Human capital, physical capital, and technology have been widely recognized as a fundamental source of economic growth.[1] Dating back to the 1960s and early 1970s, when we saw a rapid increase in educated workers, facilities, and technological catch-up, Japan’s “economic miracle” emerged along with impressive GDP and per capita output growth.[2] Nowadays, these factors are the core of many countries’ policies to power their economies, including Abenomics’ three arrows. Consequently, one may infer that companies investing in capital expenditure (CAPEX), R&D, and human capital at a higher speed are more likely to generate long-term growth.

For investors, however, looking at the growth of investment in the three drivers alone is not enough. On the corporate level, companies should simultaneously be able to boost labor productivity, increase profitability, and generate returns out of those inputs. In this sense, efficiency is the key to linking these three economic drivers to investors.

The JPX/S&P CAPEX & Human Capital Index is designed to track companies that not only proactively investing in human capital, physical capital, and R&D, but also can demonstrate efficient use of those investments. The index selects the 200 companies with highest composite CAPEX and human capital scores from TOPIX constituents after passing liquidity, creditworthiness, profitability, and beta filters.[3]

CAPEX and R&D

The JPX/S&P CAPEX & Human Capital Index targets companies with a strong growth CAPEX and R&D expenditures. Compared with the broad market, represented by the S&P Japan BMI, the JPX/S&P CAPEX & Human Capital Index steadily maintained a higher CAPEX and R&D expense growth ratio over a five-year period (see Exhibit 1).

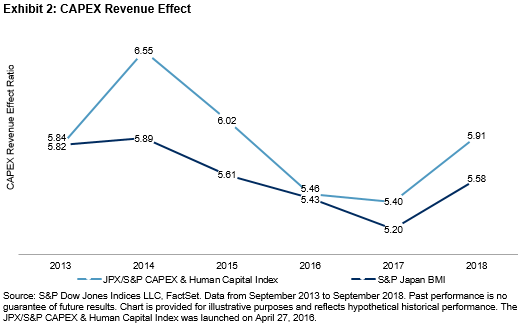

Meanwhile, it is crucial for a company to be financially disciplined and undertake worthwhile projects to avoid the pitfall of overinvesting and “empire-building.”[1] The index measures investment efficiency by allocating more weight to companies with a high ratio of revenue to three-year cumulative CAPEX (see Exhibit 2).

Human Capital

The JPX/S&P CAPEX & Human Capital Index utilizes RobecoSAM’s Corporate Sustainability Assessment (CSA) to evaluate three people-related areas: human capital development, talent attraction and retention, and gender equality and human rights. These areas focus on quality activities that can increase productivity, such as employee training, career planning, and equality and respect in the workplace, rather than merely counting the salaries paid to employees as a human capital investment.

The RobecoSAM CSA emphasizes the efficiency of human capital investment by giving a higher score to companies that are able to:

- Track and report quantitative measures of its training and development programs;

- Effectively explain the link between its development programs and the impact on its business; and

- Quantify the economic benefits of its human capital investments and demonstrate higher economic value from these investments over time.

Additionally, companies promoting gender equality are likely to rank higher, and ways they can promote this include having a larger female share of the total workforce and working to lower the wage difference between female and male employees.

In the long run, it is reasonable to believe that companies committed to cultivating, promoting, and protecting their employees could experience higher labor productivity, which in turn, can drive better stock performance.

Performance

The JPX/S&P CAPEX & Human Capital Index outperformed the benchmark TOPIX over 1-, 3-, 5-, and 10-year time horizons in terms of absolute and risked-adjusted returns. Since its launch in 2016, the JPX/S&P CAPEX & Human Capital Index has outperformed the benchmark by 0.86%.

[1] Tang, K (2015). “Considering Capex Efficiency.” S&P Dow Jones Indices.

[1] Solow, R. M. (1956). A contribution to the theory of economic growth. The quarterly journal of economics, 70(1), 65-94.

[2] Krugman, P. (1994). The myth of Asia’s miracle. Foreign affairs, 62-78.

[3] For index construction rules, please refer to the index methodology: https://spindices.com/indices/strategy/jpx-sp-capex-human-capital-index

The posts on this blog are opinions, not advice. Please read our Disclaimers.