This morning, I woke up to the headline Oil just spiked again, on news Saudi Arabia is bombing rebel positions in Yemen. It was the perfect reminder of a call I had earlier in the week from a large pension looking for an oil index to hedge geopolitical risk. After the call, my colleague asked, “Why would an investor use oil to hedge against geopolitical risk?” He continued with more questions like why not use equities or credits from those countries and isn’t it impossible to hedge against geopolitical risk?

In remarks from the Bank of Canada, geopolitical developments often have a major impact on oil prices since they can affect oil supply directly and since the threat of future supply disruptions can also build a risk premium into oil prices. As a notable example, in the early part of 2014, conflicts in Libya and Iraq led to temporary outages in their oil production, keeping world prices high, even as supply elsewhere in the world continued to ramp up. When production from those two countries came back on stream, that was an important trigger for the plunge in oil prices later in the year.

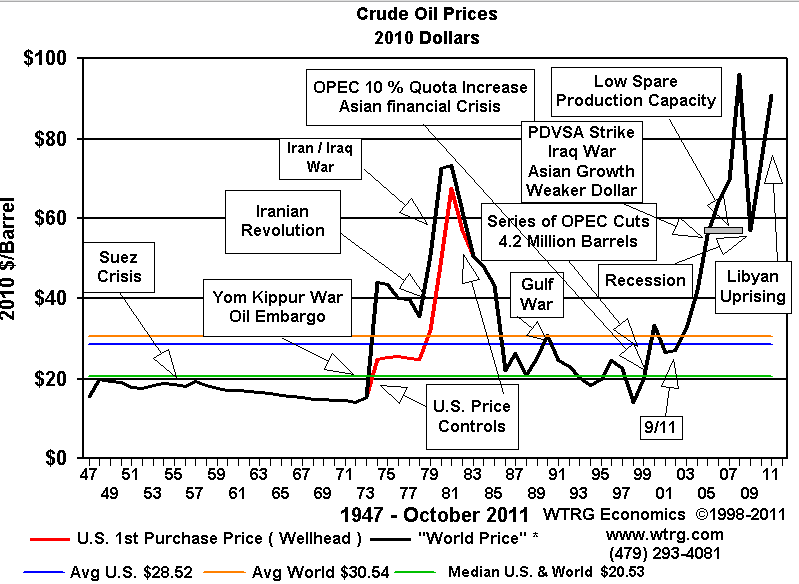

Notice in this chart produced by WTRG Economics the spikes in oil price jumped more than 2 times on average during these critical periods except the first Gulf war.

This behavior is no different today as demonstrated in the chart of oil prices for the past two weeks, hourly. Notice the oil spike from the Yemen bombing, despite the fact it is only the world’s 39th largest producer.

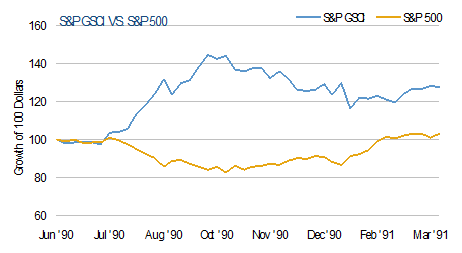

Not only do geopolitical events spike oil (and other commodities) but they may simultaneously hurt the stock market. An article posted by CNN Money just hours ago states, “The surge in oil followed a sharp sell off in the U.S. stock market overnight. European markets were all declining by about 1% to 2% in early trading and most Asian markets closed with losses.” The chart below shows another example of the S&P GSCI rising while the S&P 500 fell during the Persian Gulf War.

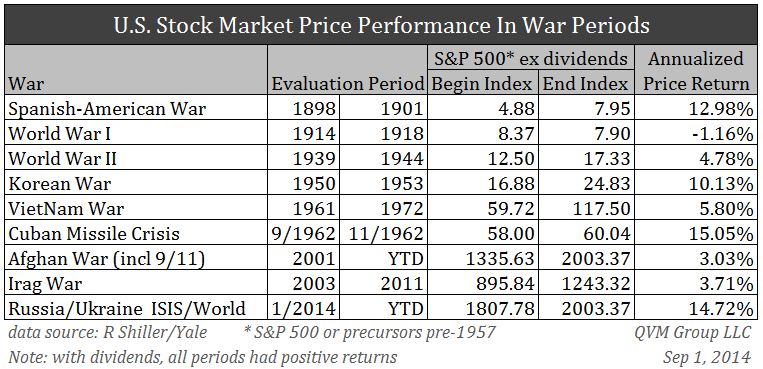

Based on the above, oil has historically performed better than stocks in times of war, though stocks have remained relatively flat in many cases as shown in the table below.

Although not all the countries with high geopolitical risk are necessarily high yield, there should be a link between them given the methodology from OECD to classify the country risk. According to OECD, “the country risk is composed of transfer and convertibility risk (i.e. the risk a government imposes capital or exchange controls that prevent an entity from converting local currency into foreign currency and/or transferring funds to creditors located outside the country) and cases of force majeure (e.g. war, expropriation, revolution, civil disturbance, floods, earthquakes).”

The high yield market has had a positive correlation with equity markets for many years when comparing the percentage change in spreads (over Treasuries) for key high yield indices vs. the percentage change in level for equities, and this correlation has become even more pronounced since the global financial crisis.

