Even a cursory glance at financial markets indicates that market participants are expecting some form of interest rate increase in the near future—there has been a sell-off in the 10-Year U.S. Treasury Bond market, and certain sectors that are expected to benefit from such a rate increase have gained. For instance, the S&P 500 Financials increased over 13% for the month as of Nov. 30, 2016, compared with a total return of 1.8% for the preceding 10-month period.

Despite evidence to the contrary, conventional wisdom still dictates that rising rates are bad for equities. From January to October 2016, there was a high correlation (0.75) between the S&P 500® and the S&P U.S. Treasury Bond 5-10 Year Index. What was good (or bad) for the U.S. Treasury market tended to have the same directional impact on the U.S. equity market. However, this relationship broke down in November 2016—the S&P U.S. Treasury Bond 5-10 Year Index lost over 3% as of Nov. 30, 2016, while the S&P 500 closed at record highs on multiple occasions. Why might this be?

President-elect Donald Trump’s victory in the Nov. 8, 2016 election caused a reflation theme to emerge; the incoming administration’s proposed infrastructure spending and tax reductions resulted in expectations of increased inflation and an upward shift in the anticipated path of nominal interest rates. This has been bad news for U.S. Treasury bond prices; the predefined stream of nominal coupon payments is being divided by a higher discount rate. In that case, why haven’t equities been affected in the same way? After all, the Gordon Growth Model tells us that equity prices should fall as the nominal discount rate increases, ceteris paribus.

The answer can be found in the concept of inflation pass-through, broadly defined as a company’s ability to pass on inflation to its customers. The explanation is simple—because companies are able to change their dividends over time, inflation affects the nominal discount rate and the expected growth rate of dividends. Companies that are able to pass on inflation to customers could increase their expected growth rates by more than the rise in the nominal discount rate. This dynamic is even more relevant to the S&P 500, as its constituents are blue-chip companies with strong brand reputations. Therefore, they may be able to increase prices in line with inflation, without the drop in earnings that may be experienced by other companies.

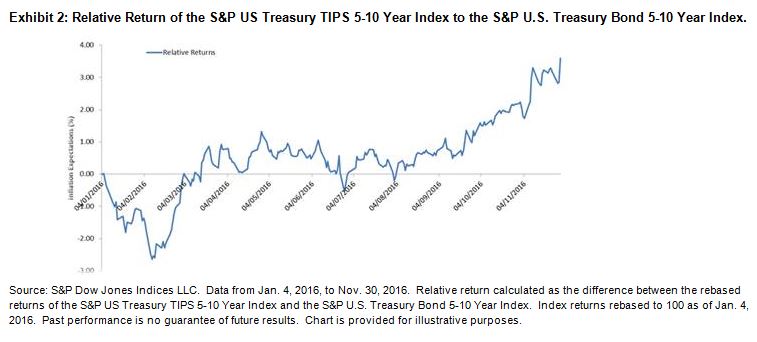

As a result, we might expect to see the S&P 500 increase (decrease) when the relative return of the S&P US Treasury TIPS 5-10 Year Index to the S&P U.S. Treasury Bond 5-10 Year Index improves (worsens) and for the reverse to be true for Treasury bonds. This is exactly what has happened since the start of 2016. If this trend continues, market participants may want to remember the impact of inflation pass-through before agreeing with the conventional wisdom regarding interest rates and equity valuations.

The posts on this blog are opinions, not advice. Please read our Disclaimers.