they continue to grow.

Quantifying the US energy boom’s contribution to economic growth is not easy, even though it is obviously substantial. As is the often the case with economic impacts, the indirect effects can be much larger and more powerful over time than the direct effects. This makes quantifying the growth benefits to the US economy of the energy supply boom more of an art than a science.

In the US, we are seeing new infrastructure being built to move oil and gas production to users. Shifting relative prices have encouraged substitution of one form of energy for another and have stimulated construction, including new industrial plants near the sources of the new supplies, especially natural gas. In some cases natural gas has replaced coal as fuel for generating electricity, and the displaced coal has served to increased US exports. Natural gas has not generally been considered a transportation fuel, yet its abundance and lower price per BTU is generating greater interest to power bus fleets as well as train locomotives.

Taking a very broad view of the indirect stimulus coming from the new oil and natural gas production, the incremental advantage to the US is probably between 0.5% and 1% of extra real GDP per year, and this energy growth dividend may last for the next five years or more as production continues to increase, as the distribution infrastructure is built, and as industrial users make new investments and build new plants to take advantage of the energy boom.

As noted, our energy growth dividend assessment is more of a back of the envelope calculation than a detailed quantification. Some energy analysts would go with a higher impact, while some traditional macroeconomists are on the lower side. No one, however, is downplaying the long-term importance to the US economy. What is clear is that the energy boom has come at a very good time for the US economy relative to other industrial economies struggling with the lingering aftereffects of the Great Recession of 2008-2009.

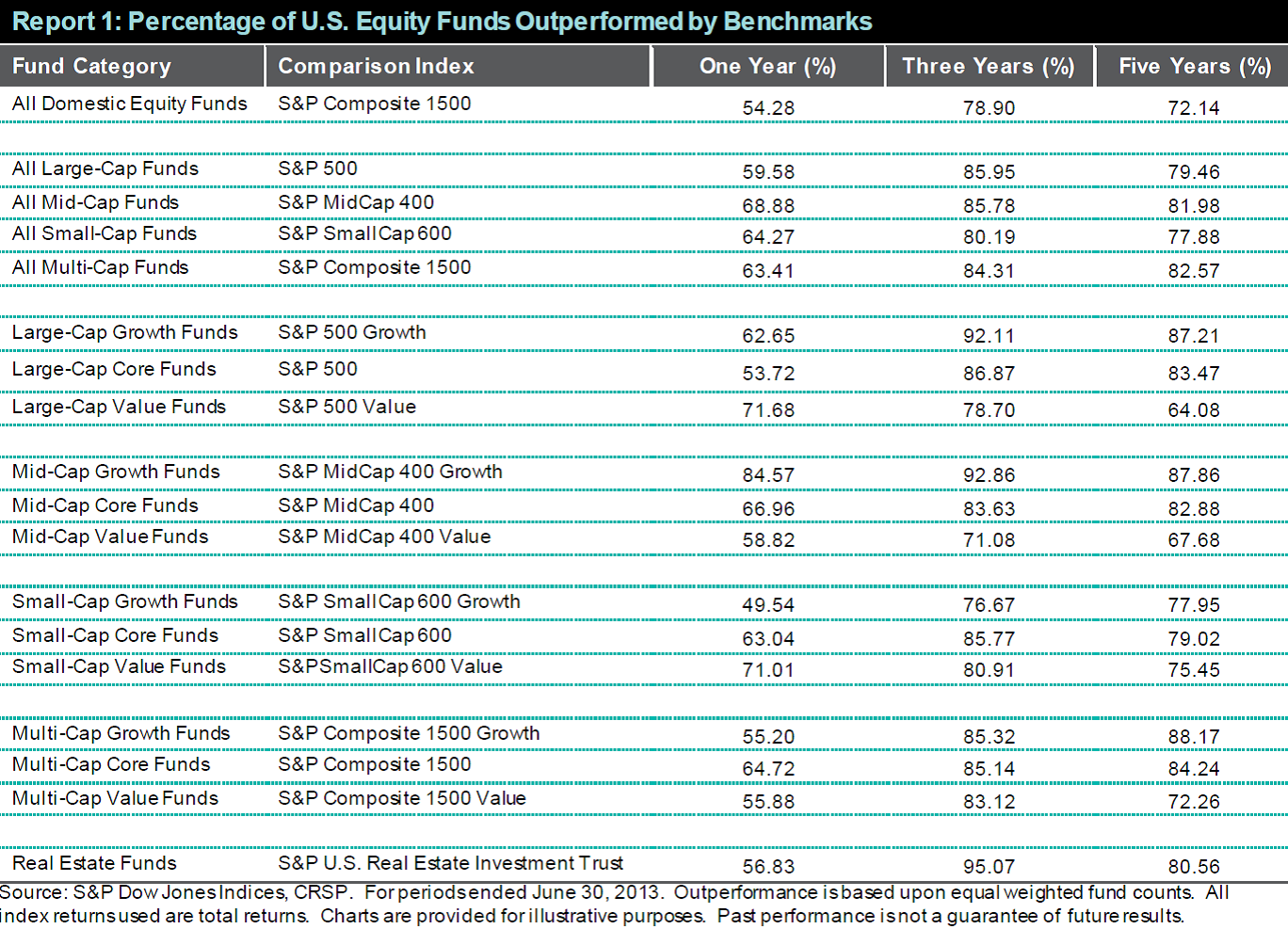

All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the authors and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience.

S&P Dow Jones Indices is an independent third party provider of investable indices. We do not sponsor, endorse, sell or promote any investment fund or other vehicle that is offered by third parties. The views and opinions of any third party contributor are his/her own and may not necessarily represent the views or opinions of S&P Dow Jones Indices or any of its affiliates.

The posts on this blog are opinions, not advice. Please read our Disclaimers.