As of Dec. 31, 2018, the passive implementation of dividend strategies measured approximately USD 141 billion based on assets under management (AUM) of dividend-focused ETFs listed in the U.S. This is a staggering amount considering that only 10 years ago the AUM amounted to just over USD 6 billion.[1] The growth in assets, as well as the number of passive dividend-oriented investment products, is a testament to the popularity of dividend investing.

Dividend strategies come with various investment objectives and target different characteristics. For example, some aim to achieve absolute dividend yields, while others may target steady dividend growth rates or combine other fundamentals such as quality or low volatility with yield. The selection and allocation to different dividend strategies can also play impactful roles. No matter what the yield seeker’s focus is, common challenges they face include dividend cuts and elimination. In addition, companies exhibiting high dividend yield may fall in a “dividend trap,” since high dividend yield can be caused by decreasing stock prices rather than the increasing dividends payments. To minimize these risks, many market participants incorporate quality[2] metrics or other filters such as volatility into dividend-focused strategies. These measures aim to ensure that a given dividend strategy is only selecting companies that are capable of maintaining stable dividend distributions and dividend yield, even during periods of market stress.

In this blog, we explore what the impact would be if a quality factor were added to a dividend strategy. For the analysis, we used the S&P 500® Quality High Dividend Index, which is designed to measure the S&P 500 companies that rank among the top 200 in terms of their quality scores and dividend yield.[3] We then compared this strategy against the pure dividend yield, dividend growth, quality, and dividend and low volatility strategies, which are represented by the S&P 500 High Dividend Index, S&P 500 Dividend Aristocrats, S&P 500 Quality Index and S&P 500 Low Volatility High Dividend Index.

Over the long-term investment horizon, all of the dividend-oriented strategies outperformed the S&P 500 on both an absolute return and relative return basis, with the quality and dividend strategy leading the outperformance (see Exhibit 1). Specifically, the quality and dividend strategy outperformed the S&P 500 by 5.42% per year, with an annualized total return of 11.04% versus 5.62% during the past 20 years. The quality and dividend strategy held up relatively well in all market environments, with an average monthly excess return of 0.28%, which was the highest among all the strategies.

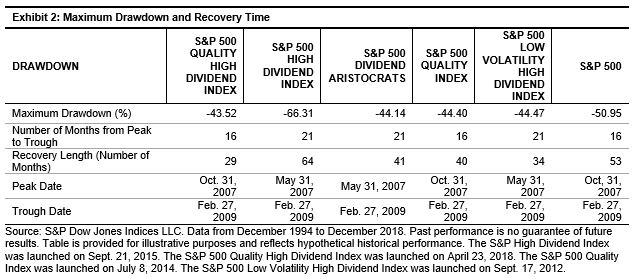

Adding quality or volatility filters to a dividend strategy allowed for quicker recovery from the bear market. During the 2008-2009 financial crisis, when all of the yield strategies experienced losses and drawdowns, the data showed that the quality and dividend combination had the smallest drawdown and quickest rebound (see Exhibit 2). The strategy recovered from the financial turmoil within 29 months, versus 53 months for the overall stock market. Meanwhile, the pure dividend yield strategy, as measured by the S&P 500 High Dividend Index, took the longest time to recover.

As displayed in Exhibit 3, the quality and dividend strategy sustained an average dividend yield of 2.92% historically, compared with 1.76% for the S&P 500. While the S&P 500 High Dividend Index historically had the highest dividend yield of 4.47%, it also exhibited the lowest quality traits among all the dividend strategies. As expected, the strategies that incorporated the quality factor demonstrated much stronger quality characteristics.

Dividends are one of the most important drivers in generating investment returns. As we analyzed in this blog, dividend-focused strategies have historically exhibited better long-term outperformance over the market. In addition, when combined with factors such as quality or low volatility, dividend strategies can potentially achieve higher returns and shorten recovery time from bear markets. Specifically, integrating quality and dividend helped generate the highest overall excess return, shortest rebound time, and the highest quality characteristics without sacrificing the yield over the period studied.

[1] Source: ETF.com; FactSet.

[2] Quality definition by S&P Dow Jones Indices:

We define quality as the combination of profitability, earnings and financial robustness, and use return on equity, accruals ratio, and financial leverage ratio to represent these factors.

- Return on equity (ROE): Indicator of a company’s profitability. ROE is computed as [trailing 12-month earnings per share/book value]

- Accruals ratio: Indicator of a company’s operating performance. It is computed as [change of net operating asset over past 1-year/average of net operating assets over past two-year period]

- Financial leverage ratio: Indicator of a company’s capability in meeting its financing obligations. It is computed as [total debt/book value].

[3] An S&P 500 member company is selected as a constituent if it ranks within the top 200 of the index universe by quality score and ranks within the top 200 of the index universe by indicated annual dividend yield. To reduce sector concentration risk and overall volatility, the stocks are weighted equally and sector weight is constrained at 25%.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

The S&P Pure Style Indices include only securities that exhibit either pure growth or pure value characteristics. Due to this, there are no overlapping securities between the pure growth and pure value indices. The concentrated exposures of the S&P Pure Style Indices potentially present them as better candidates for market participants looking to have precise tools in their investment process.

The S&P Pure Style Indices include only securities that exhibit either pure growth or pure value characteristics. Due to this, there are no overlapping securities between the pure growth and pure value indices. The concentrated exposures of the S&P Pure Style Indices potentially present them as better candidates for market participants looking to have precise tools in their investment process.