[{"display":"Anu Ganti","title":"Head of U.S. Index Investment Strategy","image":"\/wp-content\/authors\/anu_ganti-505.jpg","url":"https:\/\/www.indexologyblog.com\/author\/anu_ganti\/"},{"display":"Tim Edwards","title":"Managing Director, Index Investment Strategy","image":"\/wp-content\/authors\/timothy_edwards-535.jpg","url":"https:\/\/www.indexologyblog.com\/author\/timothy_edwards\/"},{"display":"Hamish Preston","title":"Head of U.S. Equities","image":"\/wp-content\/authors\/hamish_preston-512.jpg","url":"https:\/\/www.indexologyblog.com\/author\/hamish_preston\/"},{"display":"Fiona Boal","title":"Managing Director, Global Head of Equities","image":"\/wp-content\/authors\/fiona_boal-317.jpg","url":"https:\/\/www.indexologyblog.com\/author\/fiona_boal\/"},{"display":"Wenli Bill Hao","title":"Director, Factors and Dividends Indices, Product Management and Development","image":"\/wp-content\/authors\/bill_hao-351.jpg","url":"https:\/\/www.indexologyblog.com\/author\/bill_hao\/"},{"display":"Phillip Brzenk","title":"Managing Director, Global Head of Multi-Asset Indices","image":"\/wp-content\/authors\/phillip_brzenk-325.jpg","url":"https:\/\/www.indexologyblog.com\/author\/phillip_brzenk\/"},{"display":"Michael Orzano","title":"Head of Exchange Products and Digital Assets","image":"\/wp-content\/authors\/Mike.Orzano-231.jpg","url":"https:\/\/www.indexologyblog.com\/author\/mike-orzano\/"},{"display":"Maria Sanchez","title":"Director, Sustainability Index Product Management, U.S. Equity Indices","image":"\/wp-content\/authors\/maria_sanchez-527.jpg","url":"https:\/\/www.indexologyblog.com\/author\/maria_sanchez\/"},{"display":"John Welling","title":"Head of Global Equities & Thematic Indices","image":"\/wp-content\/authors\/john_welling-246.jpg","url":"https:\/\/www.indexologyblog.com\/author\/john_welling\/"},{"display":"George Valantasis","title":"Director, Factors and Dividends","image":"\/wp-content\/authors\/george-valantasis-453.jpg","url":"https:\/\/www.indexologyblog.com\/author\/george-valantasis\/"},{"display":"Sherifa Issifu","title":"Associate Director, Global Exchanges","image":"\/wp-content\/authors\/sherifa_issifu-580.jpg","url":"https:\/\/www.indexologyblog.com\/author\/sherifa_issifu\/"},{"display":"Silvia Kitchener","title":"Director, Global Equity Indices, Latin America","image":"\/wp-content\/authors\/silvia_kitchener-522.jpg","url":"https:\/\/www.indexologyblog.com\/author\/silvia_kitchener\/"},{"display":"Rupert Watts","title":"Head of Factors and Dividends","image":"\/wp-content\/authors\/rupert_watts-366.jpg","url":"https:\/\/www.indexologyblog.com\/author\/rupert_watts\/"},{"display":"Ved Malla","title":"Associate Director, Client Coverage","image":"\/wp-content\/authors\/ved_malla-347.jpg","url":"https:\/\/www.indexologyblog.com\/author\/ved_malla\/"},{"display":"Akash Jain","title":"Director, Global Research & Design","image":"\/wp-content\/authors\/akash_jain-348.jpg","url":"https:\/\/www.indexologyblog.com\/author\/akash_jain\/"},{"display":"Jason Giordano","title":"Director, Fixed Income, Product Management","image":"\/wp-content\/authors\/jason_giordano-378.jpg","url":"https:\/\/www.indexologyblog.com\/author\/jason_giordano\/"},{"display":"Sean Freer","title":"Director, Global Exchange Indices","image":"\/wp-content\/authors\/sean_freer-536.jpg","url":"https:\/\/www.indexologyblog.com\/author\/sean_freer\/"},{"display":"Cristopher Anguiano","title":"Associate Director, U.S. Equity Indices","image":"\/wp-content\/authors\/cristopher_anguiano-506.jpg","url":"https:\/\/www.indexologyblog.com\/author\/cristopher_anguiano\/"},{"display":"Qing Li","title":"Director, Global Research & Design","image":"\/wp-content\/authors\/qing_li-190.jpg","url":"https:\/\/www.indexologyblog.com\/author\/qing_li\/"},{"display":"Elizabeth Bebb","title":"Director, Factor & Dividend Indices","image":"\/wp-content\/authors\/elizabeth_bebb-511.jpg","url":"https:\/\/www.indexologyblog.com\/author\/elizabeth_bebb\/"},{"display":"Joseph Nelesen","title":"Head of Specialists, Index Investment Strategy","image":"\/wp-content\/authors\/joseph_nelesen-452.jpg","url":"https:\/\/www.indexologyblog.com\/author\/joseph_nelesen\/"},{"display":"Sue Lee","title":"APAC Head of Index Investment Strategy","image":"\/wp-content\/authors\/sue_lee-531.png","url":"https:\/\/www.indexologyblog.com\/author\/sue_lee\/"},{"display":"Glenn Doody","title":"Vice President, Product Management, Technology Innovation and Specialty