On May 16, 2014, Lok Sabha election results were announced, and Narendra Modi’s Bharatiya Janata Party got a clear mandate to form the government. Narendra Modi was sworn in as the 14th Prime Minister of India on May 26, 2014, and his government recently passed the four-year mark of being in power. This government has one more year before India has its next general election, so both the government and the opposition parties are now in election mode.

Over the past four years, the government has made several landmark policy decisions and initiatives that have had a major impact on the Indian economy. Some of the major policy and regulatory changes that have been initiated/implemented by the government are as follows.

- Goods and Services Tax (GST)

- Demonetization

- Arbitration and Conciliation (Amendment) Act

- Real Estate (Regulation and Development) Act

- Insolvency and Bankruptcy Code

Even after disruptive reforms like the demonetization and GST, economic growth is back on track. The government also eased foreign investment norms in important sectors like construction, retail, and aviation, which is expected to have a positive impact on these key sectors. Inflation during these four years has been moderate due to easing commodity prices, a good agricultural harvest, and the Reserve Bank of India’s monetary policies targeting inflation. However, the rupee has weakened since this government came into power.

When this government came into power, crude oil prices were over USD 100 per barrel; however, these prices have fallen substantially, which worked in the government’s favor and gave Narendra Modi room to roll out various reforms. However, oil prices have climbed over the past few months, and this will pose a challenge for the government, especially as elections are less than one year away.

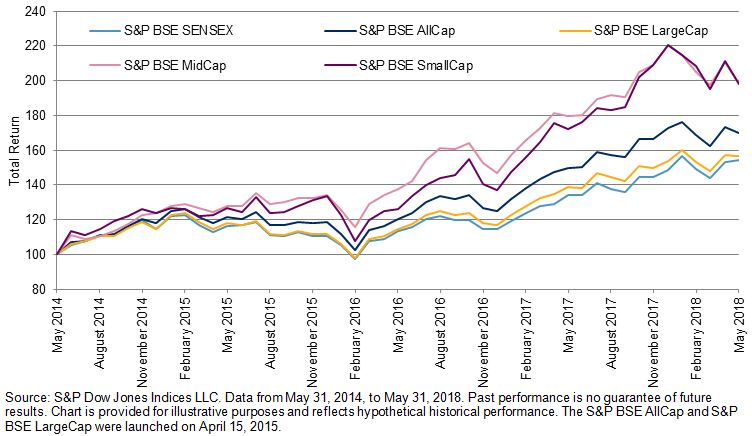

Capital markets in India have been on a bull run since this government came into power. The S&P BSE SENSEX total return value moved from 32,735.68 on May 31, 2014, to 50,572.53 on May 31, 2018; that is a four-year absolute return of 54.49%. The S&P BSE AllCap, a broad benchmark index with over 900 constituents, had a four-year absolute return of 69.79%. Among the size indices, the four-year absolute return of the S&P BSE MidCap was the highest, at 98.31%, followed by the S&P BSE SmallCap, at 98.25%, while the S&P BSE LargeCap was at 56.85%. Exhibit 1 depicts the total returns of the S&P BSE SENSEX, S&P BSE AllCap, S&P BSE LargeCap, S&P BSE MidCap, and S&P BSE SmallCap for the four-year period ending on May 31, 2018.

Exhibit 1: Total Return of the S&P BSE SENSEX and S&P BSE Size Indices

Exhibit 2 provides the four-year absolute returns of the S&P BSE AllCap series. We can see that among the sub-sector indices in the S&P BSE AllCap, the S&P BSE Consumer Discretionary Goods & Services and the S&P BSE Finance posted the best four-year absolute returns of 113.95% and 93.60%, respectively, while the S&P BSE Telecom had the worst return of -6.06%.

| Exhibit 2: Four-Year Absolute Returns of the S&P BSE AllCap Series | |||

| INDEX | INDEX VALUE ON MAY 31, 2014 | INDEX VALUE ON MAY 31, 2018 | 3-YEAR ABSOLUTE RETURN (%) |

| S&P BSE AllCap | 2,964.50 | 5,033.34 | 69.79 |

| S&P BSE LargeCap | 3,169.73 | 4,971.62 | 56.85 |

| S&P BSE MidCap | 9,486.29 | 18,811.84 | 98.31 |

| S&P BSE SmallCap | 10,151.26 | 20,125.14 | 98.25 |

| S&P BSE Consumer Discretionary Goods & Services | 2,221.81 | 4,753.64 | 113.95 |

| S&P BSE Finance | 3,685.57 | 7,135.23 | 93.60 |

| S&P BSE Fast Moving Consumer Goods | 8,059.50 | 14,144.68 | 75.50 |

| S&P BSE Information Technology | 9,615.65 | 16,593.38 | 72.57 |

| S&P BSE Basic Materials | 2,244.72 | 3,835.42 | 70.86 |

| S&P BSE Energy | 3,247.41 | 5,062.84 | 55.90 |

| S&P BSE Industrials | 2,898.42 | 4,003.18 | 38.12 |

| S&P BSE Healthcare | 11,138.54 | 14,339.33 | 28.74 |

| S&P BSE Utilities | 1,971.70 | 2,522.48 | 27.93 |

| S&P BSE Telecom | 1,364.29 | 1,281.66 | -6.06 |

Source: S&P Dow Jones Indices LLC. Data from May 31, 2014, to May 31, 2018. Past performance is no guarantee of future results. Table is provided for illustrative purposes and reflects hypothetical historical performance. The S&P BSE AllCap, S&P BSE LargeCap, S&P BSE Consumer Discretionary Goods & Services, S&P BSE Finance, S&P BSE Basic Materials, S&P BSE Energy, S&P BSE Industrials, S&P BSE Utilities, and S&P BSE Telecom were launched on April 15, 2015.

The posts on this blog are opinions, not advice. Please read our Disclaimers.