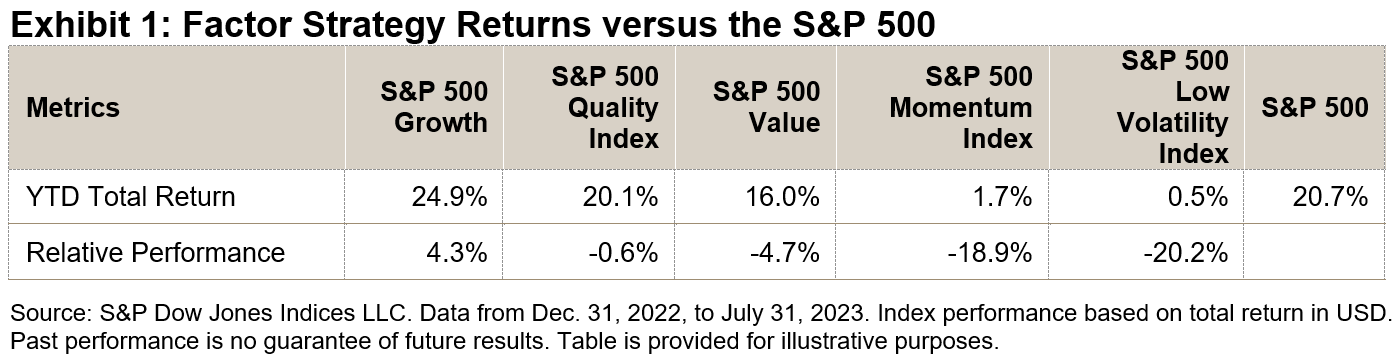

Thus far this year, about two-thirds of the S&P 500®’s rally has been driven by growth stocks and the so-called “Magnificent Seven” tech stocks. While the quality factor is traditionally viewed as defensive, it has kept pace with the market while many other factor strategies have underperformed (see Exhibit 1). Part of the reason for this is the focus on companies with solid fundamentals, which has been able to capture growth names that are financially strong.

Methodology Overview

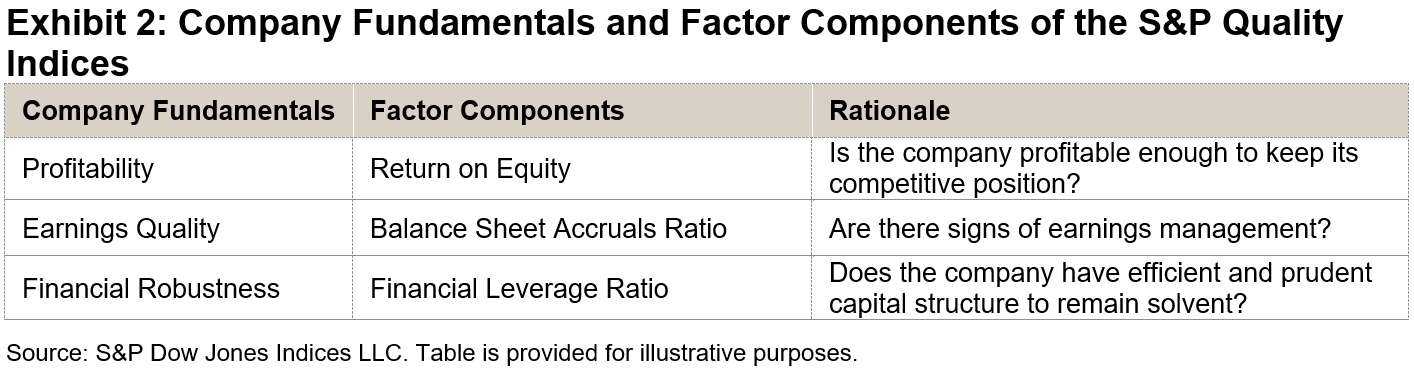

High quality is commonly associated with a company’s strong profitability, high earnings quality and robust financial strength. Hence, the S&P Quality Indices utilize three prominent metrics to capture a company’s quality characteristics (see exhibit 2): return-on-equity (ROE), balance sheet accruals ratio (BSA) and financial leverage ratio (FLR).