According to PIMCO, equity market volatility and its associated effects on enterprise value have driven high yield spreads. The investment implications of the equity–high yield correlation say that if you expect equity valuations to increase for a certain sector or name – whether based on general growth prospects, a changing environment or new information – then, all else being equal, you could expect credit spreads in that sector or name to decrease in the future. For example, spreads on credits related to metals and mining sectors widened in 2012 from relatively weak equity performance in the sector, mainly due to decreased demand from China.

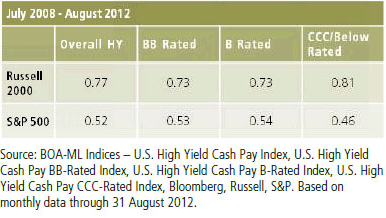

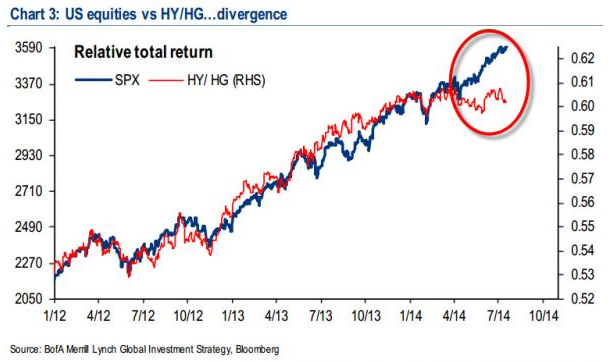

Even if stocks hold up in war times, it is possible investors will flee high yield bonds first since they may not feel they are getting compensated to take the geopolitical risk. As zerohedge.com points out, “geopolitical risk is causing a pause… Investors tend to flee riskier assets during times of turmoil.” This may cause a decoupling of high yield from stocks as seen in the chart below:

So if oil is the choice for hedging against geopolitical risk, then what type of strategy performs best? That depends on whether the term structure is backwardated or in contango. When backwardation is prevalent, the front month contracts have outperformed, and when contango is predominant, the forward months have performed better. From 2004-2011, contango dominated but in 2013 that changed. However, it takes time to move from one persistent term structure to the next given inventories can be slow moving in either direction. It can take some time for inventories to be drawn down and also may be difficult to replenish. This is similar in energy as it is in other commodities that are difficult to store, like agriculture.

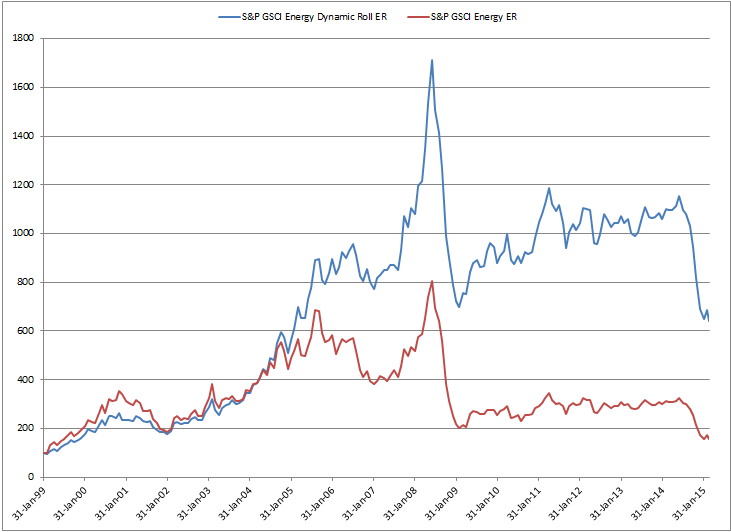

Below is a chart and table demonstrating the long term gain by using a dynamic roll strategy in energy. The sector is comprised roughly of 35% each WTI and Brent, 10% gasoil, 7.5% each of heating oil and unleaded gasoline, and 5% natural gas. Overall the annualized return since inception in 1999 is 12.7% for the S&P GSCI Energy Dynamic Roll and 3.5% for the S&P GSCI Energy.

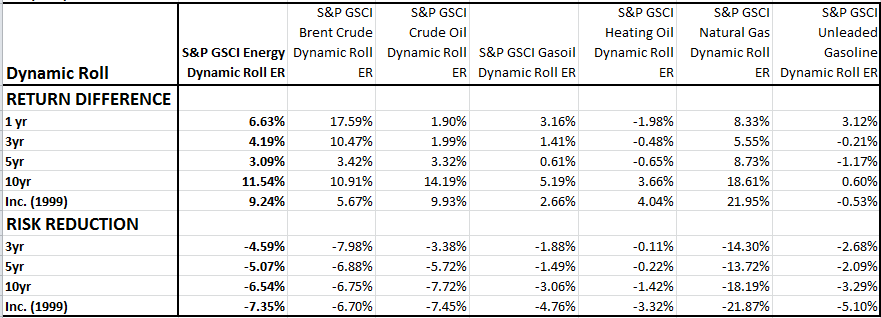

Certain commodities are more sensitive to the term structure that you can see below in the table. For example, heating oil and unleaded gasoline have front contracts that have outperformed later dated, more flexible strategies. As oil gets cheaper, the price for refined oil like heating oil and unleaded gasoline may drop, causing demand to increase and inventories to fall.

Source: S&P Dow Jones Indices. Past performance is not an indication of future results.

The posts on this blog are opinions, not advice. Please read our Disclaimers.