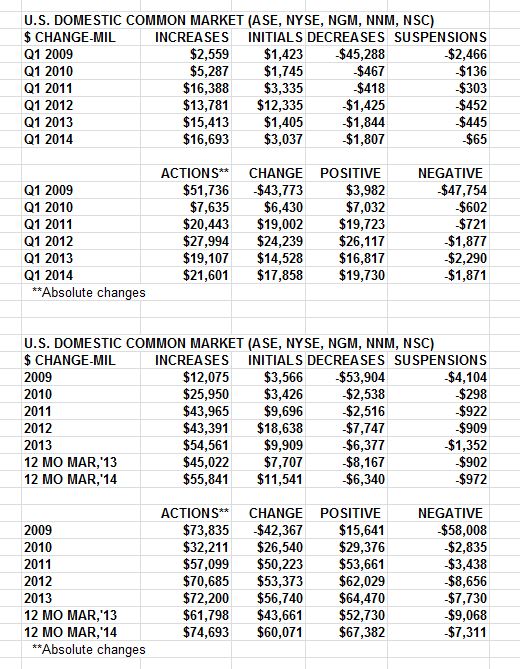

Data is for U.S. Domestic Common Stock, not just the S&P 500

U.S. domestic common issues set a first quarter record for dividend increases, as the ‘shareholder’ return theme continued. Increases have been made easier by record earnings and record cash holdings. Additionally, many issues (especially large-caps) have heard the knocking at the boardroom door – from activists. I expect strong dividend growth to continue in 2014, as ‘shareholder return’ continues to be the battle cry from boardrooms, and those knocking at the boardroom door. I expect the actual cash payments for 2014 to post a double-digit increase over the record setting 2013 level. Yields remain competitive, with qualified dividends have a tax advantage.

For U.S. domestic common stock in Q1 2014:

U.S. domestic common issues set a first quarter record for dividend increases, as the ‘shareholder’ return theme continued.

Record number of increases (increases, extras, initiations, resumptions), as 1,078 issues increase, surpassing the record of 1,069 set in 1979 (records start in 1955) 102 issues decrease (decrease, suspend), verses 139 in Q1,’13

Q1,’14 indicated dividend rate increases $17.8 billion, a 22.9% rise over the Q1,’13 $14.5 billion gain 12 month March 2014 increases $60.0 billion verses 2013’s $56.7 billion

The percentage of dividend paying issues (U.S. domestic common, ASE, NYSE, NASD) decreased to 47.0% from Q4,’13’s 47.7% (Q3,’13’s 47.4%, Q2,’13’s 47.3%, but up from Q1,’13’s 46.1%)

The number of payers went up, but the number of trading issues went up much more 84.2% of the S&P 500 (421 issues) pay a cash dividend, the most since Sep,’98 (was 473 when I started in May,’77), and all of the DJIA30 issues pay

Yields slightly increased, as the market’s growth slowed (but there was price appreciation) Weighted dividend yield at the end of Q1,’14 was 2.48%, compared to 2.44% for Q4,’13, and Q1,’13 was 2.61%

Dividend yields remain relatively attractive compared to other instruments such as corporate bonds, treasuries, and bank CDs, especially considering the lower (permanent) tax rate advantage.

Payout rates (dividends as a percentage of As Reported GAAP earnings) remain low, as companies payout record amounts, but payout less as a percentage of what they are making -> cash sets another record

U.S. common stocks set a Q1 record (from 1955) for increases, beating out 1979 (fyi: 10-year is 2.68%, was 10.33% in ’79 and then went up to 15.8%; 500 yield is 1.9% and was 5.2%)