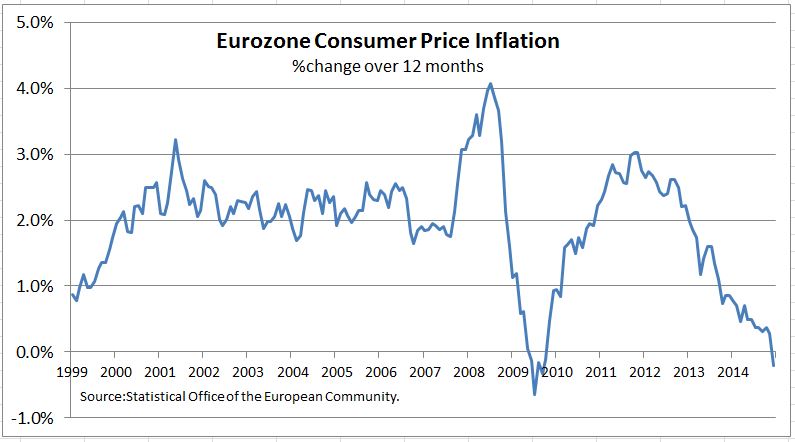

Times have changed: people of a certain age will remember when inflation was investors’ biggest worry, now in Europe the fear is deflation – falling prices. The chart shows the rate of price change in the Eurozone since 2000. It has been falling steadily for over three years. With the December report out yesterday, prices are now falling.

Deflation now is a slow creeping problem rather than an imminent disaster. However, as it continues it will squeeze the economy and shift consumer and business attitudes about spending and investment. If not reversed the damage could be long lasting. Deflation’s principal issues are the impact on debt, on consumer spending and business investment and on the central bank policy.

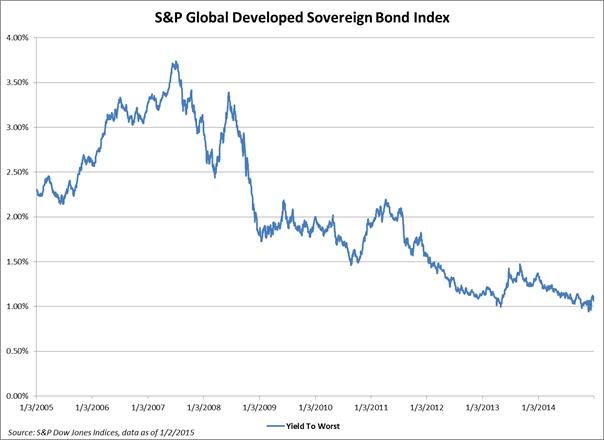

Deflation with its accompanying economic problems is a negative for stocks and is likely to weaken the euro further. The only winners are bond holders – providing the bonds are repaid.

Debt deflation – when prices fall any financial instrument denominated dollars and not adjusted for deflation becomes more valuable. Paying off debts, loans or bonds becomes more difficult as prices fall and their value rises. Businesses cut their prices and revenues fall while the real cost of debt service rises. Only if interest rates could fall below zero could debts adjust for deflation. Debtors face increasing difficulties and potential borrowers are scared away by the high cost of debt. Sectors of the economy where growth depends on credit suffer. Housing would be one of the first hurt.

As prices fall, money becomes more valuable because the same number of dollars buys more. Incentives to spend or invest whither as consumers and business recognize that it is easier and safer to leave money in the bank and watch it appreciate in value. Over time the economy would gradually grind to a halt.

Deflation is also a challenge for the central bank. While prices drift down, advice to the European Central Bank (ECB) is mounting higher and higher. The ECB is expected to implement quantitative easing, but it will face some challenges. First, the supply of bonds is smaller and more diverse than what the Fed bought in the US, making the program harder to implement and its impact harder to gauge. Secondly, Germany may try to block or limit quantitative easing out of fears that it would bailout debtor countries or sow the seeds of future inflation. Hopefully the ECB will move quickly and aggressively – the longer it waits, the worse will be consumer spending and business investment and the harder it will be to make any progress. Even an aggressive QE program may not work in the near term. Chances of successfully reversing deflation and avoiding recession without some fiscal stimulus are limited.

The posts on this blog are opinions, not advice. Please read our Disclaimers.