In a prior blog, we demonstrated that a sector-relative, carbon-efficient portfolio was superior to a sector-unconstrained one when forming low-carbon portfolios. In this blog, we explore the integration of carbon risk in quality factor portfolios. High-quality companies seek to generate higher profitability and enjoy more stable growth than “average” companies. Equally important, high-quality companies seek to adopt a conservative, yet effective, capital structure that allows them to grow. Finally, high-quality companies tend to exercise prudence in the administration of company affairs.[1]

We capture the quality investment style by equally weighting three factors: financial leverage ratio, return on equity (ROE), and balance sheet accruals ratio.

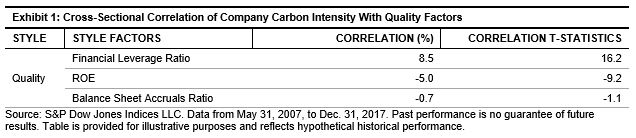

Correlation of Carbon Intensity and Quality Factors

We first analyzed the firm-level correlation between carbon intensity and each of the three quality factors in our test universe for each rebalance period (every three months), then we took the average of the cross-sectional correlations and calculated the t-statistics (see Exhibit 1).[2]

We can see that companies that are more carbon-efficient (or have lower carbon intensity) tended to have lower financial leverage ratios while displaying higher ROE, both of which were statistically significant at a 95% confidence level. In sum, carbon-efficient firms tended to be high-quality companies. Such findings are not surprising, as high-quality companies have more prudent capital structure, higher profitability, and higher earnings quality than their competitors. As a result, high-quality companies may have the financial strength to meet the market obligations that come with moving toward a low-carbon economy.

Integrating Carbon Risk With Quality Portfolios

One way to incorporate carbon risk with the quality factor is to construct an integrated quality-carbon composite score. The quality style score is defined as the equal-weighted combination of the three quality factors, while the quality-carbon composite score is defined as the equal-weighted combination of the quality style score and the carbon-efficiency score. Quintile portfolios were constructed based on the integrated quality-carbon composite score.

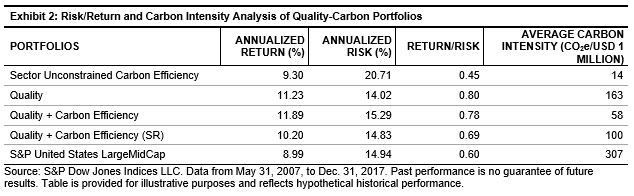

We compared the hypothetical quality-carbon-integrated portfolios (quality + carbon efficiency and sector-relative (SR) quality + carbon efficiency) to the unconstrained carbon-efficient portfolio, the quality portfolio, and the underlying benchmark (see Exhibit 2).

The quality + carbon efficiency portfolio had slightly lower risk-adjusted returns (0.78) than the quality portfolio (0.80). However, the carbon intensity of the quality + carbon efficiency portfolio was reduced to 19% of the underlying universe. The sector-relative quality + carbon efficiency portfolio also outperformed the benchmark on a risk-adjusted basis, albeit with a lower Sharpe ratio than its quality and quality + carbon efficiency counterparts.

Integrated Quality-Carbon Portfolios Maintained Target Factor Exposure

In this section, we examine the quality style exposure of integrated quality-carbon portfolios. We compared the weighted average style z-score of the integrated portfolios to the pure factor portfolio, as well as the broad benchmark (see Exhibit 3).

We can see that combining carbon efficiency with quality portfolios had little impact on quality style exposure, as measured by the weighted average z-score and t-statistics (the critical value of 95% confidence level is 1.99) from two sample t-tests.

The results from Exhibits 1, 2, and 3 showed that carbon-efficient firms tend to be high-quality companies. Moreover, integrated quality-carbon-efficient portfolios tend to have improved risk-adjusted returns and tend to be more carbon efficient over the underlying benchmark, while maintaining similar factor exposure level in comparison with pure quality factor portfolios. In the next blog, we will explore sector composition, risk exposure, and risk composition of quality-carbon-efficient portfolios.

[1] D. Ung, P. Luk, and X. Kang. “Quality: A Distinct Equity Factor?” 2014. S&P Dow Jones Indices LLC.

[2] B. Hao, A. Soe, and K. Tang. “Carbon Risk Integration in Factor Portfolios.” 2018. S&P Dow Jones Indices LLC.

The posts on this blog are opinions, not advice. Please read our Disclaimers.