What are Preferreds?

Preferred shares are hybrid equity securities, with characteristics that lie between the traditional fixed income and equity asset classes. Like common shares, preferred shares represent ownership in a company and are listed as equity on the balance sheet; the ownership isn’t entirely the same though. Preferreds have preferential rights to dividend payments before common shares, which is thanks to their seniority in the capital structure. On the other hand, common shares come with the right to vote on corporate matters, a feature that preferreds lack.

Several characteristics that preferreds share with bonds are that they are issued at a fixed par value and dividend payments are a fixed percentage rate of par. Independent credit rating agencies, such as DBRS and S&P Ratings Services, rate preferred securities using the same guidelines as bonds. Preferreds offer less security to investors than bonds, as they sit lower in the capital structure and issuers have more flexibility in cancelling or postponing a dividend payment if it is running into liquidity issues.

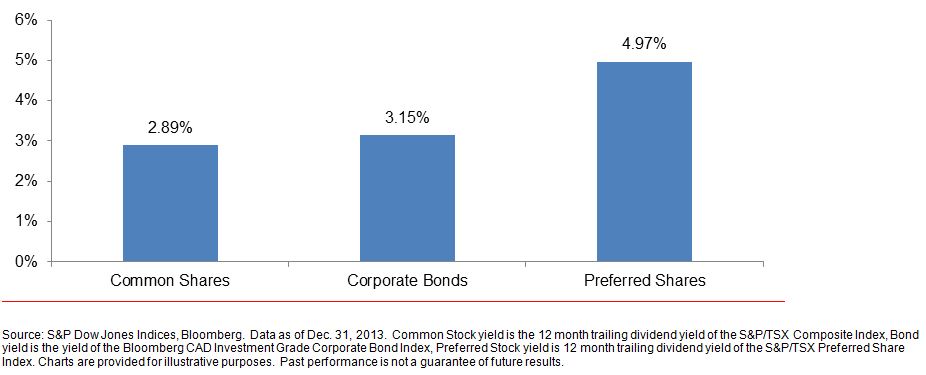

A main benefit of preferreds is that they pay sizable dividends, with most paying a fixed amount on a quarterly basis. In fact, when looking at the asset class yields of bonds, preferreds and common equity, one can see that preferreds offer the highest yields.

Preferred Market Overview

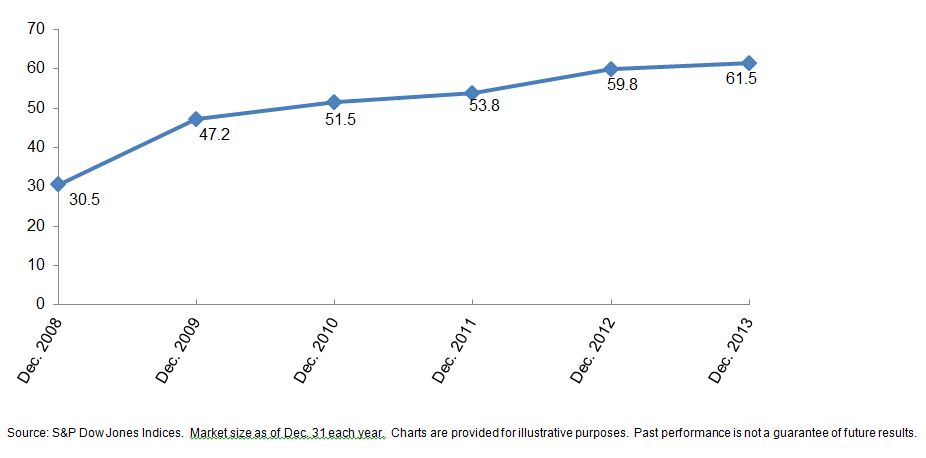

With interest rates continuing to remain at historic lows, investors have been looking for investments that offer higher yields than common stocks and bonds. Since preferreds meet this condition and have shown relatively low price volatility, the asset class has been a benefactor of investor demand. The preferred market in Canada grew to an estimated CAD 61.5 billion at the end of the year in 2013, doubling in size since year-end 2008. The exhibit below shows the growth of the Canadian preferred market over the past five years.