Factor tilts have resulted in divergent dividend strategy performance following the November elections

November’s US elections have buoyed investor optimism about the potential for tax reform, increased infrastructure spending, reduced regulation and accelerating economic growth. These expectations led to a 0.75% spike in the 10-year Treasury yield between Nov. 8 and Dec. 16, and a 5.2% increase in the US dollar, as measured by the US Dollar Index.1

Still, by historical standards, interest rates remain low. Nearly a decade ago, the 10-year Treasury yield finished 2007 at 4.02%; it now stands near 2.50%.1 When adjusted for inflation, even the 0.75% bump in the 10-year Treasury yield amounts to a modest 0.40% increase. Compare that with the average annual real (inflation-adjusted) increase in the 10-year Treasury yield between January 1962 and November 2016 of 2.40%.1

Shouldn’t dividend stocks be underperforming?

Global demand for dividend-paying exchange-traded funds (ETFs) is strong, as evidenced by robust flows of over $20 billion in 2016; US-based ETFs accounted for more than half of that amount.1 The appeal of dividend-paying stocks is clear, as dividends can help provide a nice offset to rising inflation, while most fixed-coupon debt cannot hedge against rising prices.

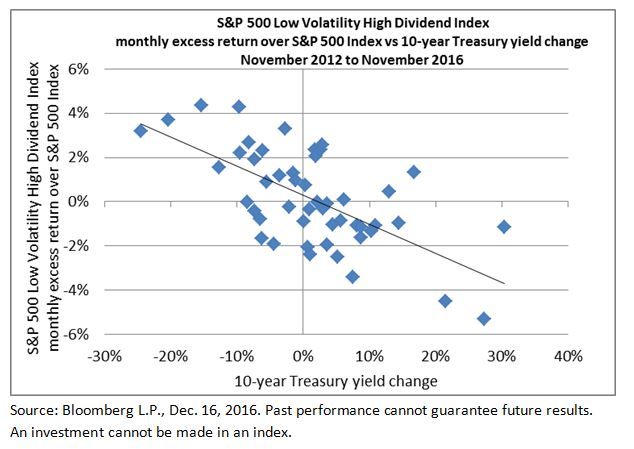

Nonetheless, the timing of recent gains is counterintuitive; typically, rising interest rates cause dividend-paying shares to lag. This is because yield-seeking investors tend to trade out of dividend stocks and into bonds when interest rates rise. This can be seen in the chart below, which depicts the relationship between the excess monthly return of dividend-paying stocks (represented by the S&P 500 Low Volatility High Dividend Index relative to the S&P 500 Index) to the monthly change in the 10-year Treasury yield. Note the inverse relationship, with higher yields creating a drag on the excess returns of dividend payers.

Dividend stock performance running contrary to long-term trends

With yields rising, dividend stocks are bucking this long-term trend, although performance has varied by index. Following the Nov. 8 election through Dec. 16, the S&P 500 Low Volatility High Dividend Index lagged the S&P 500 Index by only five basis points, returning 5.76%, while the NASDAQ US Dividend Achievers 50 Index outpaced the S&P 500 Index by 3.20%, returning 9.01%.1 These counterintuitive returns may have investors wondering about the reasons behind the results.

One way to analyze portfolio returns is through factor exposure. Both the S&P 500 Low Volatility High Dividend Index and the NASDAQ US Dividend Achievers 50 Index are dividend-based indexes, but each has different factor tilts beyond just dividends, which can affect performance.

Let’s take a closer look:

- The S&P 500 Low Volatility High Dividend Index has a value factor load of 0.51 and a growth factor load2 of -0.60, meaning that it is more of a value-oriented index than a growth index.1 Keep in mind that value stocks outperformed growth stocks following the election. From Nov. 8 through Dec. 16, the S&P 500 Value Index rose 8.66%, compared with 5.81% for the S&P 500 Index and just 3.07% for the S&P 500 Growth Index, which helps explain the strong performance of the S&P 500 Low Volatility High Dividend Index.1 Put another way, meaningful value exposure and negative growth exposure helped to mute the impact of rising rates – boosting index performance.

- By contrast, the NASDAQ Dividend Achievers 50 Index did not have material value exposure, but did have negative exposure to the growth factor (-0.43). More importantly, the index had a negative factor load (-0.90) to large-cap stocks, with 44% of its holdings in smaller-cap stocks.1 Thus, with the S&P SmallCap 600 Index outpacing the large-company S&P 500 Index by 10.35% from Nov. 8 through Dec. 16, the strong performance of the NASDAQ Dividend Achievers 50 Index is no great mystery.1

Factor exposure matters

To reiterate: While dividend-paying stocks may have surprised investors with their robust performance in the face of rising interest rates following the Nov. 8 election, much of this performance can be explained by factor tilts. In this case, exposure to value and smaller-cap stocks helped mitigate the impact of rising interest rates. As you can see, factors are not only valuable building blocks for constructing portfolios, but also useful tools for gauging portfolio performance.