Making a suitable investment decision among multiple options has always been a dilemma. Market-linked investment options have generally resulted in apprehensive views from conservative investors who sense that equity markets bear heavy risks. Retail investors who lack an understanding of the markets are at risk, as bull runs tend to promote participation. Index-based investing can offer exposure to the markets with diversification, low cost, and transparency.

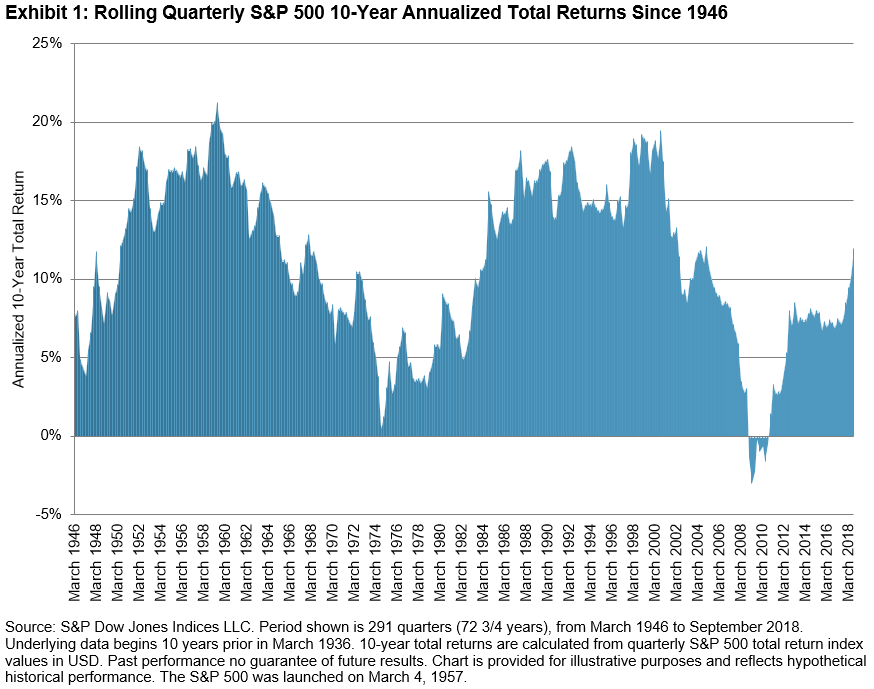

An index is designed to represent a market, sector, strategy, or theme. Investment strategies that replicate the index seek to align their performance to that index’s returns. For example, if an investment strategy were based on the S&P BSE SENSEX, its one-year annualized returns would be approximately 13% as of Sept. 24, 2018.

In the ongoing active versus passive debate, one could argue that active strategies outperform market beta. Could that be true? Yes, provided that a financial market expert makes all the right calls, coupled with the perfect timing. Is it possible for all investors to be such experts and to be vigilant of market movements in order to get the timing right? What about investable funds that are available for professionals who are not financial experts? There are doctors, engineers, architects, and businesspeople in diverse fields who all need viable investment avenues and are constantly researching investment options or reaching out to investment advisors.

Index-based investing can be a good solution to foray into market-linked returns. An index can provide a diverse basket of securities to manage concentration risk. A diversified market index like the S&P BSE SENSEX or S&P BSE 100 can offer exposure across sectors. Access to index information is also not an issue, as index changes are tracked on a day-to-day basis via multiple channels; index movements are displayed on stock exchange websites, past index trends are available on index provider websites, and there are other sources that provide continuous information on market movements. Index-based products have a lower expense ratio than active investing and are therefore a low-cost option. Indices are designed, calculated, and maintained by a neutral index provider, which ensures transparency, standardization, and a lack of bias in the strategy. Furthermore, there are many options for market segments via indices like the S&P BSE SENSEX 50, S&P BSE 100, S&P BSE 150 MidCap Index, S&P BSE 250 SmallCap Index; sector-based strategies via indices such as the S&P BSE Energy, S&P BSE Finance; and thematic strategies via indices like the S&P BSE India Infrastructure Index, S&P BSE Bharat 22 Index, S&P BSE Low Volatility Index, S&P BSE Quality Index, etc.

The posts on this blog are opinions, not advice. Please read our Disclaimers.