There have always been select actively managed funds that beat the cap-weighted indices market, and there always will be. But trying to find these funds before they outperform is exceedingly difficult, especially across multiple asset classes and styles. In addition, the outperformers may not pay well enough given the risk. Active managers may claim victory in certain categories for certain periods of time, but poor performance in other categories drags down overall portfolio performance. These combined hurdles should make an all-index-fund portfolio particularly appealing to many investors.

Hurdle #1: Predicting Individual Active Winners

The success of index investing over actively managed funds in individual asset classes and styles has been widely documented. The S&P Dow Jones SPIVA® U.S. Scorecard is an extensive report that’s published semiannually at mid-year and year-end. SPIVA divides mutual fund return data into category tables covering different asset classes, styles, and time periods. There’s also a measure of survivorship bias and style drift for every category over each period. This accounts for funds that are no longer in existence or have had a change in investment style.

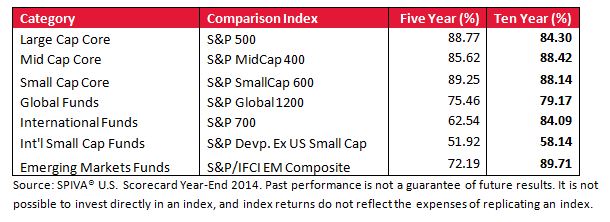

The SPIVA® U.S. Scorecard Year-End 2014 has data going back 10 years. Table 1 is a sampling of this data from a few popular equity asset classes and styles. The data represents the percentage of active funds that underperformed comparable indexes in each category for 5- and 10-year periods ended in 2014.

Table 1: Percentage of active funds that underperformed their comparison index

Hurdle #2: Building a Portfolio with Active Funds

Investors typically use multiple funds in their portfolios spanning several asset classes and styles. Although the underperformance of active funds in each individual category is well understood in the passive versus active debate, less well known is how portfolios of index funds have performed against portfolios of similarly structured active funds. Comparing these two types of portfolios is a relatively new area of research.

A Case for Index Fund Portfolios, a White Paper by this author and Alex Benke, CFP®, of Betterment looked into this question. We created portfolios using only index funds and compared them to portfolios using only actively managed funds from a database free from survivorship bias.

As expected, index fund portfolios outperformed comparable active fund portfolios because index funds outperformed the average active fund in each investment category. Interestingly, we also found an all-index-fund portfolio went further than expected. It had a greater probability for beating portfolios of active funds than we would have expected from using a simple weighted average of the active versus passive performance in each category.

Why were portfolios of index funds beating more active fund portfolios than expected?

Hurdle #3: Good Outperformance, Greater Underperformance

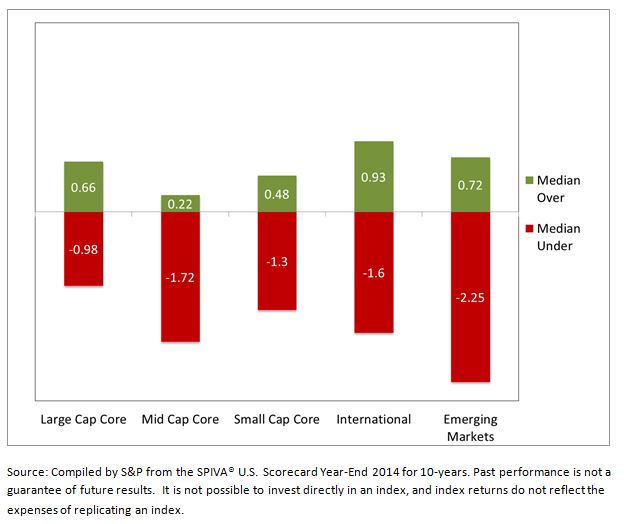

The reason all-index-fund portfolios outperformed active fund portfolios in greater numbers than expected comes from a second dimension of active fund underperformance. It’s not only the percentage of funds that underperform that matters, it’s the amount by which they underperform. Figure 1 is the magnitude of over- and underperformance of the median active fund in the primary equity asset classes in Table 1.

Figure 1: Magnitude of Active Funds’ Over- and Underperformance vs. Their Index

As shown in Table 1, the probability of an active fund’s outperformance was low in every investment category. To make matters worse, the funds that underperformed did so by a magnitude significantly greater than the alpha from funds that outperformed. The median over- and underperforming results are shown in Figure 1.

This is a double-whammy for active fund investors. It’s difficult to find active funds that will outperform, and when these funds do outperform, there’s not enough relative alpha to adequately compensate investors for taking active manager risk.

This risk is multiplied in an active fund portfolio. It may only take one or two underperforming active funds to drive the entire active fund portfolio under, because the magnitude of underperformance in the losing funds is expected to be higher than the magnitude of outperformance by the winning funds.

Too Many Hurdles to Win the War

It’s widely known that, over time, index investing has typically outperformed actively managed funds across every investment category. What’s less known is the benefit achieved from using a diversified portfolio of only index funds over a comparable portfolio of actively managed funds. The median alpha from the winning funds is low relative to the median underperformance from the losing funds, and this makes it tough to beat an all-index-fund portfolio, all the time.