The third quarter of 2025 was notable for a number of market milestones. There were 12 days when the S&P/ASX 200 reached a new all-time high at market close. The movements of the flagship market index and new highs were widely reported; however, lesser known is the outperformance of the S&P/ASX Small Ordinaries compared to the S&P/ASX 200.

The S&P/ASX Small Ordinaries was up 15.3% in Q3 2025, outperforming the S&P/ASX 200 by more than 10%. That is the largest quarterly outperformance of the S&P/ASX Small Ordinaries versus the S&P/ASX 200 since Q2 2009, when the markets were recovering from the 2008 Global Financial Crisis.

The quarter’s small-cap outperformance is also the third-largest three-month outperformance of the S&P/ASX Small Ordinaries over the S&P/ASX 200 since the inception of the index.

The Materials sector accounted for more than half of the S&P/ASX Small Ordinaries return for the quarter, with gold mining companies among the top contributors, benefitting from a strong gold price.

What Is the S&P/ASX Small Ordinaries?

The S&P/ASX Small Ordinaries was launched April 3, 2000, and is designed to measure the performance of smaller companies listed on the ASX. The index includes all the companies in the S&P/ASX 300, while excluding the S&P/ASX 100, which comprises the 100 largest ASX-listed companies by rank of three-month average market capitalization.

Typically, the S&P/ASX Small Ordinaries has had less representation of Financials than the S&P/ASX 200 and more diversified weights in other sectors such as Materials, Consumer Discretionary, Real Estate and Industrials.

Small Caps Offered More Diversification

The higher the weight of a constituent in an index, the larger the contribution to the index performance, based on the company’s share price movements. Fewer companies can meaningfully affect performance in a more concentrated stock market index.

As of Sept. 30, 2025, the top 10 companies in the S&P/ASX 200 comprised more than 47% of the index weight, with the “big four” banks making up 24%.1 The S&P/ASX Small Ordinaries was more diversified at the constituent level, with the top 10 companies comprising just under 15% at the same point in time. Cumulatively, the top 50 securities in the S&P/ASX 200 comprised nearly 80% of the index weight, while for the S&P/ASX Small Ordinaries, the top 50 companies represented less than 50% of the index weight.

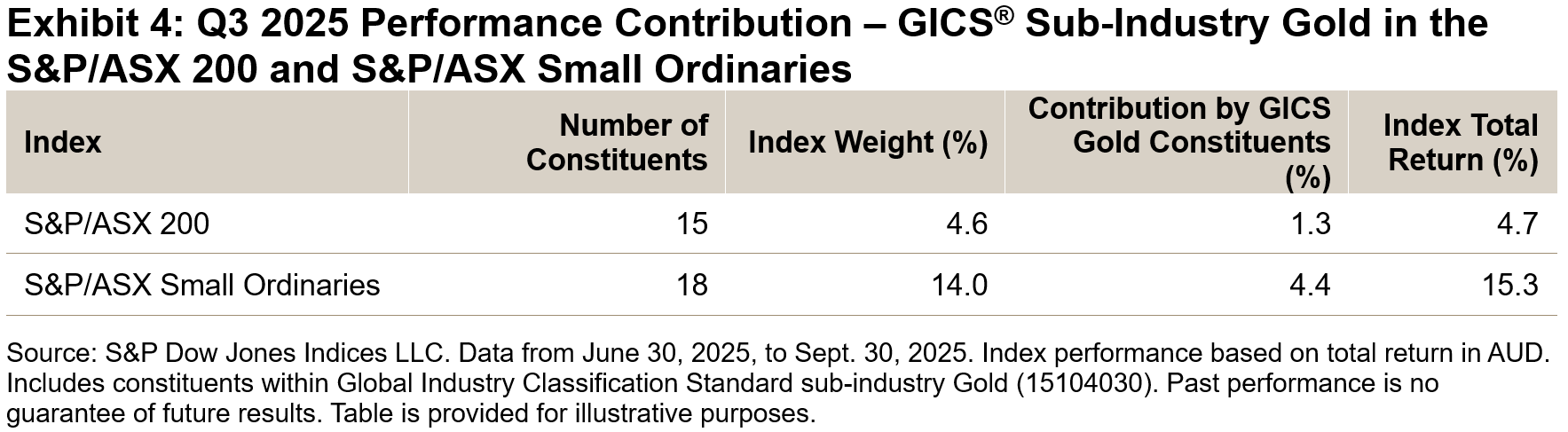

Therefore, more companies within the S&P/ASX Small Ordinaries could have a meaningful contribution to index performance when compared to the S&P/ASX 200. Exhibit 4 further breaks down performance contribution to show a comparison of gold producers in each index.

S&P/ASX Small Ordinaries Edged ahead over Three-Year Period

With its strong performance in Q3 2025, the S&P/ASX Small Ordinaries gained 21.50% over the one-year period, doubling the gains of the S&P/ASX 200 while also edging ahead of the S&P/ASX 200 over the three-year period ending Sept. 30, 2025.

In terms of diversifying away from large-cap-heavy broad market indices, other S&P/ASX mid- and small- cap indices have also performed well. The S&P/ASX 200 Ex-S&P/ASX 100 Index (the bottom 100 companies in the S&P/ASX 200 by market cap) outperformed over the one- and three-year periods, while the S&P/ASX Midcap 50 was the top performer over the 5- and 10-year periods ending Sept. 30, 2025.

Conclusion

S&P/ASX mid- and small-cap indices have significantly outperformed in the short term and showed greater diversification at both the sector and security level compared to broad market indices, which have been increasingly concentrated in large-cap Financials and Materials.

1 Big 4 banks are made up of: Commonwealth Bank of Australia, National Australia Bank, Australia and New Zealand Banking Group and Westpac.

The posts on this blog are opinions, not advice. Please read our Disclaimers.