The selection for the S&P Quality Indices corresponds to the top 20% of eligible stocks within their respective universe, ranked by their overall quality scores. Index constituents are weighted by the product of their market capitalization and quality scores, subject to constraints.1

Performance Comparison

Historically, the S&P Quality Indices outperformed their corresponding benchmarks in the short and the long term with respect to total return and risk-adjusted return (see Exhibit 3). Year-to-date, the S&P MidCap 400® Quality Index and S&P SmallCap 600® Quality Index outperformed their benchmarks by 8.55% and 6.46%, respectively.

Additionally, these indices have tended to exhibit defensive qualities, as evidenced by lower volatility, lower beta and smaller drawdowns.

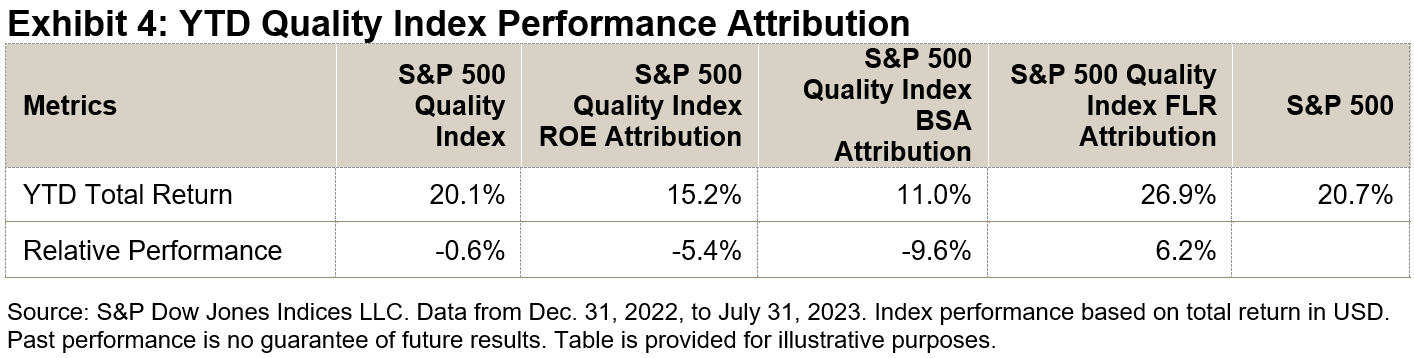

YTD Quality Index Performance Attribution

Thus far in 2023, the financial leverage ratio (FLR) component has significantly outperformed the S&P 500 (see Exhibit 4), suggesting that markets may have rewarded lower leveraged companies on the back of high interest rates.

