Two carefully watched numbers are the earnings per share (EPS) and the price-earnings ratio (PE) on the S&P 500. Their popularity stems from the wide spread use of the index and its long data history. EPS is the market analysts’ gauge corporate profits in the US while the PE is their measure of value. While there is a lot of debate over what level of PE is so high one shouldn’t but or so low one should rush into the market, most analysts agree it is a key valuation measure.

The PE is the ratio of the price of the index to the earnings per share. The index price, say 1848, can be thought as the price of one “share” of the S&P 500 and the EPS, about $108.00 is the earnings of the companies represented by that share of the index. There are a few ways to measure the PE, depending on how earnings are measured. Most of the time people use a full year measure instead of one quarter’s earnings because there are seasonal shifts in earnings for some industries. The key question is whether to measure earnings by the last four quarters of data based on company reports or to be forward looking and measure earnings by analysts’ estimates for the coming year. While market prices depend in part of people’s expectations of the future, using the recent history – usually called “trailing earnings” — means using real numbers rather than forecasts. Since earnings usually rise, the PE based on trialing earnings is likely to be a higher number than the PE based on analysts’ estimates of next year’s results.

Calculating the earnings per share for the index is a bit more complicated than the PE. It follows the same approach used to calculate the index itself: the market value of each of the 500 companies is added together giving a total is about $15 trillion today. Then to have a more manageable number for the index level, the $15 trillion is divided by a scale factor called the divisor. One can think of the divisor as if it were the number of shares outstanding of a company: a company’s stock price is its total market value divided by the number of shares. Likewise, a company’s EPS is its total earnings divided by the number of shares. The analogy is that the EPS for the S&P 500 is total earnings of the 500 companies, divided by the same divisor used to calculate the index.

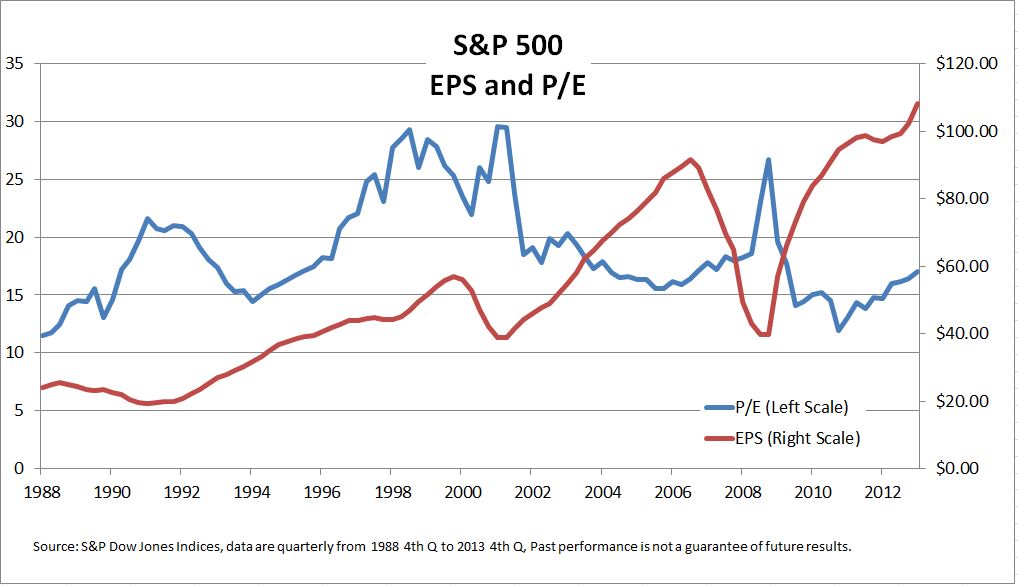

The EPS calculation includes earnings of all the companies in the index, including any that lost money. Counting only positive profits and skipping losses might make for nicer numbers, but it would be market analysis through rose colored glasses. The chart shows both the PE and the EPS for the S&P 500 going back to 1988. The bear markets in 2000-2002 and 2007-2009 stand out: earnings fell sharply. On both occasions, the PE rose because the proportional drop in earnings was greater than the decline in stock prices.

Neither the PE nor the EPS are infallible guides to the stock market, but both are important measures of how the market is doing.

The posts on this blog are opinions, not advice. Please read our Disclaimers.