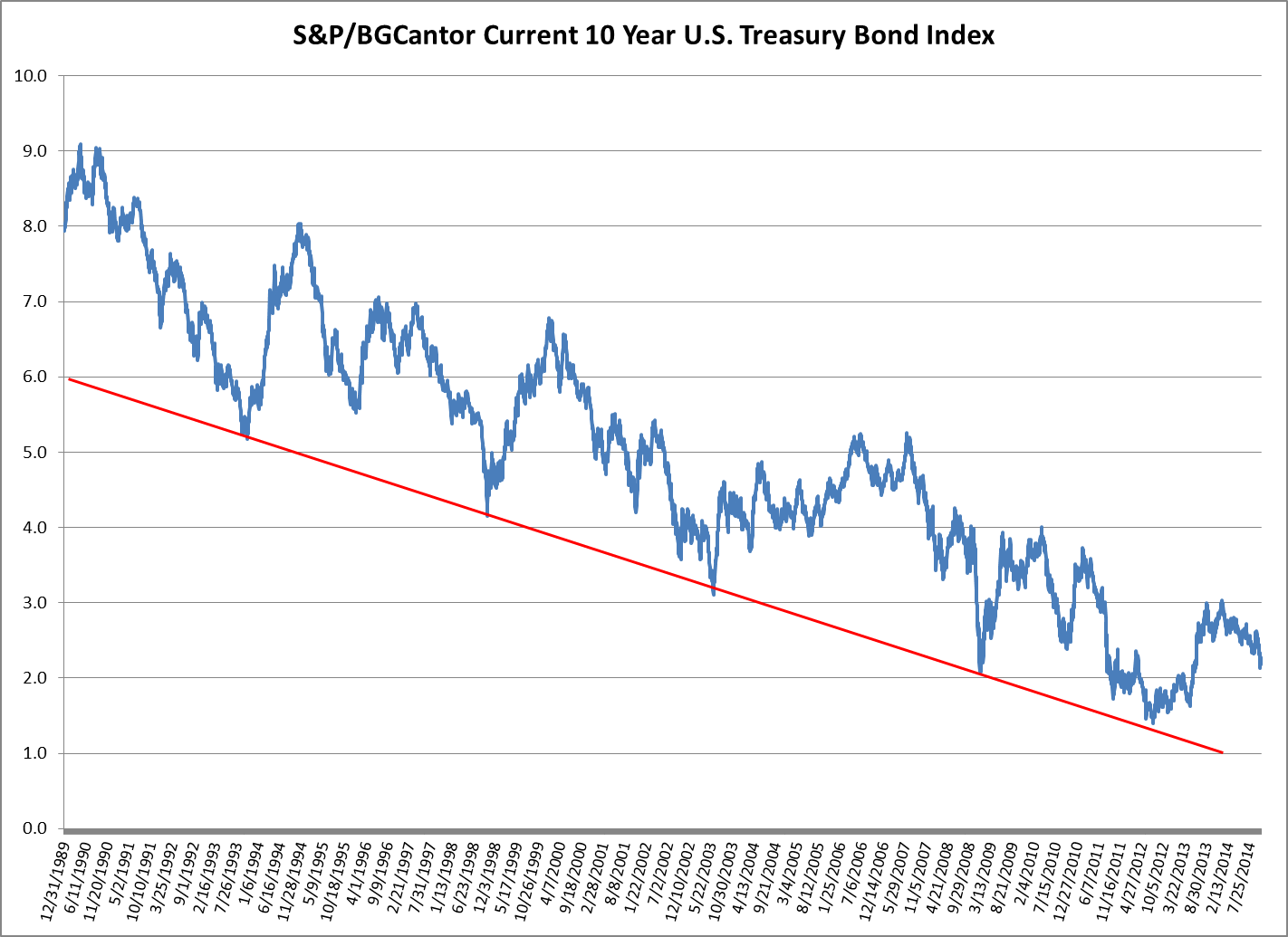

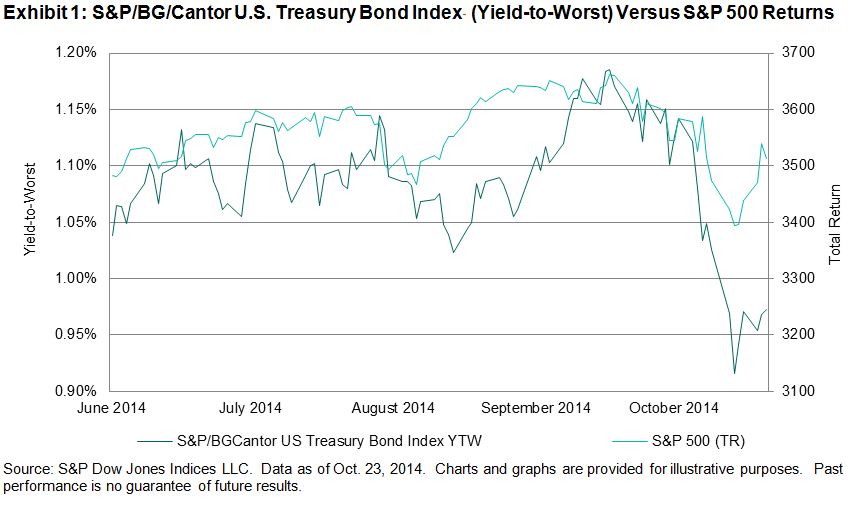

Following in suit with the colors of the trees, investor sentiment appears to be cycling. While the market may not be trading high-yield junk for investment-grade positions as quickly as New Yorkers are trading in their flip-flops and shorts for scarves and umbrellas last week, market demand has shifted in October. The S&P/BGCantor U.S. Treasury Bond Index, which tracks over USD 7 trillion of outstanding treasury debt, responded to October’s equity volatility with investors moving toward quality. Wednesday, Oct. 15, 2014, risk adverse demand drove up the price of T-bonds; bringing yields down to the lowest end-of-day close in over a year, at 0.92% (see Exhibit 1). The shift in tide was not lost on the municipal bond market.

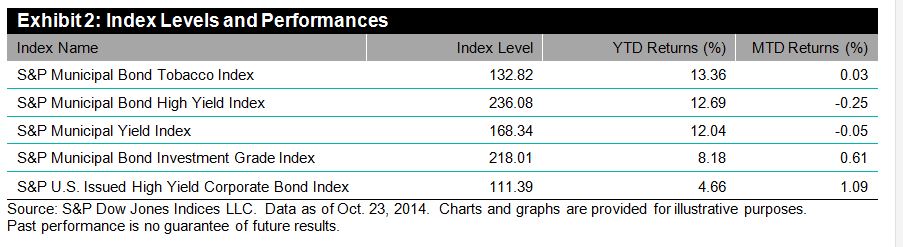

Thus far, 2014 has seen investors clamoring for yields in a low interest and low supply muni market. High-yield munis have outperformed their investment-grade counterparts. Bonds from the Tobacco Master Settlement Agreement of 1998, tracked by the S&P Municipal Bond Tobacco Index have performed outstandingly this year, up 13.36% YTD. However, up to this point of Q3 2014, high-yielding tobacco bonds have remained flat, at 0.03% (see Exhibit 2).

