2016 has been an unpredictable year on many fronts, whether it was Leicester City FC winning the Premier League, the Brexit, or the U.S. election results. In India, “demonetization” and the Goods and Services Tax (GST) are fundamentally altering fund managers’ target portfolios. Active institutional fund managers have the benefit of professionally run research teams. The question is, therefore, how do individual market participants churn their portfolios in times of such volatility?

Many active portfolio managers have been adopting risk factors to achieve portfolio diversification and deliver excess returns. These common risk factors include size, dividend, volatility, momentum, quality, and value. In recent years, an increasing number of passive investment products have been designed to capture the potential benefits of factor-based investing (also referred to as “smart beta”) as well as the transparency and cost effectiveness of passive investing.

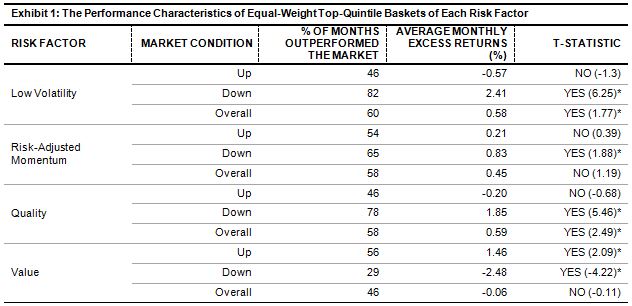

We recently published a report called Factor Risk Premia in the Indian Market, which studies the risk/return characteristics of common risk factors in the Indian equity market. The research analyzed four common equity risk factors—low volatility, risk-adjusted momentum, quality, and value—based on the S&P BSE LargeMidCap universe back-tested from Sept. 30, 2005, to April 30, 2016. Using the monthly return of the S&P BSE LargeMidCap to define up and down markets, we summarized the performance of different factors under these two market conditions.

The low volatility portfolio delivered significant excess return in the overall period, and the excess return was more pronounced during down markets. The quality portfolio, which was constructed using a combined score on return on equity (ROE), the balance sheet accruals ratio, and the financial leverage ratio, demonstrated similar defensive characteristics as the low volatility portfolio. In contrast, the value portfolio, constructed using book-to-price, earnings-to-price, and sales-to-price ratios, tended to outperform during up markets but significantly underperforms in down markets. The risk-adjusted momentum portfolio did not deliver significant excess returns in the overall period, despite significantly outperforming the benchmark during down markets.

The analysis shows that different risk factors in the Indian equity market have distinct characteristics and, therefore, they can be used for the implementation of active investment views. Moreover, blending risk factors with low return correlation may also provide portfolio diversification to mitigate risk.

Above risk factor portfolios are hypothetical equal-weight portfolios.

Source: S&P Dow Jones Indices LLC. Performance data is based on total return in INR. Data from Sept. 30, 2005, to April 30, 2016. Past performance is no guarantee of future results. Table is provided for illustrative purposes and reflects hypothetical historical performance. Please see the Performance Disclosure available in the research paper for more information regarding the inherent limitations associated with back-tested performance. Up months are those months when the float-market-cap-weighted S&P BSE LargeMidCap had positive returns. Down months are those months when the float-market-cap-weighted S&P BSE LargeMidCap had negative returns. Percentage of months that outperformed the market and average monthly excess returns were calculated using the float-cap-weighted S&P BSE LargeMidCap as the benchmark.

*Implies significance at a 5% level.

The posts on this blog are opinions, not advice. Please read our Disclaimers.