Products","image":"\/wp-content\/authors\/glenn_doody-517.jpg","url":"https:\/\/www.indexologyblog.com\/author\/glenn_doody\/"},{"display":"Liyu Zeng","title":"Director, Global Research & Design","image":"\/wp-content\/authors\/liyu_zeng-252.png","url":"https:\/\/www.indexologyblog.com\/author\/liyu_zeng\/"},{"display":"Eduardo Olazabal","title":"Associate Director, Global Exchange Indices","image":"\/wp-content\/authors\/eduardo_olazabal-451.jpg","url":"https:\/\/www.indexologyblog.com\/author\/eduardo_olazabal\/"},{"display":"Fei Wang","title":"Senior Analyst, U.S. Equity Indices","image":"\/wp-content\/authors\/fei_wang-443.jpg","url":"https:\/\/www.indexologyblog.com\/author\/fei_wang\/"},{"display":"Izzy Wang","title":"Associate Director, Factors and Dividends","image":"\/wp-content\/authors\/izzy.wang-326.jpg","url":"https:\/\/www.indexologyblog.com\/author\/izzy-wang\/"},{"display":"Srineel Jalagani","title":"Senior Director, Thematic Indices","image":"\/wp-content\/authors\/srineel_jalagani-446.jpg","url":"https:\/\/www.indexologyblog.com\/author\/srineel_jalagani\/"},{"display":"Diego Zurita","title":"Senior Analyst, Global Equities & Thematics","image":"\/wp-content\/authors\/diego_zurita-592.jpg","url":"https:\/\/www.indexologyblog.com\/author\/diego_zurita\/"},{"display":"Michael Mell","title":"Global Head of Custom Indices","image":"\/wp-content\/authors\/michael_mell-590.jpg","url":"https:\/\/www.indexologyblog.com\/author\/michael_mell\/"},{"display":"Jason Ye","title":"Senior Director, Factors and Dividends","image":"\/wp-content\/authors\/Jason%20Ye-448.jpg","url":"https:\/\/www.indexologyblog.com\/author\/jason-ye\/"},{"display":"Andrew Innes","title":"Head of Global Research & Design","image":"\/wp-content\/authors\/andrew_innes-189.jpg","url":"https:\/\/www.indexologyblog.com\/author\/andrew_innes\/"},{"display":"Rachel Du","title":"Senior Analyst, Global Research & Design","image":"\/wp-content\/authors\/rachel_du-365.jpg","url":"https:\/\/www.indexologyblog.com\/author\/rachel_du\/"},{"display":"Anna Mittra","title":"Associate Director, Global Exchanges","image":"\/wp-content\/authors\/anna_mittra-554.jpg","url":"https:\/\/www.indexologyblog.com\/author\/anna_mittra\/"},{"display":"Brandon Hass","title":"Global Head of Client Solutions Group, Direct Indexing and Model Portfolios","image":"\/wp-content\/authors\/brandon_hass-568.jpg","url":"https:\/\/www.indexologyblog.com\/author\/brandon_hass\/"},{"display":"Agatha Malinowski","title":"Quantitative Associate, Index Investment Strategy","image":"\/wp-content\/authors\/agatha_malinowski-593.jpg","url":"https:\/\/www.indexologyblog.com\/author\/agatha_malinowski\/"},{"display":"Daniel Perrone","title":"Former Director and Head of Operations, ESG Indices","image":"\/wp-content\/authors\/daniel_perrone-387.jpg","url":"https:\/\/www.indexologyblog.com\/author\/daniel_perrone\/"},{"display":"Abbie Zhang","title":"Senior Analyst, Thematic Indices","image":"\/wp-content\/authors\/abbie_zhang-538.jpg","url":"https:\/\/www.indexologyblog.com\/author\/abbie_zhang\/"},{"display":"Hugo Barrera","title":"Senior Analyst, Product Management","image":"\/wp-content\/authors\/hugo_barrera-412.jpg","url":"https:\/\/www.indexologyblog.com\/author\/hugo_barrera\/"},{"display":"Louis Bellucci","title":"Senior Director, Index Governance","image":"\/wp-content\/authors\/louis_bellucci-377.jpg","url":"https:\/\/www.indexologyblog.com\/author\/louis_bellucci\/"},{"display":"Stephanie Rowton","title":"Senior Director, Tokenization and U.S. Equities","image":"\/wp-content\/authors\/stephanie_rowton-578.jpg","url":"https:\/\/www.indexologyblog.com\/author\/stephanie_rowton\/"},{"display":"Carlos Mendizabal","title":"Senior Analyst, Global and Thematic Equity Indices Product Management","image":"\/wp-content\/authors\/carlos_mendizabal-572.jpg","url":"https:\/\/www.indexologyblog.com\/author\/carlos_mendizabal\/"},{"display":"Narottama Bowden","title":"Director, Sustainability Indices Product Management","image":"\/wp-content\/authors\/narottama_bowden-331.jpg","url":"https:\/\/www.indexologyblog.com\/author\/narottama_bowden\/"},{"display":"Wanying Wu","title":"Senior Analyst, Private Markets Indices","image":"\/wp-content\/authors\/Wanying_Wu-533.jpg","url":"https:\/\/www.indexologyblog.com\/author\/wanying_wu\/"},{"display":"Hector Huitzil","title":"Senior Analyst, Global Equity Indices","image":"\/wp-content\/authors\/hector_huitzil-552.jpg","url":"https:\/\/www.indexologyblog.com\/author\/hector_huitzil\/"}]