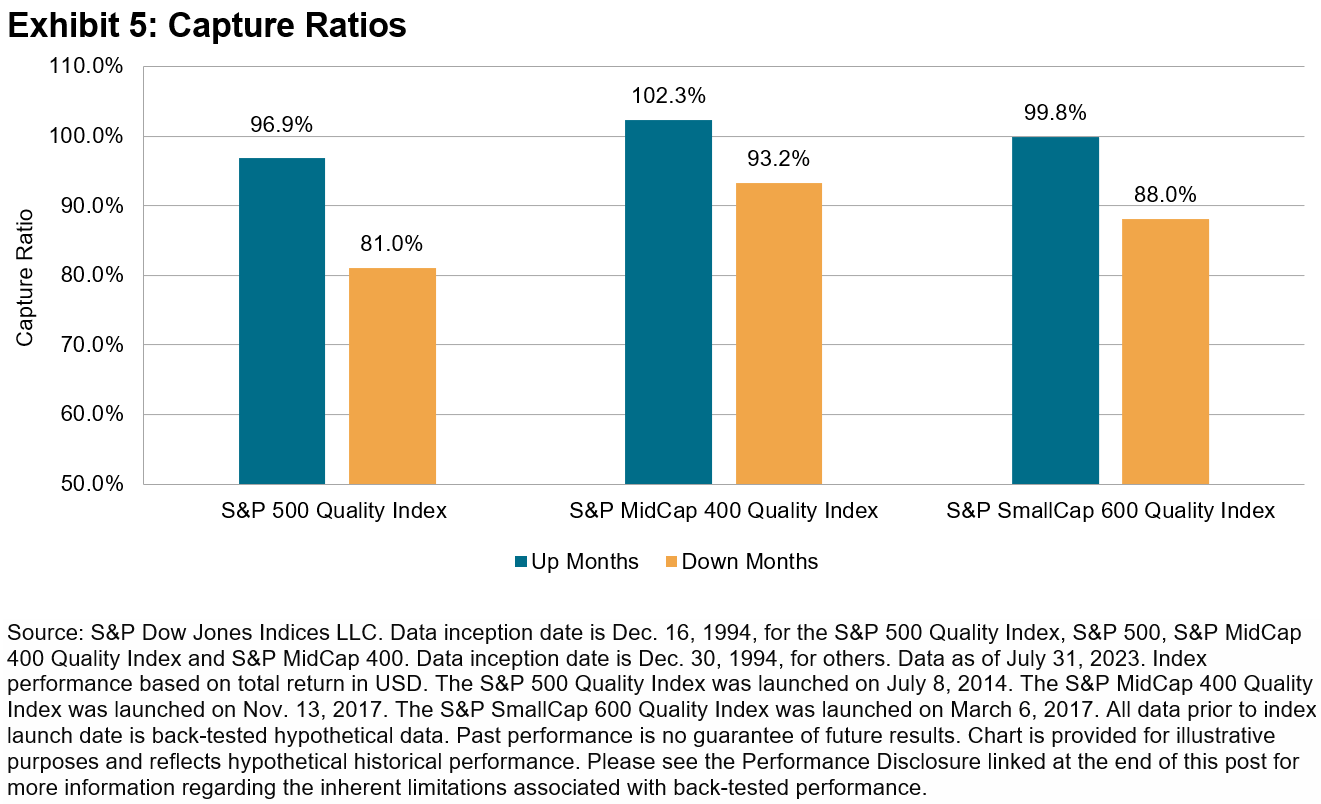

High Upside Participation and Defensive Characteristics

The historical capture ratios in Exhibit 5 show that the S&P Quality Indices tend to participate one for one in up markets2 while delivering significant outperformance during down markets. The defensive nature of these indices makes sense since the quality factor tends to track companies with durable business models and sustainable competitive advantages.

