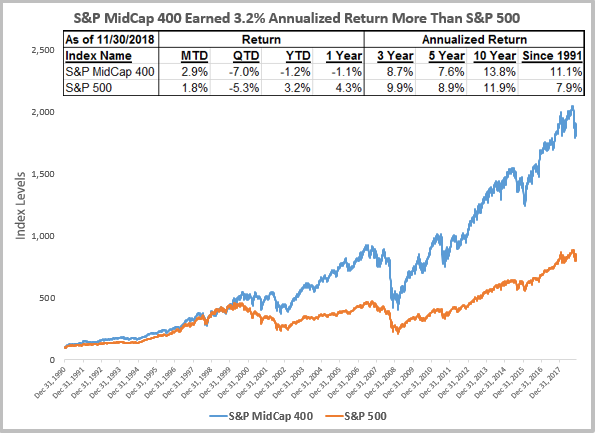

29 months after the referendum that triggered Britain’s departure from the E.U., and a little over four months from the scheduled departure date, the nature of the ultimate exit deal (if any) remains uncertain. What can indices tell us about the market’s reaction and expectations?

The volatility of the pound sterling has offered a direct link to the uncertainty faced by market participants. And with a parliamentary vote on the proposed terms of Britain’s withdrawal expected on December 11th, the CBOE/CME FX British Pound Volatility index (BPVIX) has risen to its highest levels since the referendum.

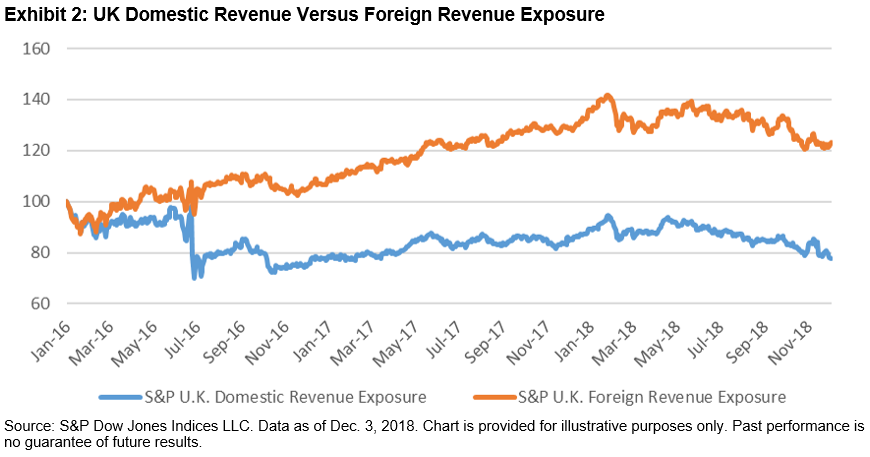

UK equities tell a similar story; the S&P U.K. Focused Domestic Revenue Exposure Index and S&P U.K. Focused Foreign Revenue Exposure Index were designed to measure the performance of UK companies with primarily domestic and primarily foreign revenues, respectively. Comparing these indices provides a better understanding of how the markets believe companies in the UK will fare. Exhibit 2 compares their performance since the beginning of 2016. (The Brexit referendum was held on June 23, 2016.)

Through Dec. 3, 2018, UK companies with primarily foreign revenue exposure had gained 14% since the Brexit referendum, while UK companies with primarily domestic revenue exposure had lost 21%. For those counting, that’s a 35% return spread.

Part (but not all) of this decline may be attributed to currency movements. The pound sterling’s relative decline against the U.S. dollar and other major currencies has elevated the value of foreign earnings to companies that have them. Currency cannot take all of the blame, however. Another driver of the decline could be an expectation that UK domestic consumer demand will decline (or at least not grow as fast) as equivalent demand from those abroad.

Safety among British equities may lie in shiny objects. Sectors with greater exposure to commodities have weathered the Brexit storm admirably, particularly the Materials sector, which is up 76% since the referendum. On a more granular level, the Metals & Mining Industry has done particularly well (up 93% since the referendum).

Of course, circumstances can change quickly. The present situation has reminded some commentators of the final quarter of 2008 when, considering a politically divisive “bail out” to stave off financial collapse, the U.S. Congress initially voted against a rescue package. On the day the results become clear, the Dow plunged by over 7%. Shortly thereafter, Congress reversed its initial decision. Whether the UK political establishment will be as sensitive to the market’s concerns, and which scenarios are already “priced in”, remains to be seen. Until then, the indices highlighted in Exhibits 2 and 3 could indicate which way the winds are currently blowing, and where shelter might be found in a storm.

The posts on this blog are opinions, not advice. Please read our Disclaimers.