Today’s Wall Street Journal brought the latest in a string of articles suggesting that we have entered a period of particular opportunity for active investment management — a so-called “stock-picker’s market.” Because the average correlation of stocks within the S&P 500 or other major indices has declined, it’s argued, “active managers are going to do better” as the “cream rises to the top.”

Or maybe not. The argument in favor of active management in 2014 has to contend with at least three inconvenient truths.

First, the average cannot be above average. If all asset owners own all the assets there are to be owned, the average asset owner will earn the return of the average asset (i.e., the market return). If we array the asset owners in rows and the assets they own in columns, the sum of the rows must equal the sum of the columns, and the sum of the changes in the rows must equal the sum of the changes in the columns — so the average return across the rows equals the average return down the columns. William Sharpe called this “The Arithmetic of Active Management” more than 20 years ago, and the laws of arithmetic still hold.

Of course, there can still be periods when the average institutional manager outperforms a market index — but they occur only when the rows and the columns don’t match. For example, if individual investors control 80% of the assets, and institutions control 20%, it’s entirely possible for most of the institutions to do better than the market average. (This may be a fair description of the 1950s and 1960s.) If a market index doesn’t describe the managers’ entire opportunity set, it’s also possible for the average manager to outperform — perhaps by buying small- and mid-cap stocks while being compared to a large-cap benchmark.

But if the index is sufficiently comprehensive, and the census of all investors is sufficiently accurate — the inexorable arithmetic of active management will hold. Empirical studies have amply verified the theoretical argument.

Second, correlation is primarily a measure of timing, not of investment opportunity. Assets which are positively correlated go up and down at the same time; negatively correlated assets move in opposite directions. It’s not hard to put together an example of two stocks with perfectly negative correlation but with identical returns over the course of a month. An omniscient day trader would benefit from trading these stocks. For the rest of us, the benefits are less clear. The fact that correlations declined in 2013 means that (other things equal) the market will be less volatile in 2014. It does not mean that active manager performance will improve — the average is still average.

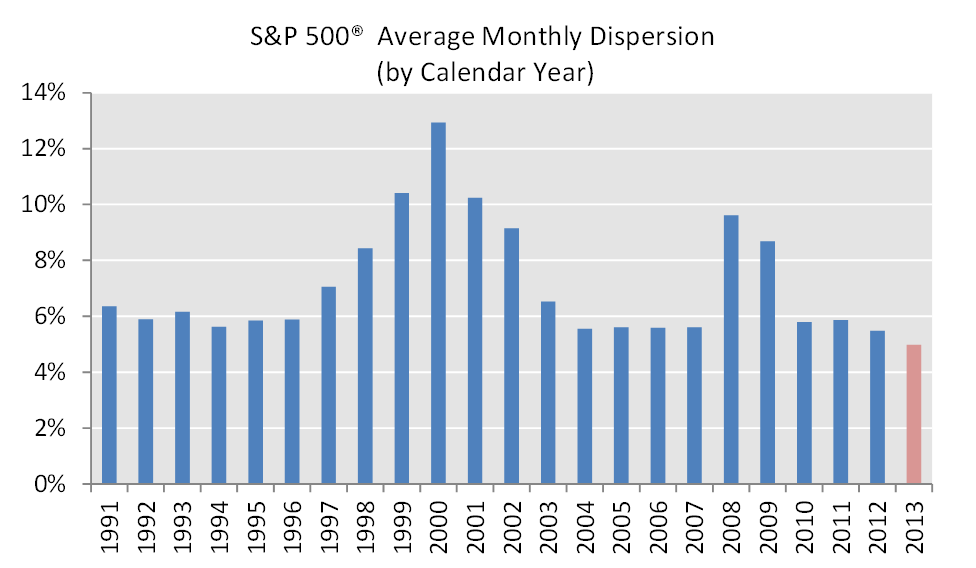

Finally, dispersion — which is a measure of investment opportunity — remains low. Unlike correlation, which measures whether assets go up and down at the same time, dispersion reflects the degree of difference between the best and the worst performers. In a high dispersion environment, there’s a large gap between the “best” stocks and the “worst” stocks; when dispersion is low, the gap is small. In 2013, dispersion in the U.S. market — despite falling correlations — was at its all-time low:

Although dispersion ticked up modestly at the beginning of 2014, it’s still well below its historical average level. This doesn’t mean that a skillful (or lucky) manager will be less skillful (or lucky) than he would otherwise be. Dispersion says nothing about the level of a manager’s skill, but it signifies something important about the value of that manager’s skill. The fact that today’s dispersion levels are quite low implies that the rewards to successful stock picking are likely to be small by historical standards.

Although dispersion ticked up modestly at the beginning of 2014, it’s still well below its historical average level. This doesn’t mean that a skillful (or lucky) manager will be less skillful (or lucky) than he would otherwise be. Dispersion says nothing about the level of a manager’s skill, but it signifies something important about the value of that manager’s skill. The fact that today’s dispersion levels are quite low implies that the rewards to successful stock picking are likely to be small by historical standards.

Which does not sound like a “stock-picker’s market” to me.

The posts on this blog are opinions, not advice. Please read our Disclaimers.