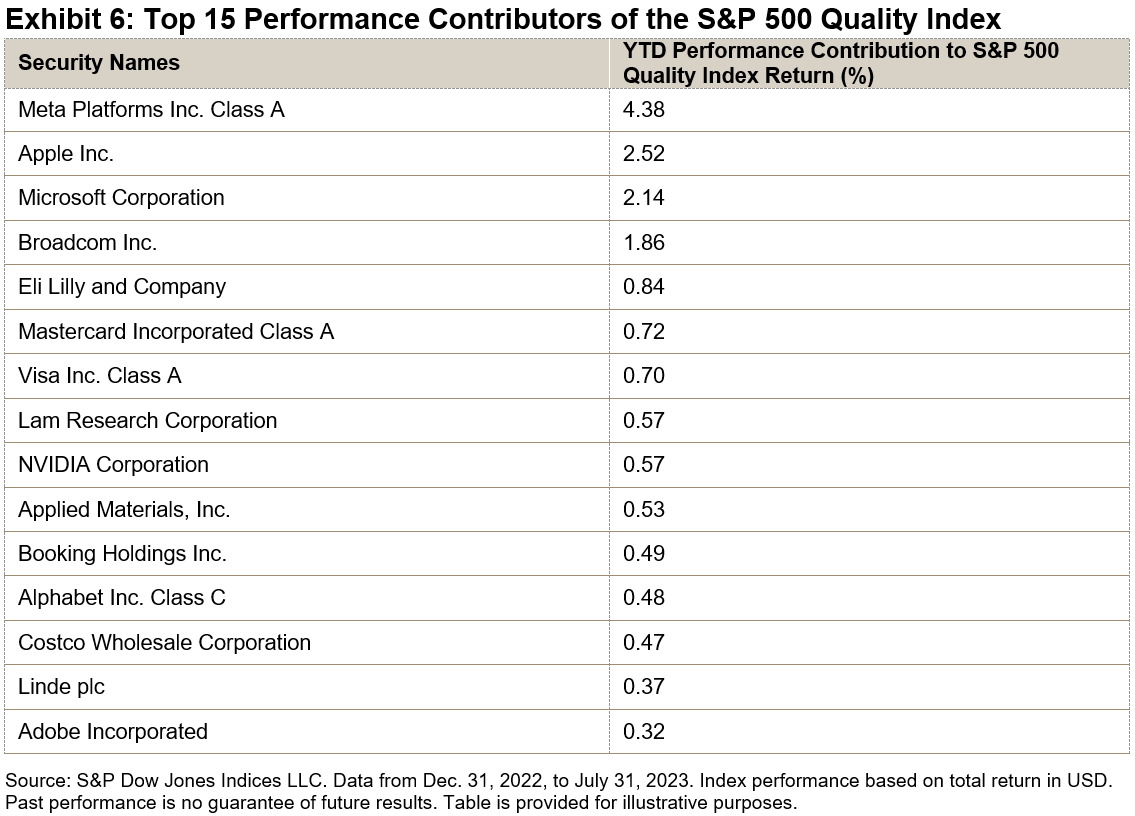

For the S&P 500 Quality Index, these capture ratios may be partially explained by the selection of mega-cap growth stocks, which tend to have strong financials and underlying business fundamentals. The recent constituents include five (Apple, Microsoft, Nvidia, Alphabet and Meta) of the Magnificent Seven. Exhibit 6 shows the top 15 contributors to the S&P 500 Quality Index’s performance YTD.