S&P DJI combines global reach with local expertise, working with exchanges around the world to build indices for both the local and international investment communities.

S&P DJI combines global reach with local expertise, working with exchanges around the world to build indices for both the local and international investment communities.

S&P DJI combines global reach with local expertise, working with exchanges around the world to build indices for both the local and international investment communities.

S&P DJI has an extensive history of delivering robust and transparent benchmarks to the financial industry and always endeavors to deliver high quality indices in conformity with our core values and in compliance with all applicable laws and regulations as well as industry standards and guidelines.

S&P Global's Code of Business Ethics

coupled with S&P DJI policies and procedures set the standard for an effective governance program.

Find out what makes our indices tick—access index policies and methodologies, GICS® structure definitions, rebalancing and holiday schedules, and other information related to index calculation and maintenance.

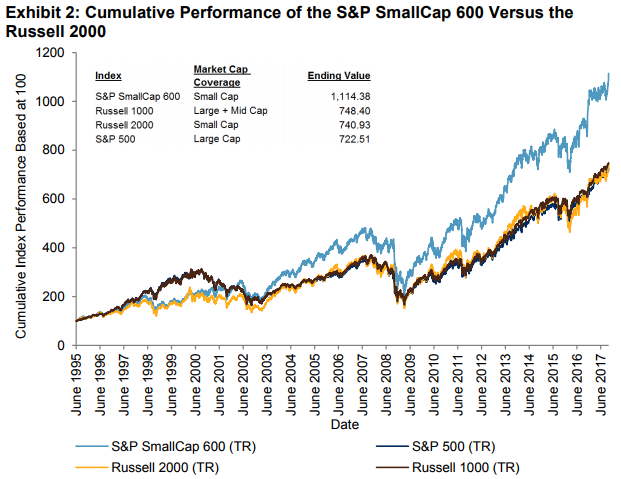

However, it’s not only where in the world small caps generate revenue from that matters, it is that the small caps have earnings. Just as in the methodology of the S&P 500, the S&P SmallCap 600 has the same financial viability eligibility criteria that states the sum of the most recent four quarters’ as-reported earnings should be positive as should the most recent quarter. This basic quality rule is vital to earning the small cap premium as discussed here in detail, and shown below where since inception of the S&P 600, only it has outperformed the large caps while the Russell 2000 has performed similarly to both the S&P 500 and Russell 1000:

Source: S&P Dow Jones Indices LLC. Data from June 1, 1995, to Sept. 29, 2017. Index performance based on total return in USD. Past performance is no guarantee of future results. Chart is provided for illustrative purposes.

As the media has highlighted small cap performance this year, they are asking more questions and doing deeper analysis on the available small cap indices. Upon closer inspection of the small cap index choices, they are calling the Russell 2000, “the wrong small cap index.”

Here are two separate examples from articles where this has been published:

Barron’s SIZING UP SMALL CAPS: A Tale of Two Indexes Small-cap investors may be measuring their performance against the wrong benchmark

By Brett Arends – January 27, 2018 Are investors following the wrong small-company stock index?

“The most commonly used benchmark is the Russell 2000, and over 90% of investment funds focusing on U.S. small-cap stocks use it to peg their performance. But for more than two decades, it consistently has done worse than the lesser-known S&P SmallCap 600 index…”

Financial Times Are you following the wrong small-cap index?

