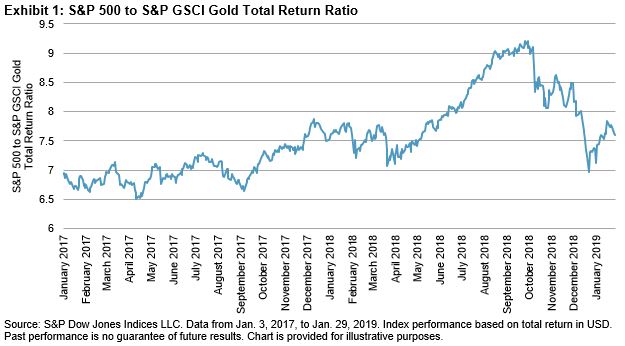

It should be no surprise to seasoned investors that gold has regained some of its shine over recent months. A resurgence in investors’ appetite for so-called “safe-haven” assets has seen the S&P GSCI Gold rise by 11% since mid-August 2018 to the highest level since May 2018. Considering gold’s relative performance, which is arguably a more valuable comparison from a portfolio perspective, gold strongly outperformed U.S. equities during the final quarter of 2018 before giving back some of that outperformance, as U.S. equities rallied through January 2019.

There is certainly no lack of risk catalysts for those investors that are ascending the investment wall of worry at the start of the new year and considering increasing their tactical allocation to gold.

- A delayed hangover from the sharp global equity market correction in late 2018 and the related uptick in equity market volatility (a proxy for the “fear factor” in any market).

- Growing concern that the global economy is slowing, albeit from a relatively strong position.

- A stalling Chinese economy at the same time as burgeoning debt levels that make a large stimulus push increasingly difficult for Chinese leaders to enact.

- Expectations that the U.S. Federal Reserve may park or even reverse its rising interest rate regime (non-income-generating assets tend to perform better in lower interest rate and lower U.S. dollar environments).

- Geopolitical turmoil ranging from the U.S. government shutdown, Brexit, and the ongoing U.S.-China trade war saga, to the more recent escalation of the political situation in Venezuela.

But as investors navigate through the myriad of financial risk factors that will shape the trajectory of gold prices over the coming months, it is important for them to differentiate between investor and non-investment demand for gold. Clearly, investor demand for gold has been strong, as illustrated by the flow of funds into gold-linked investment products, but physical demand from the jewelry sector—highly dependent on demand in India and China—has been less stellar. According to the World Gold Council, global jewelry demand was close to flat year-over-year in 2018. On a more positive note, an uptick in central bank gold buying for strategic reserves bodes well for the overall strength of demand. Central banks purchased 74% more gold in 2018 than 2017, for the second-highest annual total on record.

Gold has, at least temporarily, re-entered a golden period in the eyes of those investors looking for safe-haven assets to insulate their portfolios from any number of risks buffeting global financial markets. Gold’s ongoing performance will depend heavily on how quickly these risks dissolve or escalate but will also continue to be influenced by non-investment demand trends.

The posts on this blog are opinions, not advice. Please read our Disclaimers.