How would you like some heating oil (HO) for Christmas? Chances are you wouldn’t really like that too much, especially if you agree with this report posted on Morningstar.com that quotes, “Nobody would ever put oil in their house unless there was no gas on their street.”

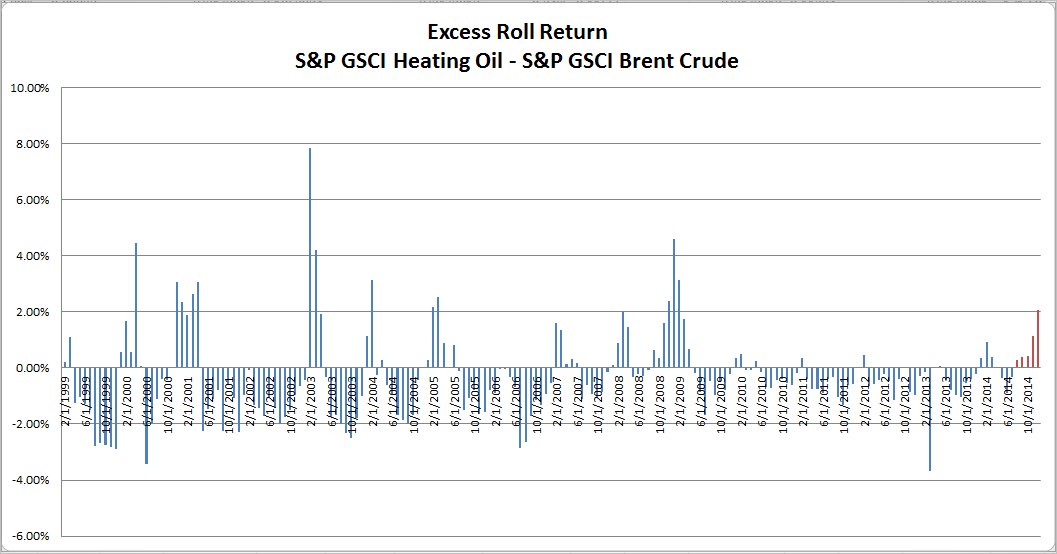

Despite the S&P GSCI Heating Oil (spot return) losing 12.7% this month through December 18, it is the only commodity in the energy sector whose excess return of -11.5% is greater than its spot return. With oil prices falling and heating oil in the index at its lowest since May 2010, how could the roll return (excess return – spot return) possibly be positive, indicating inventory pressure?

According to the International Energy Agency (IEA), saavy consumers are taking the opportunity to stock up on heating oil as prices fall. By October, German end‐user heating oil stocks reached 66% of tank‐fill (+1 percentage point m‐o‐m), their highest level since 2009. The impact is pairing excess return losses this month on heating oil compared to other petroleum constituents including WTI -18.1%, Brent -16.0%, unleaded gasoline -16.4% and gasoil -16.7% in the index.

The difference in roll return or term structures between the S&P GSCI Heating Oil and S&P GSCI Brent Oil has been increasing at an unprecedented rate. Never in history has this difference increased for five consecutive months. There have been five times in history since 1999 with five consecutive months showing greater excess return in heating oil than Brent oil but not with the acceleration of today that reflects the stockpiling by the heating oil consumer.