Nicole Bullock in New York – June 8, 2018 The widely-tracked Russell 2000 has done well, but not as well as a rival benchmark

“Small companies are setting a record pace on Wall Street this year, but many investors are missing out on the cream thanks to a divergence between the two main benchmarks that define the sector for fund managers…”

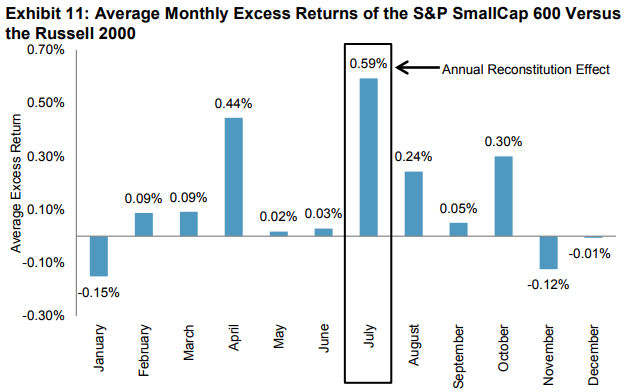

In addition to the basic earnings screen that has enabled the S&P 600 to deliver the small cap premium through time, there is one more reliable contributor to the S&P 600’s outperformance over the Russell 2000, and it happens in July.

The other key methodology difference that drives the outperformance of the S&P SmallCap 600 versus the Russell 2000 is the annual reconstitution effect that dilutes Russell 2000 returns. It, too, has been well documented, not only in a report by S&P Dow Jones Indices13

showing the significant t-stat of the return difference of the indices, but also by several other well-known researchers.

As winners from the Russell 2000 graduate to the Russell 1000, and losers from the Russell 1000 move down to the small-cap index, fund managers are forced to sell winners and buy losers, thereby creating a negative momentum portfolio.14 Jankovskis15 and Chen, Noronha, and Singal16 estimated that the predictable nature of the June Russell rebalancing process biases the return of the index downward by an average of approximately 2% per year. Similarly, Chen, Noronha, and Singal found the rebalancing impact to be 1.3% per year.

Source: S&P Dow Jones Indices LLC, Russell, FactSet. Data from 1994 through 2016. Past performance is no guarantee of future results. Chart is provided for illustrative purposes and reflects hypothetical historical performance. Please see the Performance Disclosure at the end of this document for more information regarding the inherent limitations associated with back-tested performance.

Together, quality and reconstitution account for most of the S&P SmallCap 600’s outperformance over the Russell 2000. Some of the return difference may also be associated with the liquidity criterion of the S&P SmallCap 600 that is not applied to the Russell 2000. Within the S&P SmallCap 600, a small percentage of stocks, roughly 3%, have a three-month average daily trading volume (ADVT) of less than USD 1 million, compared with about 15% of stocks in the Russell 2000 that have a three-month ADVT of less than USD 1 million. (2017, pp. 13-14)

Endotes:

13 Brzenk, P. and A. Soe, (2015), “A Tale of Two Benchmarks: Five Years Later,” S&P Dow Jones Indices. 14 Furey, James H., (2001), “Russell 2000 Bigger but not better benchmark.” 15 Jankovskis, Peter, (2002), “The Impact of Russell 2000 Rebalancing on Small-Cap Performance.” 16 Chen, Honghui, Greg Noronha, and Vijay Singal, (2006), “Index Changes and Losses to Investors in S&P 500 and Russell 2000 Index Funds.”

The posts on this blog are opinions, not advice. Please read our Disclaimers.

