We have heard for many years now about the Chinese super-cycle that supported commodity prices since 1999 and we have also heard many debates about whether it has ended. So if it has ended what now? How huge is the impact on commodity prices?

That all depends on the level of inventories that result from the combination of supply and demand. Theoretically if there were no inventories or supply, it wouldn’t matter how much Chinese demand fell. They could demand all they wanted but there would be no price impacts if there were no supply or inventories. Realistically this is not the case but there are shortages in various commodities, so the slowdown in Chinese demand growth matters more for some commodities than others.

Another point to remember is that Chinese demand does not slow equally in all areas. Construction, automobile demand and food demand all require different natural resources, so it is understandable that copper, palladium, gasoline and soybeans may not move together. China has also been known to stockpile resources at various times, which may influence the available inventories like in cotton last year.

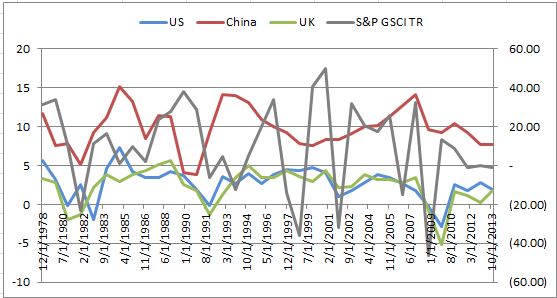

First let’s take a look at the slowdown in GDP growth from China. In 2013 the growth was 7.7%, roughly the same as in 2012, which is also close to 1998-99 levels and almost half as much as in 2007 when it was 14.2%. There is no correlation (0.04) between the total returns of the S&P GSCI and Chinese GDP growth, while there is only slightly positive correlation of the commodities to the GDP growth of the US at 0.23 and UK at 0.30.

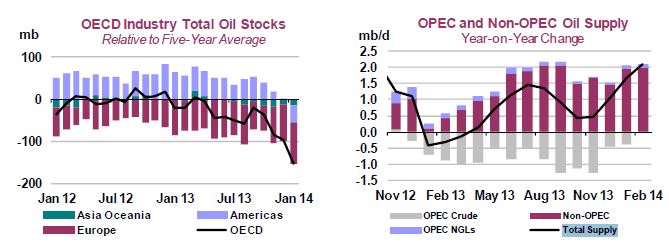

Further, let’s take a look at the supply and demand situations a few of the mainstay commodities. According to IEA’s March Oil Market Report, although the OPEC and Non-OPEC supply has increased roughly 2 mb/d yoy, it is against a backdrop of staggering inventory draws from a cold snap in the US. From this, the oil stock deficit to the seasonal average is at 154 mb, its widest in more than a decade.

Now let’s evaluate the demand side of oil, and again, what does a slowdown in Chinese demand mean? It depends on the commodity, even within the oil complex. For example gasoil has had the slowest growth yoy in 2013 of -1.6% and 2.5% (projected by the IEA) in 2014 since the demand for transporting coal has dropped. This translated into 54 kb/d coming off demand in 2013 but 83 kb/d coming back on in 2014 (projected by the IEA). However, gasoline demand has been relatively strong with a 6.5% growth in 2013 and 6.2% (projected by the IEA) in 2014 adding up to 129 kb/d in each year of 2013 and 2014 fueled by car sales.

Chinese demand also is relative to the rest of the world. They still have the highest demand growth in the world for oil and even if it is slowing, they are still consuming an additional 344 kb/d in 2014 (projected by the IEA) after a 278 kb/d incremental increase in 2013. The 344 kb/d is less than half of the consumption of the top 10 consumers in the world that the IEA projects will consume 834 kb/d more in 2014. It is actually the slowdown in the US which should be highlighted, where the demand growth is slowing the most, dropping to just 0.5% growth adding just 96 kb/d only behind Japan and Korea in 2014 (according to the IEA). The world should also watch demand coming from India, Russia, Brazil and Saudi Arabia, which taken together are more powerful than China on the demand front with an IEA projection of an additional 364 kb/d in 2014.

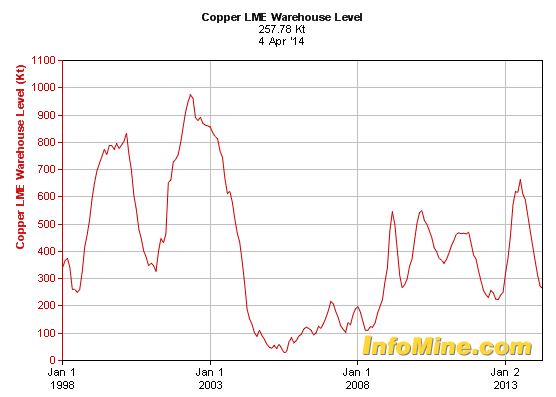

This is all interesting but oil is not the only commodity where the possible Chinese super-cycle bust doesn’t really matter. There are mixed impacts on copper, and as I have pointed out before, copper is not the best indicator of economic health. Currently inventories are at relatively low levels despite weaker Chinese demand.

Despite this inventory drop, the S&P GSCI Copper has fallen 9.05% this year. Undoubtedly, some of this loss is due to slower Chinese demand; however, more factors are at play. Copper is used as collateral for high risk loans where cash might not be available and the credit default caused a big scare. The bigger question surrounding copper’s future is probably around whether producers can deliver the supply they plan this year and whether Indonesia relaxes its export bans on copper concentrates.

This is evidence of the impacts of low inventories we have been seeing recently. Commodities this time around, in the new cycle, might not be primarily driven by the super-cycle of Chinese demand growth and may be more impacted by the supply side.

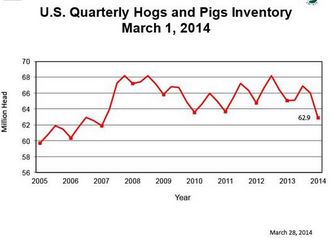

For further evidence, let’s examine the agriculture and livestock. Take a look at the chart below of hog and pig supply. A slowdown in Chinese demand is just not powerful enough to kill the virus driving the rally, where the S&P GSCI Lean Hogs is up 42.4% YTD.

The S&P GSCI Agriculture has also spiked this year, up 15.1% YTD. This has been mainly due to weather that shocked the supply, again outpacing the demand drop from China due to the ban on GMO corn. It’s interesting that in the recent USDA report on World Agricultural Supply and Demand Estimates the focus is much more on China as a supplier than a consumer. Despite this, Agweb pointed out that China is still the third largest importer of US corn and the USDA projects imports to triple from 236 million bushels in 2014/5 to 836 million bushels by 2023. Some say a similar pattern in soybeans could follow. That seems like super demand growth even with the end of a super-cycle.

The posts on this blog are opinions, not advice. Please read our Disclaimers.