The Bank of Canada left its key interest rate unchanged at 0.5% last Wednesday, Sept. 9, 2015. The message from the central bank was that it could be “considerable time” before there is significant recovery from the collapse of oil prices that pushed the economy into a technical recession. The last rate cut was back on July 15, 2015, and the central bank feels the effects of that action are still working their way into the economy. The number of jobs is also an important factor to watch. The Canadian economy added 12,000 jobs in August and exports were up for the second month in a row, but the unemployment rate also rose to its current level of 7%.

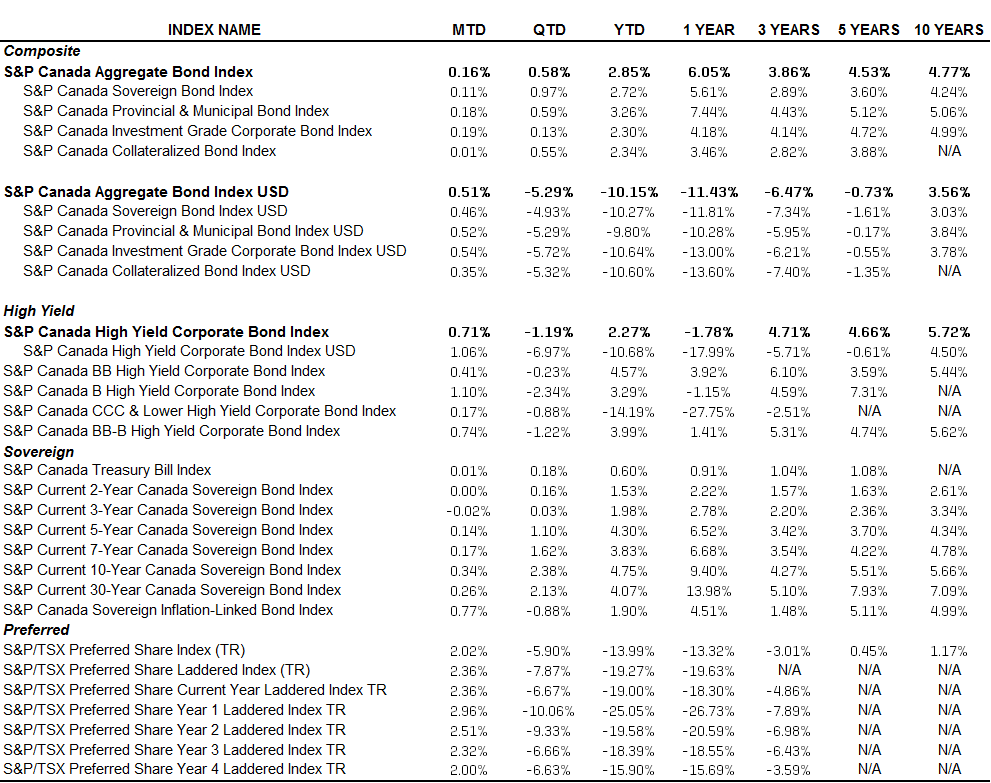

So far, September has been positive for Canadian indices, as Exhibit 1 indicates. Bonds rated CCC and lower have returned 0.17% for the month, while they have lost 14.19% YTD, as of Sept. 15, 2015. The S&P Canada CCC & Lower High Yield Corporate Bond Index was as low as -18.36% YTD as of Aug. 20, 2015, before recovering to the level seen as of Sept. 14, 2015. The S&P Canada B High Yield Corporate Bond Index, which measures single B bonds, had a total return as high as 5.84% YTD at the beginning of July, but as of Sept. 14, 2015, it has returned 3.29% YTD after bouncing back from a 1.71% YTD return on Aug. 25, 2015.

Exhibit 1: Canadian Indices Returns

Source: S&P Dow Jones Indices LLC. Data from Sept. 14, 2015. Past performance is no guarantee of future results. Table is provided for illustrative purposes.

The posts on this blog are opinions, not advice. Please read our Disclaimers.