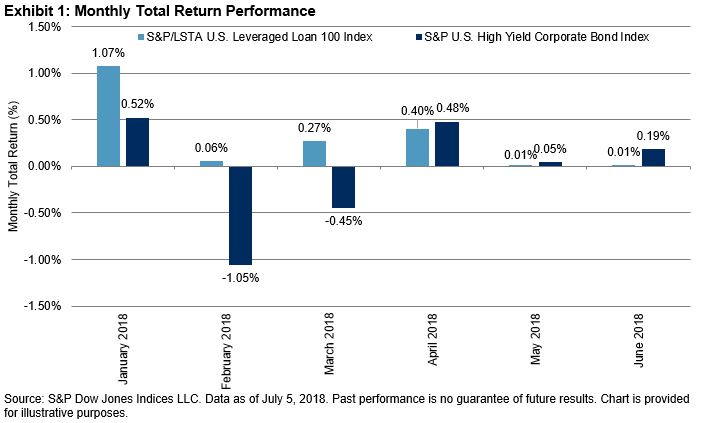

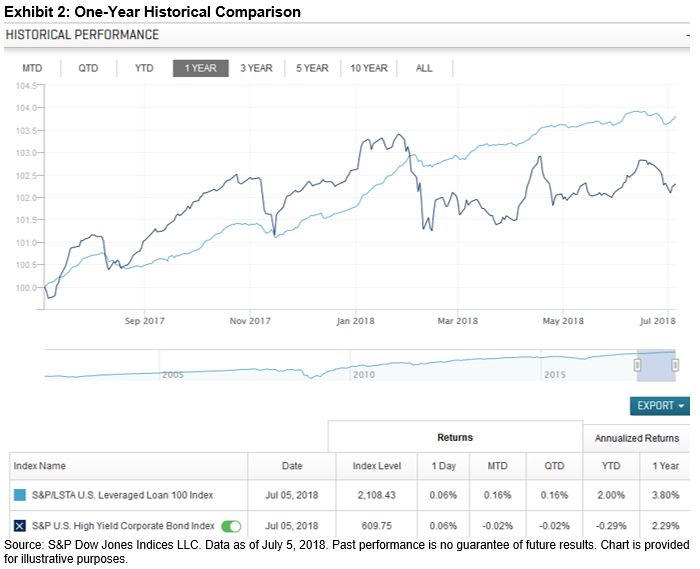

As of July 5, 2018, the S&P/LSTA U.S. Leveraged Loan 100 Index returned 2% YTD, compared with the S&P U.S. High Yield Corporate Bond Index’s return of -0.29%. In 2018, U.S. high-yield performance has experienced two rather sizeable negative returns—back-to-back declines in February (-1.05%) and March (-0.45%)—followed by a turnaround in April (see Exhibit 1). Steady positive performance throughout has kept loans in the green for the year. In 2017, U.S. high yield prevailed in overall performance versus loans (with 2017 total returns of 7.2% and 3.3%, respectively), as more return is expected for the risk of being almost five years out in duration (4.87% as of July 5, 2018—see Exhibit 2).

Increased demand for bank loans this year has caused more loans to come to market, providing record-setting supply and increasing the amount outstanding of the S&P/LSTA U.S. Leveraged Loan 100 Index by 5% since the beginning of the year. Such large amounts of supply kept the average price and monthly performance flat for May and June. Concerns about the recent supply have centered on loan quality and the number of deals with fewer covenants and other protections for investors.

The floating rate, senior secured characteristics of this asset class provide some downside protection when compared with an unsecured high-yield bond. Loans provide some relative protection against duration risk in rising rate environments and structural protections as a senior secured instrument in periods of economic stress.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

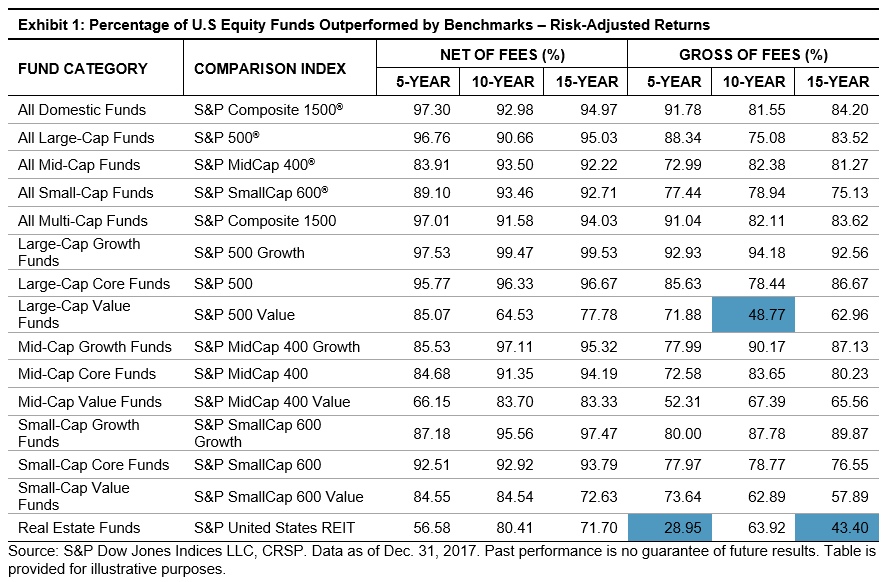

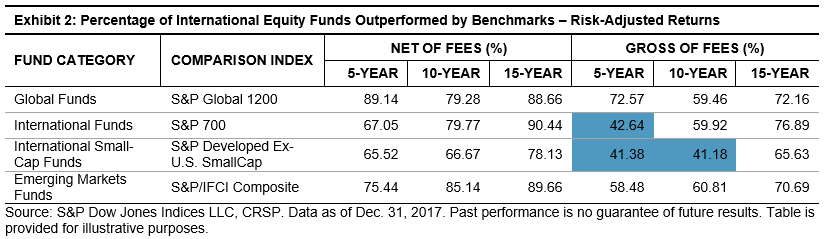

Evaluating active managers’ performance through a risk lens is rooted in modern portfolio theory (MPT), which states that the expectation of returns must be accompanied by risk—the variation (or volatility) around the expected return. MPT assumes that higher risk should be compensated, on average, by higher returns.

