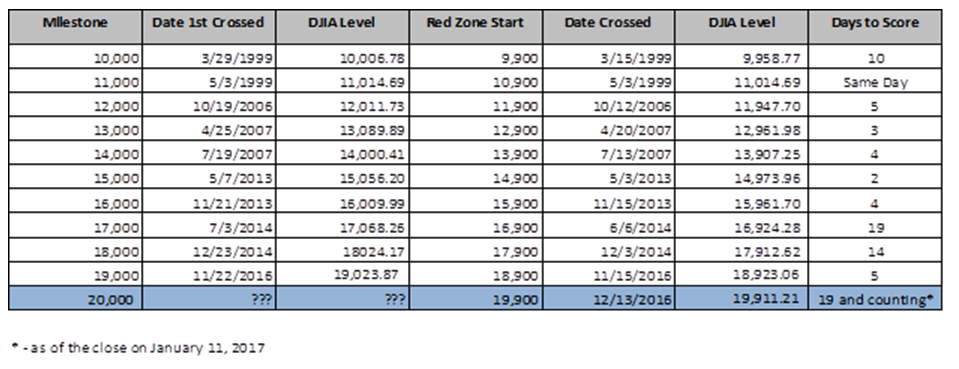

In grid-iron football, The Red Zone refers to the area between the 25 yard line and the goal line, the last remaining ground the offense must battle through in order to score a touchdown. This is a somewhat apt metaphor for what we’re currently witnessing with the Dow Jones Industrial Average.

Unless you’ve been living under a rock these last few weeks, you are no doubt aware that The Dow has been closing in on, yet remaining tantalizingly short of, the 20,000 level. Coming as close as a mere .37 points during the Friday, January 6 session, as of this writing the DJIA has yet to record its first close past this vaunted milestone.

Investors and the market commentariat have been teased with the event for days, but the 20k level has thus far remained resistant to breach. More specifically, it’s the last 100 points – the distance from 19,900 to 20,000 – that has proven to be such stubborn ground to cover. Why? Even if I could, I won’t answer that here – better-informed market participants can speak into that analysis. But I can say that the DJIA’s current Red Zone campaign just became the most protracted of recent major milestones.

Listed in the table below is the number of trading days it took the DJIA to move through that last 100 points leading up to round, 1,000 point increments. As of today’s close, which was again found wanting, we find ourselves 19 days into this journey. Thus, even if we hit our target tomorrow, it will have taken the DJIA 20 sessions to cover the last 100 points – longer than the ten 1,000 point campaigns that preceded it. On average, it has taken less than 7 trading sessions to cover that distance during recent memory.

How much longer? As William Faulkner said, “And sure enough even waiting will end…if you can just wait long enough.” A quote from Vince Lombardi might be more appropriate here but, hey, this was the best I could find.