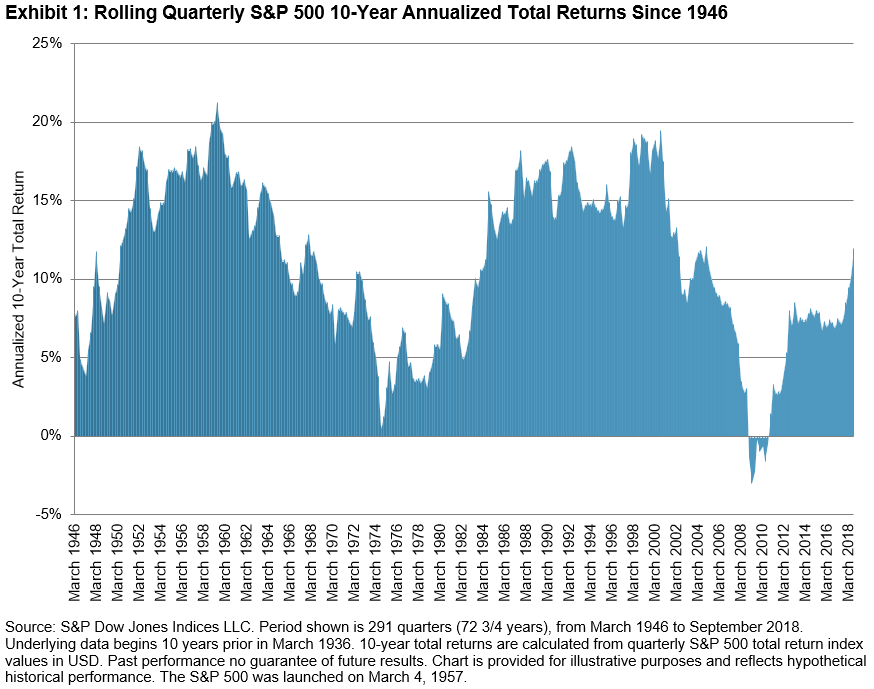

In this bull market, by some measures the longest running in U.S. history, investors may wonder what its prospects for continuation are. Judging by rolling quarterly 10-year annualized returns, the S&P 500® does not necessarily seem over-extended. As Exhibit 1 shows, since the end of World War II, large retracements followed lengthy periods of greater-than-10% annualized total returns with significant sub-periods north of 15% per year. The median 10-year annualized total return over the entire post-war period was 11.08%. As of Q2 2018, it was 10.17%, its first quarterly value greater than 10% since Q1 2005. As of Q3 2018, it rose to 11.97%.

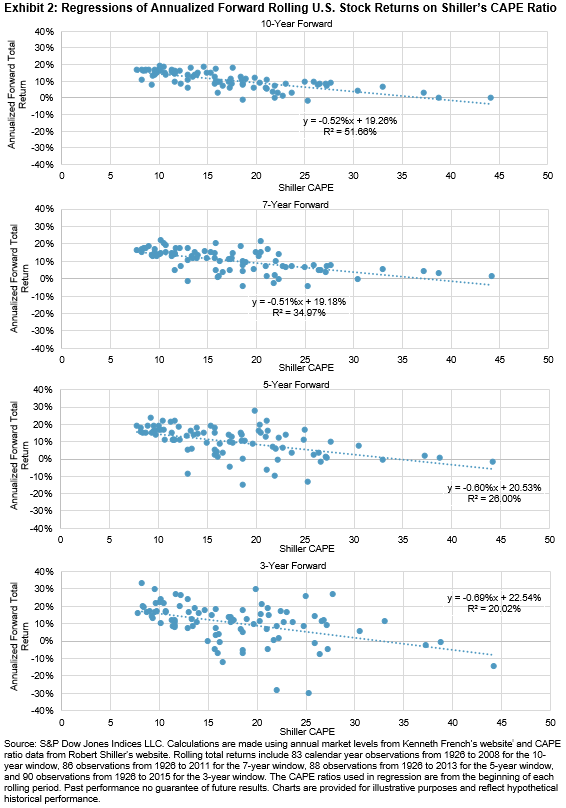

On the other hand, backward-looking valuation measures, such as Shiller’s CAPE ratio, paint a less sanguine picture. They generally indicate the market is fully valued, if not over-extended. Exhibit 2 shows 4 regressions of 10-, 7-, 5-, and 3-year forward-looking annualized returns on the CAPE ratio. The explanatory power of the linear regression increases with window length. For example, R2 of the 10-year forward returns is almost 0.52, while R2 of the 3-year forward returns is barely over 0.20. The data are clustered more tightly around their respective regression lines as the forward-looking period grows longer. There is too much random variability to use CAPE as a short-term timing tool, however over longer periods its relationship with future returns grows more significant.

Plugging in the current observed CAPE of about 33ii into the regressions shows that it is signaling low expected returns. For example, using the 10-year regression equation we have:

-0.52% (33) + 19.26% = 2.10%

After inflation, a nominal return of about 2% would probably equate to a near-zero, or even negative, average real return over the coming 10 years.

Nonetheless, backward-looking data may currently be less representative of the future than before. On the positive side for U.S. corporate profits, tax cuts have juiced earnings. But an important question is whether earnings can remain elevated relative to the economy, or whether they have peaked. There is also significant uncertainty about the outlook for global trade, and the prospect that U.S. monetary policy may work at odds with fiscal policy. Therefore, market participants may benefit from incorporating a wide degree of variability into their capital market return expectations. “Moderation” is probably a good word to bear in mind when considering reasonable expectations for U.S. stocks, while granting plenty of room for both downside and upside surprises.

i French, Kenneth. http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html

ii As of Oct. 2, 2018 CAPE was reported on Robert Shiller’s website at 33.18. See http://www.econ.yale.edu/~shiller/data.htm

The posts on this blog are opinions, not advice. Please read our Disclaimers.