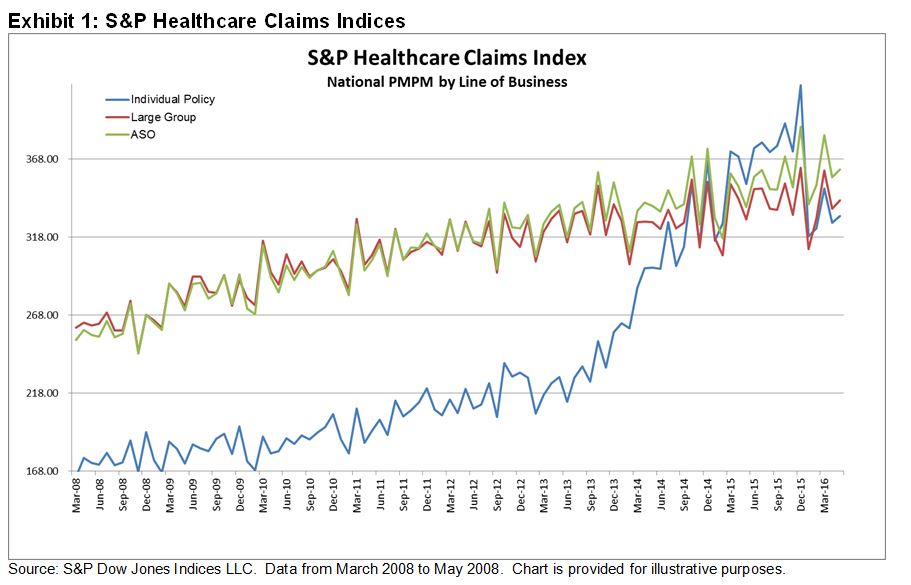

There are many in the healthcare market who have speculated that the Affordable Care Act (ACA) was doomed to fail due to high-cost individuals with pre-existing conditions driving up the average cost of care, while the healthy population that needed to support the cost of care for the sick remained on the sidelines with little-to-no incentives to become insured. The S&P Healthcare Claims Indices supported this theory throughout 2015, when the average cost of care for a patient with an individual health insurance policy topped out at USD 415.15 versus USD 388.70 for an employee covered under an ASO type policy by their employer, or USD 338.92 for an employee covered under a large group type policy by their employer (see Exhibit 1). That is, USD 26.45 more to treat a patient covered by an individual policy versus a self-insured type policy, and a whopping USD 76.23 more to cover an individual policy patient versus a patient covered by a large group policy by their employer. Under both the self-insured and large group structure, the employer requires all employees to maintain insurance, which in effect forces a suitable population of healthy people to pay for unhealthy people.

What Has Changed?

As seen in Exhibit 1, we can see a drop in the average cost of care for a patient covered under an individual policy starting in 2016. Now that costs for individual policies are in line with those of employers, one can argue that this is how the ACA was envisioned to work. With everybody having access to care, everybody paying their fair share, average costs should be in line with that of the overall market. However, a more in-depth study is needed to understand the reasoning behind individual policy costs coming in line with the employer market. We envision several potential reasons for the larger drop in average costs relative to the employer market. In this edition, we will focus on one possible explanation.

When plan enrollees approach the end of a plan year, they often review their total out of pocket costs for that given year. In a year where plan members have hit their maximum out of pocket costs, they are more likely to continue to spend and try to get all elective health issues addressed in the current year rather than carry them over to the next plan year where their maximum out of pocket costs will reset. If we think about how the ACA enticed many uninsured individuals with pre-existing conditions to enter the market, buy insurance, and utilize that coverage to address their existing needs, it only makes sense that they will try to address all of their pre-existing conditions in the same plan year to avoid unnecessary out of pocket expenses. If this is the case, then 2015 should be an anomaly, and moving forward we should see average individual costs stay in line with employer costs, assuming the ACA is working the way it was intended to work.

The posts on this blog are opinions, not advice. Please read our Disclaimers.