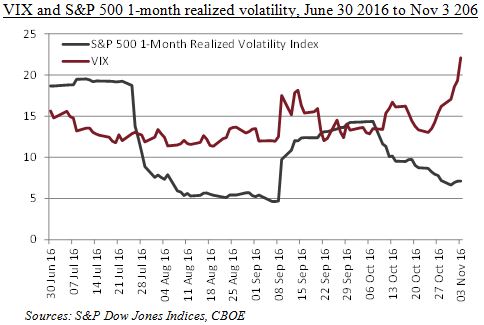

Despite a narrowing election race and a deluge of earnings, the S&P 500 has not seen a daily change greater than 1% in nearly four weeks. Realized volatility remains remarkably low. But the CBOE Volatility Index (VIX) – a predictive measure of future volatility that is often seen as Wall Street’s “fear gauge” – has nearly doubled in the same period. Is it the calm before the storm, or has VIX just got the jitters?

Presently, the difference between VIX and S&P 500 realized volatility is highly significant. November 3rd’s closing VIX was 22.1 – nearly triple the S&P 500’s trailing volatility of 7.1. A VIX higher than realized volatility is not unusual, especially when realized volatility is low, but the spread between VIX and realized volatility has reached extremely rare levels.

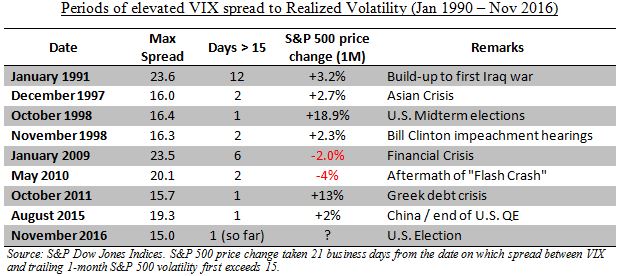

The gap between VIX and realized volatility has been greater than 15 on only a handful of occasions in the past quarter century. In most cases, an impending political event was the cause of the elevated VIX, and intriguingly, the subsequent performance in the S&P 500 was more commonly positive than negative.

The table provides grounds for optimism: with so much fear in evidence, one might assume that the current level of the S&P 500 reflects a discount for the market’s fears of a disruptive election result, not the current economic reality. And indeed the day-to-day economic news has been encouraging: earnings have been largely positive and as far as the U.S Federal Reserve sees it, a case is easily made for the bulls.

But we may well ask “what if the pollsters and the betting markets – both of which are currently indicating a win for Hillary Clinton in the election – have it wrong?”

Volatility markets have precedent for predicting surprise results: it is notable that the spread from VIX to realized S&P 500 volatility rose as high as 13 on the day before the UK referendum in June. In fact, the market’s anxiety over a potential vote to leave the EU was telegraphed in the currency volatility markets as much as three weeks before polling day.

Trump’s protectionist trade policy and political populism have drawn comparisons with the “Brexit” campaign, and the behavior of volatility markets in advance of the vote provides a further similarity. If Trump does indeed win, we cannot claim that the VIX didn’t warn us.

The posts on this blog are opinions, not advice. Please read our Disclaimers.