Institutional investors tend to be interested in risk-adjusted returns. In addition to the performance of managers hired to manage their assets, institutional investors also look at the risks managers take to achieve those returns.

With that in mind, we initiated the first Risk-Adjusted SPIVA Scorecard, which seeks to establish whether actively managed funds are able to generate higher risk-adjusted returns than their corresponding benchmarks over a long-term investment horizon.

In our analysis, we used the standard deviation of monthly returns over a given period to define and measure risk. The monthly standard deviation was annualized by multiplying it by the square root of 12. The risk/return ratio looks at the relationship and the trade-off between risk and return. All else equal, a fund with a higher ratio is preferable since it delivers a higher return per unit of risk taken. To make our comparison relevant, we also adjusted the returns of the benchmarks used in our analysis by their volatility.

Given that indices do not incur costs, we also present gross of fees performance figures by adding the expense ratio back to net of fees returns. In this way, all else equal, higher risk taken by a manager should be compensated by higher returns.

Exhibits 1 and 2 look at the percentage of domestic and international managers outperformed by benchmarks, using risk-adjusted returns on gross of fees and net of fees bases over 5-, 10-, and 15-year investment horizons. We observe that large-cap value funds (over 10 years) and real estate funds (over 5 and 15 years) outperformed their respective benchmarks when using gross of fees risk-adjusted returns, indicating that fees played a major role in those categories.

Similarly, in international equities, we find that fees contributed meaningfully to the underperformance of international and international small-cap funds. For example, when using gross of fees returns in the risk-adjusted performance analysis, funds in those two categories outperformed the benchmarks over 5- and 10-year periods. When net of fees returns were used, the majority of managers across all categories underperformed the benchmarks.

The evaluation of active managers’ performance through a risk lens is an integral part of the investment decision-making process. However, as our study highlights, actively managed domestic and international equity funds across almost all categories did not outperform the benchmarks on a risk-adjusted basis. The figures improved for some categories when gross of fees returns were used. Therefore, we did not see evidence that actively managed funds were better risk managed than passive indices.