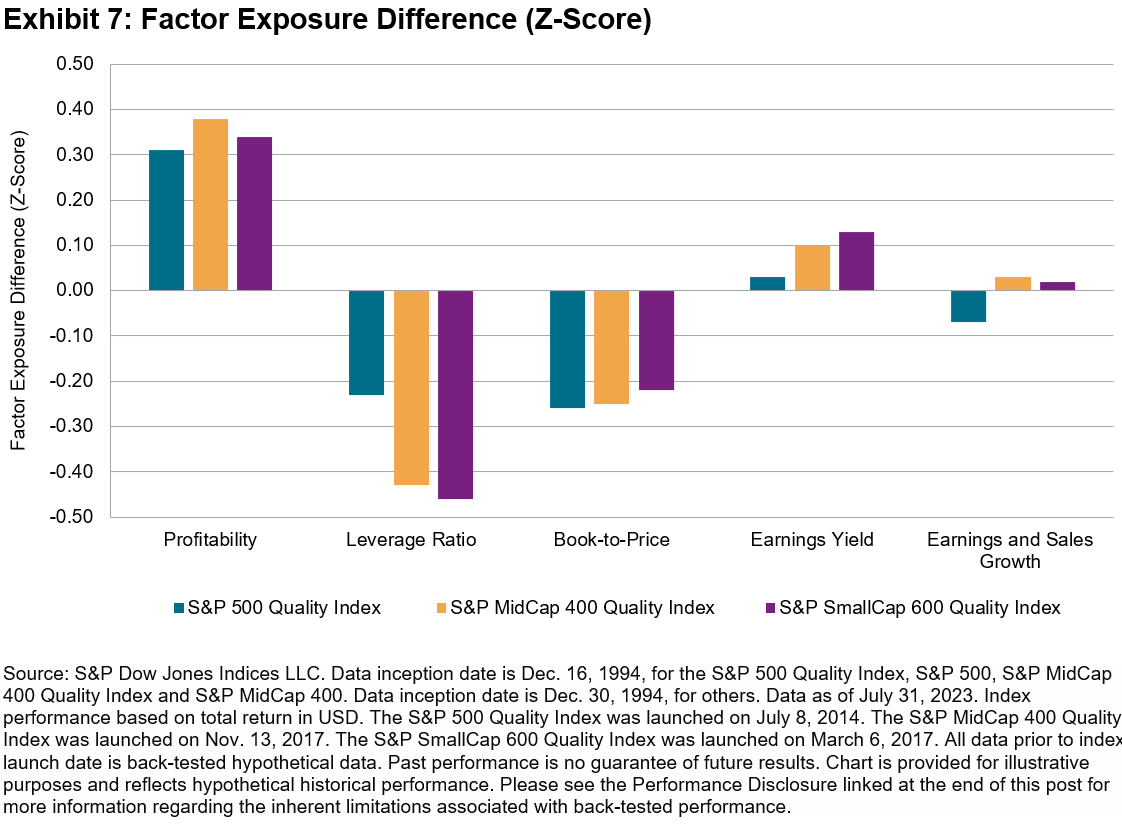

Factor Exposure

Exhibit 7 shows the factor exposure difference between quality indices and their benchmarks in terms of Axioma Risk Model Factor Z-scores. The S&P Quality Indices demonstrated a strong quality tilt versus their respective benchmarks. Specifically, the quality indices had higher exposure to profitability and lower exposure to leverage ratio factors. Additionally, the indices had similar valuation and growth exposures to their benchmarks.

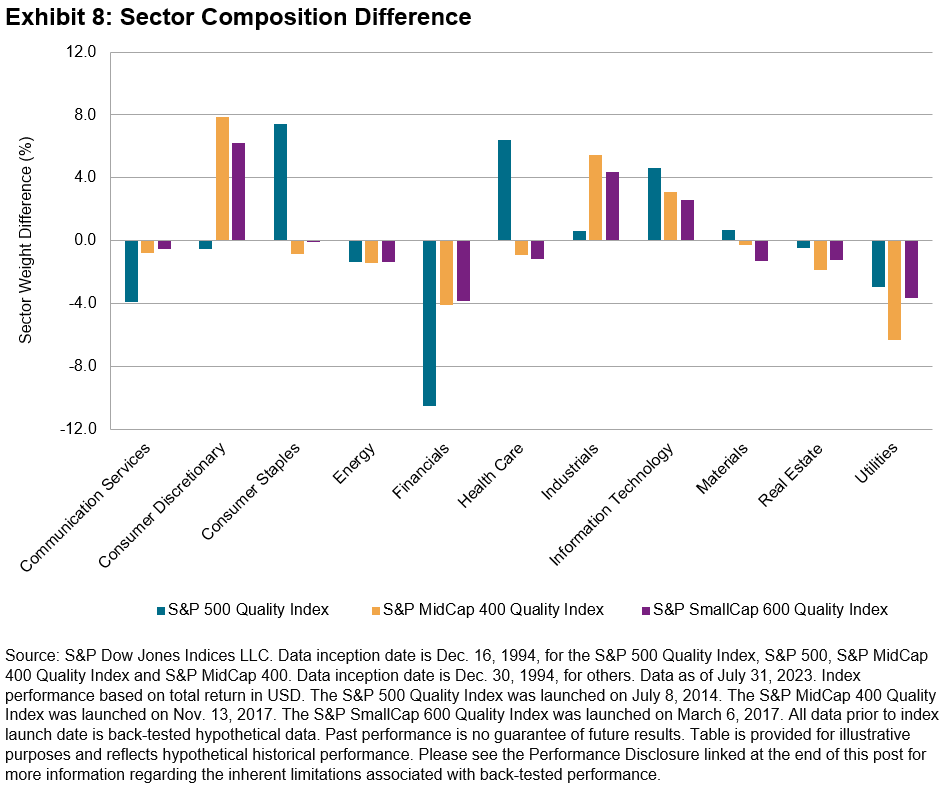

Sector Composition

Exhibit 8 shows the historic sector exposure difference between the quality indices and their benchmarks. Historically, the quality indices were overweight in Industrials and Technology, while underweighting Communication Services, Energy, Financials, Real Estate and Utilities.

1 For further information about the factor definition, factor score calculation and index design, please see the S&P Quality Indices Methodology.

2 The market is defined as the monthly performance of the underlying benchmarks from Dec. 31, 1994, to July 31, 2023.

The posts on this blog are opinions, not advice. Please read our Disclaimers.