For the first time, the main S&P DJI indices in Latin America have been analyzed by Trucost to reveal their exposure to a range of different carbon metrics that prudent investors may want to be aware of.

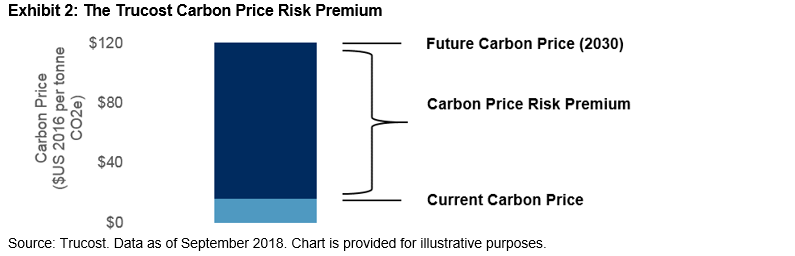

A central element of the analysis is the estimated portion of earnings that could be lost if the constituent companies were to absorb the additional cost of 2030 carbon prices for their operational emissions and purchased electricity. For the S&P/BVL Peru Select Index, this represents 19% of companies’ EBITDA—for the S&P/BMV IPC, this rises to 42%.

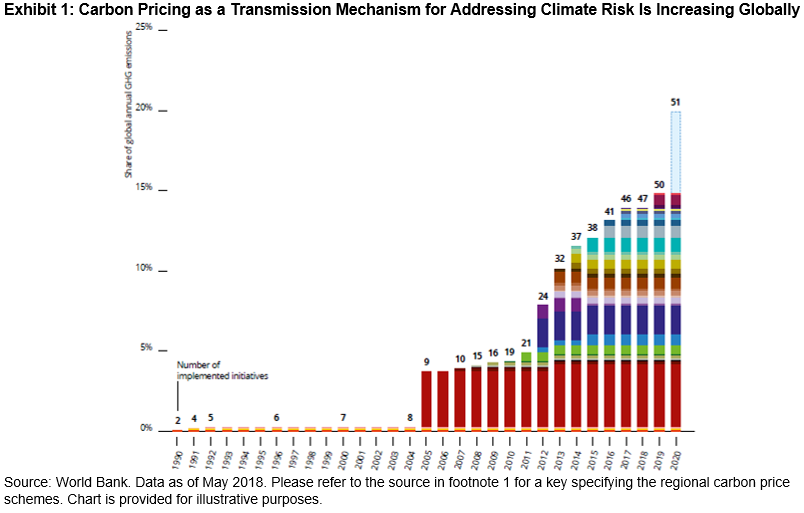

We know that outside death and taxes nothing is certain, but Brazil, Chile, Colombia, Mexico, and Peru have all signed the Paris Agreement—and have carbon targets in place. In Europe, where there are similar commitments, we have seen the price of carbon emissions rise fivefold over the last year.

With these cost implications, companies are being encouraged to report on such matters. In 2017, the G20 set up the Task Force on Climate-related Financial Disclosures, which provided guidance for consistent climate-related financial risk disclosures. Mexico’s government passed the General Law on Climate Change, which set forth requirements for mandatory measurement, reporting, and verification of corporate emissions and established the creation of a National Emissions Registry. In the UK, trustees must update or prepare their statement of investment principles to show how they account for financially material considerations arising from environmental, social, and corporate governance considerations, including climate change. In France, the energy and transition law requires not only companies to report, but also pension funds and investment managers.

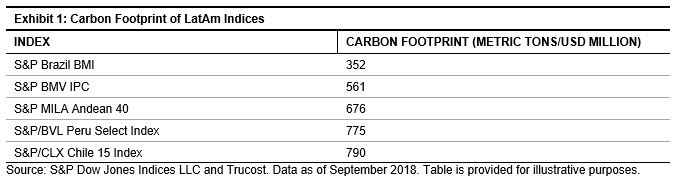

The carbon footprint of a company is determined by its direct emissions and those that come from supplier companies including purchased electricity. This is then normalized by USD 1 million in sales. This process can be aggregated to give a figure for a whole index. For the S&P Global 1200, a representative global index, that figure was 279 metric tons/USD million as of September 2018. For the Latin American indices, the figures are shown in Exhibit 1.

It is likely that a transition to a lower-carbon economy will present challenges for the countries of Latin America. For example, Mexico’s emphasis on trade makes its companies globally competitive. Its main industries include iron and steel, petroleum, automotive, chemicals, and food and beverages. However, these are industries with significant environmental impacts. If companies are to remain competitive, they will have to respond to the challenges and opportunities that a changing economic course presents.

Most investors expect governments to bring forward policies to reduce emissions—and these tend to involve increased costs. Even in the absence of strong government action, it is important for financial institutions to step up to the mark. They may want to prioritize acquiring more detail on sector exposure to natural capital risks. If banks and investors take into account natural capital in their decision-making processes, that in turn will tend to encourage companies to measure, manage, and improve their environmental performance for everyone’s benefit.

The posts on this blog are opinions, not advice. Please read our Disclaimers.