The last few weeks have been challenging for business the world over. People working from home and aggressive social distancing have led to business contraction and the expectation of rising default. On March 19, 2020, an S&P report expected that the U.S. trailing 12-month speculative-grade corporate default rate would rise to 10% within the next 12 months, from 3.1% in December 2019.

In this blog, we aim to highlight how the S&P U.S. High Yield Low Volatility Corporate Bond Index,[1] by reducing volatility, has delivered better risk-adjusted returns in recent market turmoil.

Option-Adjusted Spreads (OAS): Screaming Market Volatility

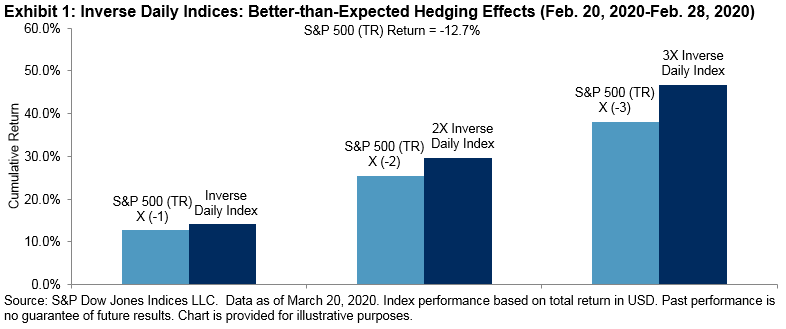

In 2020, high yield credit spreads traded stable at the tight end up until the first half of February, reflecting persistent yield chasing (see Exhibit 1). However, since then, global risk assets, driven by COVID-19 concerns, have sold off sharply. From Jan. 17, 2020, to March 23, 2020, the OAS for the S&P U.S. High Yield Corporate Bond Index widened by 719 bps from trough to peak, along with a 33% decline for the S&P 500® during the same time period.

S&P U.S. High Yield Low Volatility Corporate Bond Index: Lower Volatility, Better Long-Term Risk-Adjusted Returns

Exhibit 2 displays the comparative performance of the S&P U.S. High Yield Low Volatility Corporate Bond Index during the most stressed scenarios of the past two decades. There are two key takeaways.

- The S&P U.S. High Yield Low Volatility Corporate Bond Index outperformed its broad market high yield benchmark during each of these stress periods, including a 2.8% outperformance during the recent COVID-19 sell-off; and

- The defensive nature of the low volatility index has acted as cushion during market sell-offs.

Lastly, Exhibit 3 compares the return/risk trade-off among asset classes during 5-year, 10-year, and 20-year periods. There are several key points to be stressed.

- The S&P U.S. High Yield Low Volatility Corporate Bond Index consistently exhibited volatility levels lower than its broad-based high yield benchmark;

- In fact, its volatility levels fell between those of the investment-grade and high yield universes; and,

- For longer time periods (20 years), the S&P U.S. High Yield Corporate Bond Index delivered higher marginal returns than its broad-based high yield benchmark for every incremental unit of risk to investment-grade bonds.

Conclusion

There remains a lot of uncertainty surrounding the current pandemic. It remains to be seen how soon economic activity could start to pick up. Therefore, we might be looking at an extended period of time with an evolving and uncertain economic situation. All of this uncertainty leads to volatility and even more so for risky assets such as traditional high yield bonds.

During times of uncertainty and volatility, the S&P U.S. High Yield Low Volatility Corporate Bond Index provides exposure to high yield bonds with reduced volatility and the potential for higher risk-adjusted returns in the long term.

[1] For information about the methodology, please refer to https://spdji.com/documents/methodologies/methodology-sp-us-high-yield-corporate-bond-strategy-indices.pdf.

The posts on this blog are opinions, not advice. Please read our Disclaimers.