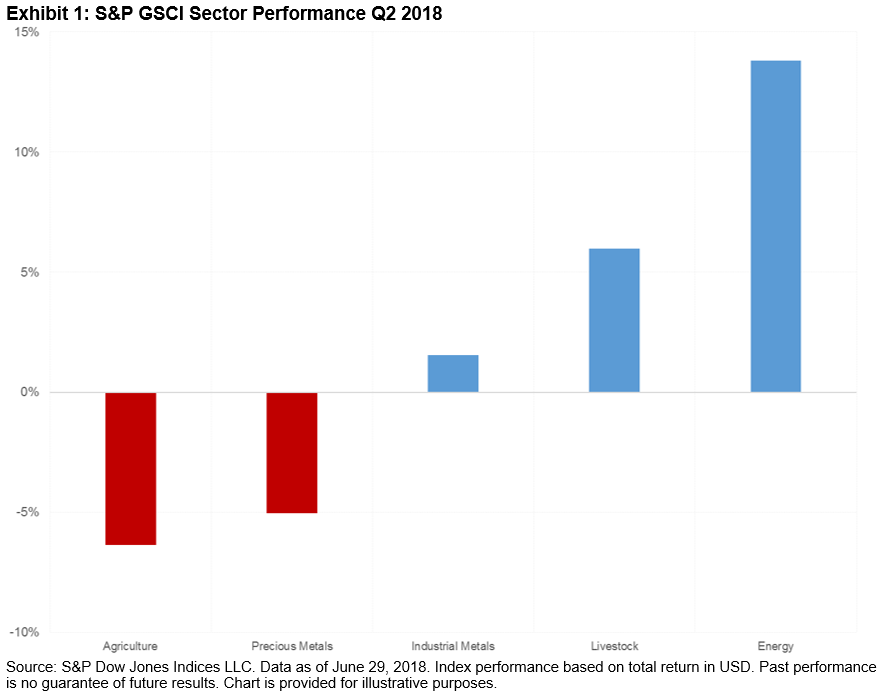

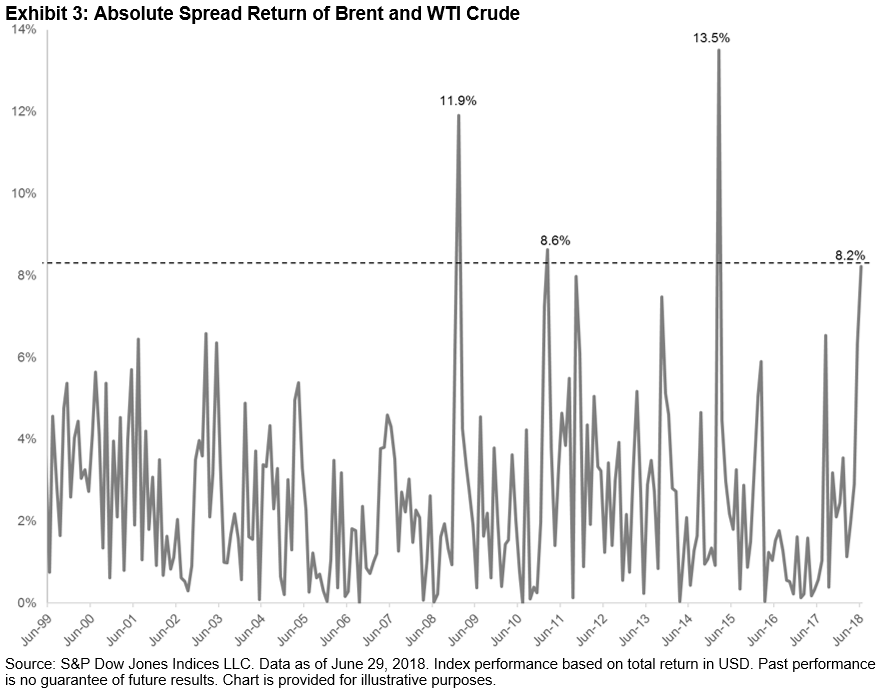

The S&P GSCI was up 8.0% for the Q2 2018, with agriculture being the worst-performing sector in the index, and energy the best (see Exhibit 1). Of the 24 commodities tracked by the index, 14 finished the quarter on a positive note. Soybeans was the worst-performing commodity in the index, and Brent crude was the best.

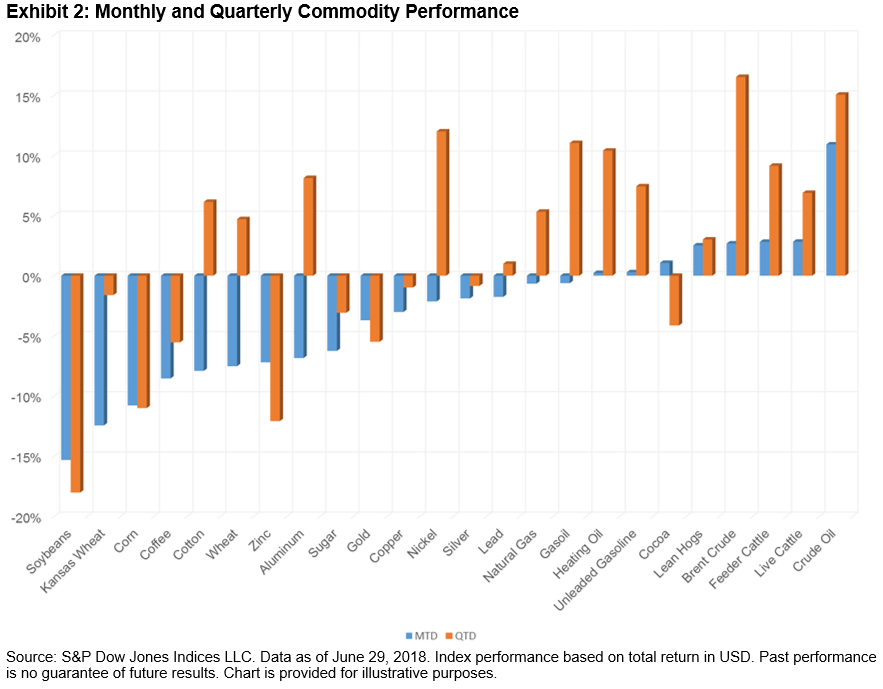

Exhibit 2 depicts the monthly and quarterly performance of the 24 commodities tracked by the indices.

Soybeans was the worst-performing commodity in the index on both a monthly and quarterly basis, down 15.3% for the month and 18.0% for the quarter. The tensions in the trade relationship between China and the U.S. have led to uncertainty about whether China, one of the largest buyers and consumers of U.S. soybeans, will purchase the grain in the fall.

WTI crude oil was the best-performing commodity on a monthly basis, up 10.9%, while Brent crude was the best-performing commodity for the quarter, up 16.5%. The spread of 8.2% between Brent and WTI was the fourth-highest month-end spread in the history of the indices (the S&P GSCI Brent Crude Oil launched in 1999). Exhibit 3 depicts the absolute values of the spread between Brent and WTI based on the indices and representative of the contracts.

