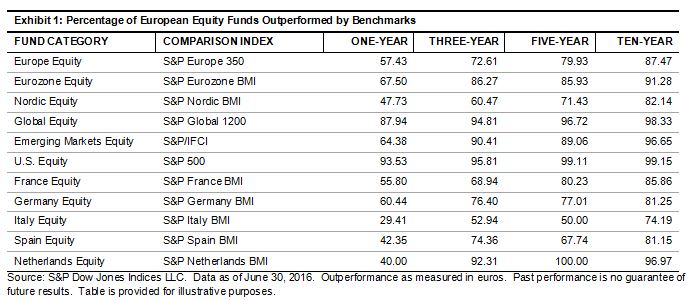

European equity markets fared poorly over the one-year period ending June 30, 2016, with the S&P Europe 350® decreasing 10.47%. This underwhelming performance was brought on by heightened volatility following the U.K.’s vote to exit the European Union, as well as the negative interest rate policy in Europe. Normally, these conditions might be considered ideal for active managers to perform well, but they actually underperformed in most categories analyzed in the SPIVA Europe Mid-Year 2016 report. Overall, about 57% of active fund managers investing in pan-European equities underperformed their benchmark over the one-year horizon ending June 30, 2016 (see Exhibit 1). This statistic deteriorated over the long run, with over 87% of active managers underperforming their benchmark over the 10-year period.

In regard to active funds invested in emerging markets, global equities, and the U.S., the statistics were even starker. Over 98% of active managers investing in global equities lagged their respective benchmark over the 10-year period ending June 30, 2016, and over 96% of active managers invested in emerging market equities trailed their corresponding benchmark over the same period.