The debt ceiling debate in Washington appears to be nearing an end. According to the U.S. Treasury, Congress has “always acted when called upon” and markets will look for them to do so for the 79th time this month. By index rule, all commodities in the S&P GSCI are traded in U.S. dollars, so the importance and reverence to the “world’s reserve currency” rings true every time a futures contract on the S&P GSCI is settled.

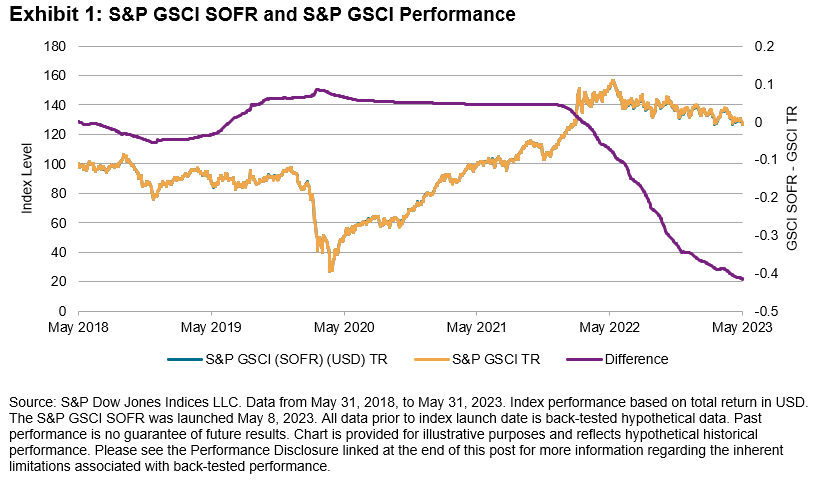

The S&P GSCI SOFR launched in May and leverages the same index construction and calculation principles as the S&P GSCI, but applies the Secured Overnight Financing Rate (SOFR) into the calculation instead of Treasury Bills. Using SOFR in lieu of Treasury Bills allows for performance tracking with alternative cash management strategies. Including rates that are collateralized by Treasury securities, there is still exposure to the faith and credit of the U.S. government. However, it excludes certain transactions that are deemed to be trading “special,” or at a rate outside the general market activity. The SOFR is published daily by the U.S. Federal Reserve and can be found on its website. As SOFR volumes rise, the ability to have a complementary index allows for potentially improved cash management capabilities through cash and derivative instruments.

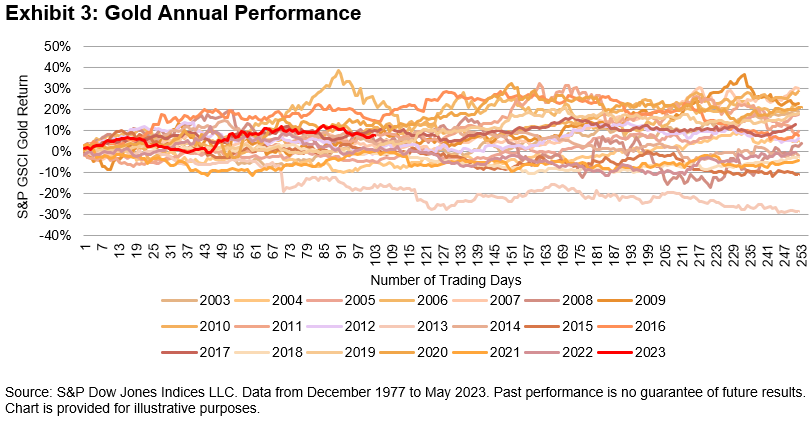

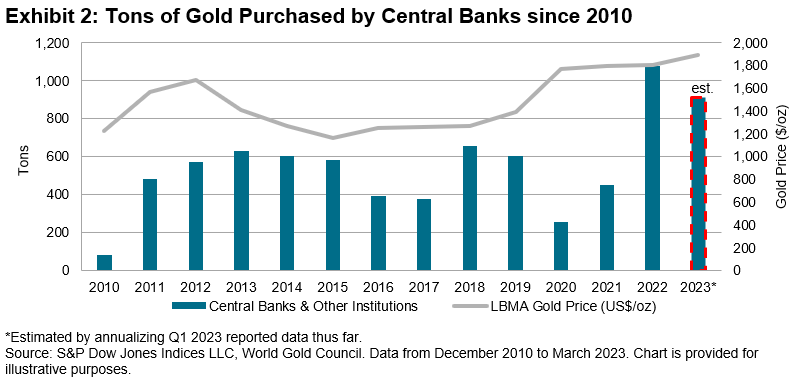

Gold has long served as the alternative to fiat currency when there is concern in the market regarding the political outlook. With this year’s debate, the S&P GSCI Gold has traded near its all-time high and has outperformed broad commodities by over 18%. While fiat money can, and likely will, continue to be printed, the global production of gold is relatively flat at just 1%-2% of total supply. Central banks have purchased gold at rates not seen since the U.S. government broke its gold standard in 1971. Steady supply creates a relatively fixed base for the metal, while demand is largely driven by some of the largest holders of U.S. government debt: global central banks.

Largest Central Bank Purchases in 50 Years

Since hitting a YTD high of 12%, the S&P GSCI Gold has turned in solid, if not spectacular, results. Popularity has risen due to the recent debt ceiling debates, and despite politicians coming to a solution that would avoid default, central bankers appear to be stocking up.