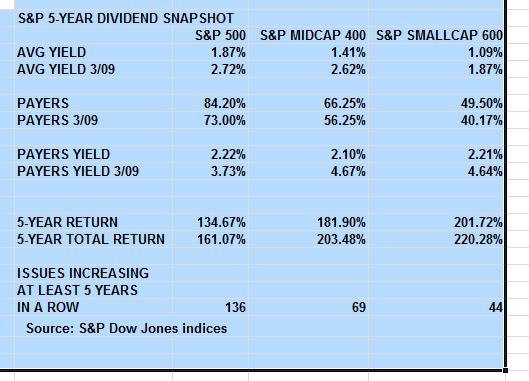

March marked the fifth anniversary from the Bear market low. Dividends have not only recovered from their bottom, but are setting new records. Yields are less, but relative to other instruments they remain competitive, and have a much lower tax rate. Two observations that became apparent are the risk-reward trade off and the yields. For the S&P indices, the large-cap market has more issues which pay a dividend and more issues which increase year-after-year. On a risk-reward note, the S&P 500 offers a higher yield, with a richer history of increases. However, that security of income comes at the cost of capital appreciation, with the S&P Small and Mid caps having returned more in stock price (and total return).