In June, WTI benefited from reduced crude flows to Cushing, Oklahoma, caused by an outage in the largest producer of crude oil in Canada, and the Trump administration warning companies from buying Iranian oil. However, Brent outpaced WTI for the quarter, due to high production and inventory levels for WTI Crude oil, compared with Brent, which has been moderated by OPEC and Russia’s collaboration to control production, a deal that was announced in March 2018.

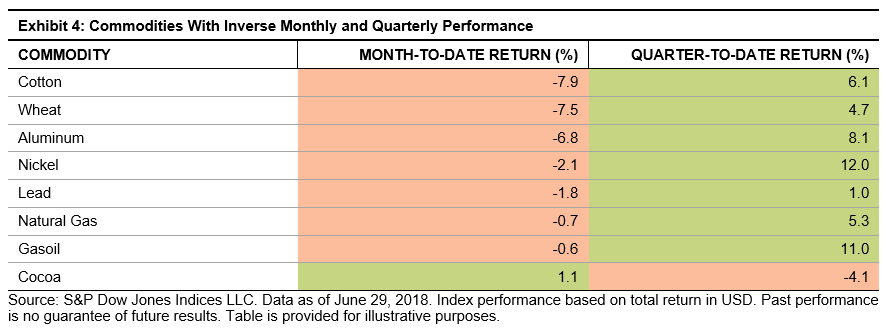

Exhibit 4 shows the commodities that presented June monthly returns that were in the opposite direction of their quarterly returns.

Cocoa was the only positive agricultural commodity in June, up 1.1%, benefiting from Cote d’Ivoire and Ghana (which produce about 60% of the world’s cocoa) announcing plans to work together in order to strengthen the cocoa sector and set price floors to better manage global prices, which were weighed down over the past two years by higher-than-expected levels of production. Cotton and wheat were hurt by high production levels, and aluminum, nickel, and lead were hurt by a rising U.S. Dollar Index. Gasoil prices declined as the Canadian regulatory and appeals commission lowered the price of petroleum products in mid-June, while natural gas was weighed down by high inventory levels.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

The world’s most prestigious cycling race, the Tour de France, begins tomorrow. The tour lasts three weeks and comprises a series of one-day stages. Although the main prize – the yellow jersey – is awarded to the rider that takes the minimum amount of time to complete the entire tour, there are plenty of races (and prizes) up for grabs along the way. Some cyclists aim to prove themselves as the best sprinter, while others hope to wear the polka-dot jersey awarded to the “King of the Mountains” – the fastest cyclist over the tour’s stages in the Alps, Pyrenees, and the Massif Central.

Each rider’s particular talents are important in determining the stages to which their style of racing is most suited. However, not all talents are rewarded equally: one of the interesting facts about the Tour de France is that the yellow jersey is typically captured by a rider who excels in the mountainous stages. This is because – generally speaking – there is a greater degree of variation in completion times in the mountain stages than the sprint stages. Since the overall winner is based on the total time, outperformance in the mountain stages is more valuable than outperformance on the flats, even though there are more of the latter. Said differently, the greater dispersion in rider’s times during the mountain stages mean the rewards to outperformance are higher compared to stages when everyone sprints at similar speeds to a bunched finish.

The relative value of sprinting and mountain-climbing in the Tour de France has analogies in financial markets. Over time, investors will encounter calm, smooth gains in some periods, and more challenging, volatile returns in others. Extending the analogy further, just as performance in the mountainous stages often determines the yellow jersey, the performance of equity portfolios during the most volatile periods goes a long way in determining long-term returns, because there are typically greater differences between the relative winners and losers during periods of elevated volatility.

As we showed in our recent practitioner’s guide, low volatility indices tend to underperform in less volatile, rising markets and outperform in more volatile, falling markets. The table below summarizes this empirically through the monthly “capture ratios” for a number of our low volatility indices. Each monthly downside capture ratio is less than one, meaning the low volatility indices were typically better insulated in months when their benchmark fell. The higher upside capture ratios indicate that the low volatility indices stayed closer to the pack when the benchmark rose.

Exhibit 1: Low Volatility Indices Have Provided Downside Protection And Upside Participation

Source: “Low Volatility: A Practitioner’s Guide”; Edwards, Lazzara & Preston (2018), S&P Dow Jones Indices LLC. Data based on monthly total returns from January 2001 to April 2018. Past performance is no guarantee of future results. Table is provided for illustrative purposes and reflects hypothetical historical performance.

Just as the race for King of the Mountains is a key determinant of who takes home the yellow jersey, the pattern of upside participation and downside protection offered by low volatility indices can help to explain how many of them have recorded market-beating performance in the longer term, historically. And in a year when momentum, growth and information technology have dominated headlines, low volatility may presently offer a way to avoid a crowded finish.

The posts on this blog are opinions, not advice. Please read our Disclaimers.