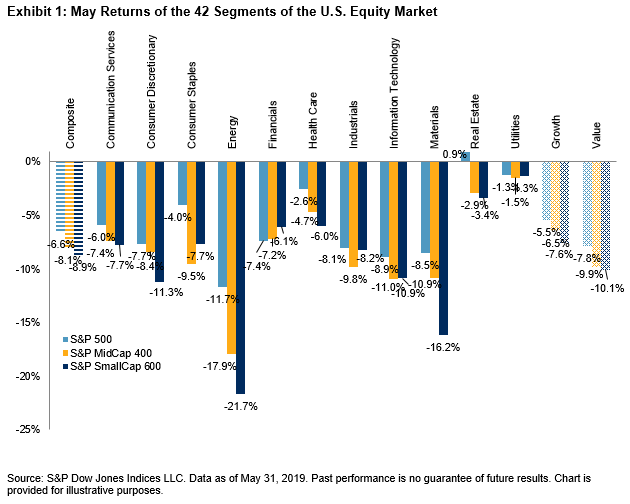

After four consecutive months of gains by the S&P 500®, the U.S. equity market broadly declined in May. The S&P 500, S&P MidCap 400®, and S&P SmallCap 600® declined 6.6%, 8.1%, and 8.9%, respectively. The primary catalyst was the renewed trade tension between the U.S. and China, which reversed course from the optimism coming out of March and April negotiations. On May 10, 2019, President Trump followed through on earlier threats to increase tariffs to 25% on USD 200 billion of Chinese products. This move was promptly thereafter reciprocated with tariffs raised on USD 60 billion of U.S. goods, effective June 1, 2019. Investors were left mulling the short- and long-term effects this would have on the global economy.

Large-cap Real Estate was the only segment of the U.S. equity market to post a gain in May. The 41 other U.S. equity segments were negative. The S&P 500 Real Estate finished May up 0.9%. The Real Estate sector consists of real estate investment trusts (REITs) and real estate management and development companies. The sector benefited in May from its relatively low exposure to foreign markets. Utilities, which was the best performer in May within the mid- and small-cap segments, was the only sector with lower average foreign revenue exposure than Real Estate. The Energy sector had the worst returns across all three size segments.

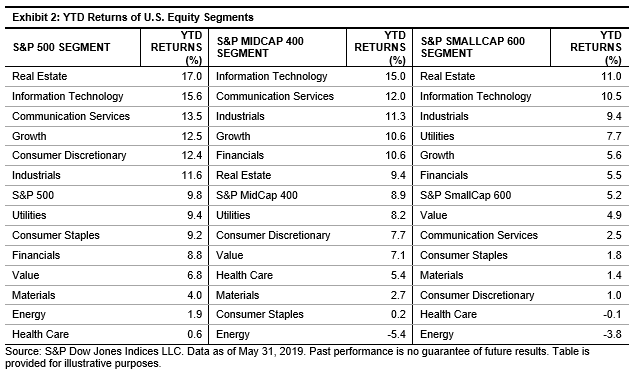

As of May 31, 2019, the Real Estate sector was the top-performing sector year-to-date. The price return of S&P 500 Real Estate year-to-date was 17%. The S&P 500 as a whole returned 9.8%. With strong price performance and an index dividend yield well above 3%, large-cap Real Estate was a clear winner through the first five months of 2019.

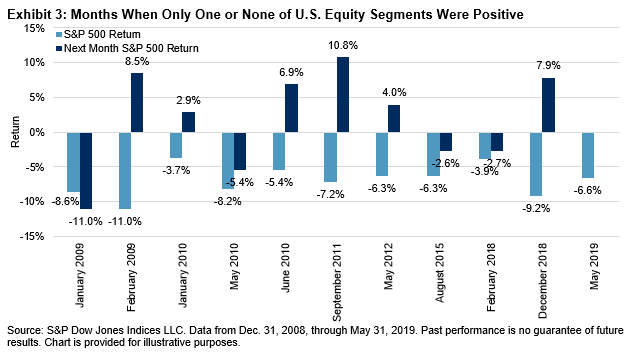

May 2019 marked the 11th time since January 2009 that the U.S. equity market declined this broadly. In the 10 previous instances when only 1 or 0 of the segments across U.S. equities were positive for the month, the S&P 500 average return was -5.6%. Only twice did the S&P 500 fully recover in the immediately following month, although the index had a positive return for 6 out of 10, averaging 1.9%, with a maximum increase of 10.8% and decrease of 11.0% (see Exhibit 3).