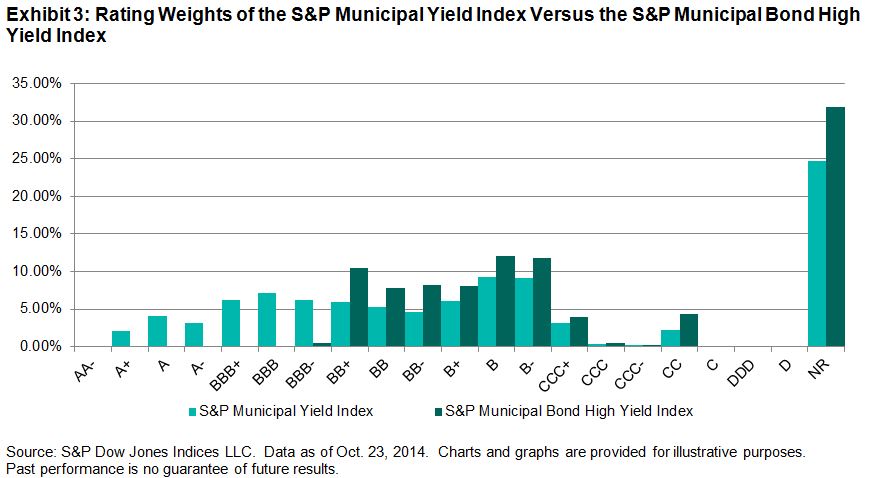

The S&P Municipal Bond High Yield Index, with a 12.69% return YTD, saw returns go the other way in October, down 0.25% for the month after a mild rebound. A similar trend occurred with the S&P Municipal Yield Index, down 12.04% YTD and down 0.05% MTD, although not as dramatically. The S&P Municipal Yield Index implements a weighted investment strategy based on blended quality (see Exhibit3). The S&P Municipal Bond Investment Grade Index only returned 8.18% YTD, yet saw a jump of 0.61% in October.

The S&P 500 has recovered from the drop off from the week of Oct. 13, 2014, and the sun came out this weekend, however the market is far from a consensus on what the future will hold. The municipal bond market has many variables to consider, along with a multitude of viewpoints. On November 5, 2014, S&P Dow Jones Indices will be hosting their annual Municipal Bond Forum live online and in New York. Industry leaders from top Wall Street firms will be debating the central issues and solutions facing both the economy and municipal bond market. For more information, please attend our Third Annual Municipal Bond Forum—Rising Rates? How to Deal With “Maybe”. The event will also be live streamed.

The posts on this blog are opinions, not advice. Please read our Disclaimers.