After starting last week at a yield of 2.52%, the yield of the S&P/BGCantor Current 10 Year U.S. Treasury Bond Index climbed to a high of 2.72% to close the index before the July 4th holiday. The 6.1% unemployment number moved yields higher as the markets were expecting an unchanged result from the prior level of 6.3%. Indicators of a strengthening economy have market participants speculating as to the timing of a possible Fed rate increase.

Investment grade municipal bonds as measured by the S&P National AMT-Free Municipal Bond Index were down on the week having returned -0.37%, though on the year are returning 5.52%. All eyes have been on Puerto Rico and its developing events as the S&P Municipal Bond Puerto Rico Index whose year-to-date return was at a high of 10.65% at the end of June has now dropped to a -0.16%.

Last week high yield as measured by the S&P U.S. Issued High Yield Corporate Bond Index gave up very little ground and continues to return 5.51% year-to-date. Over the same time frame, the S&P U.S. Issued Investment Grade Corporate Bond Index dropped -0.72% month-to-date and its year-to-date return had moved from 5.59% at the start of the month down to 4.82%. Both markets experienced plenty of new issuance as investment grade names such as Anadarko Petroleum, Goldman Sachs and Oracle, along with the high yield names of Ithaca Energy, Jaguar and RJS Power all issued debt last week.

Consistently yielding 4.35%, the S&P/LSTA U.S. Leveraged Loan 100 Index returned +0.12% month-to-date in comparison to the similar credit of high yield which was down -0.04%. Year-to-date the shorter life senior loan market lags behind the longer duration high yield by only having returned 2.59% year-to-date.

A light economic calendar this week as the bond market and its participant’s kick the start of the vacation season into full gear. Though smaller releases will occur Tuesday, Wednesday’s Fed release of the June 17th / 18th meeting along with MBA Mortgage Applications (-0.2% prior) should grab some attention. Initial Jobless Claims are expected to be unchanged at 315k, while Wholesale Inventories month-over-month for May is expected to be 0.6% versus the prior 1.1%. A true summer Friday is expected as the only release for the day will be June’s monthly U.S. Treasury Federal Budget Debt Summary number which is surveyed to be an $80 billion surplus. In addition to weekly bill auctions, the U.S. Treasury will be auctioning $27 billion 3-years while also tapping $21 billion 10-years and $13 billion 30-years.

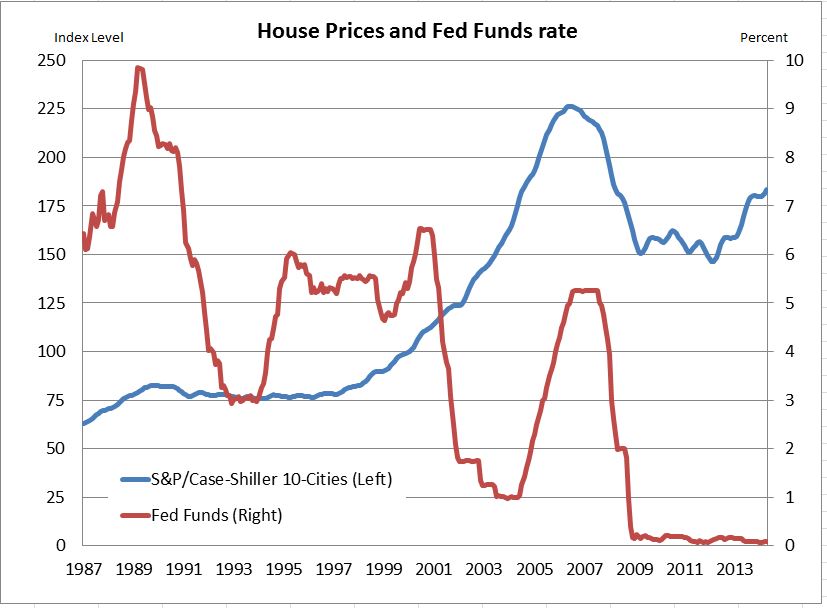

Source: S&P Dow Jones Indices, Data as of 7/3/2014, Leveraged Loan data as of 7/6/2014.

The posts on this blog are opinions, not advice. Please read our Disclaimers.