In a prior post, we analyzed the holding period of single-family homes using the S&P/Case-Shiller Home Price Index Series. We quantified the holding period with the rolling return for each period in question—10-, 7-, 5- and 3-year holding periods. In this post, we use the same holding period concept to look into whether the condo market behaves differently than the single-family homes market and assess whether the same pattern holds across the different cities. The cities investigated are Boston, Chicago, Los Angeles, New York and San Francisco. We found that the five-year holding period was the worst-performing holding period across the five cities.

In the single family market, the longer 10-year holding period fared better than the shorter duration periods, and we found that of the shorter duration periods, the three-year period performed better than the five-year period. In the condo market in all five cities, the five-year period experienced the largest decline. To rule out that the cause of the five-year decline was the trough in 2012, we looked at the holding period’s behavior prior to 2012, and we found that the time period that experienced the largest decline was indeed the five-year period.

So what is the cause of this five-year itch? On average, American home owners sell and move every five-to-seven years according to the Census, for reasons ranging from the house being too small to a job transfer. Many variables that drive single-family homes drive the condo market: upgrade, change in demographic, the need to move to a single family home, neighborhood changes, cash in equity, etc. Property owners are less likely to base their decision to buy or sell on the state of the market, and they are more likely to make the decision for personal reasons, because it’s where they live and the place most likely to affect their quality of life.

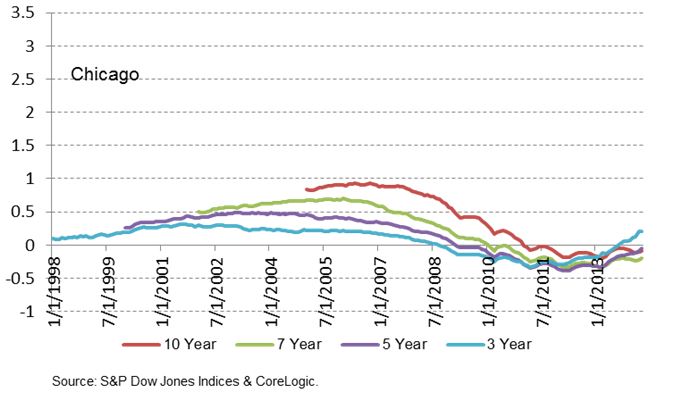

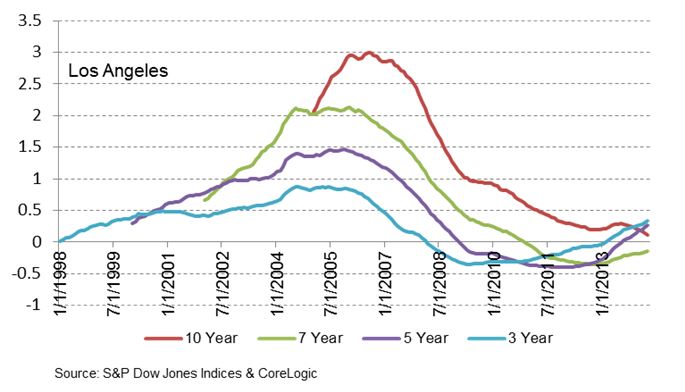

We did find that while the five-year period was the one that fared the worst, the range of returns—gains and losses—varied across the five cities. The following charts show the different holding periods for Chicago and Los Angeles.

In the 10-year holding period, Chicago faired worst having the smallest gain of 93% and the largest decline of 20%. Los Angeles had the maximum gain of 300%. New York didn’t enter into negative territory in the ten year holding period with the smallest gain being 37%. Overall, home owners could benefit from longer holding periods in the condo market, albeit differently depending on their geographic location, but they may need to watch out for that five-year itch.

The posts on this blog are opinions, not advice. Please read our Disclaimers.