The SPIVA U.S Scorecard, published twice a year, is a de facto scorekeeper of the active versus passive debate. It measures the performance of the actively managed domestic equity funds across the various market capitalizations and styles. The results for the 2014 mid-year Scorecard are in and reveal very few surprises. Here are some of the key findings:

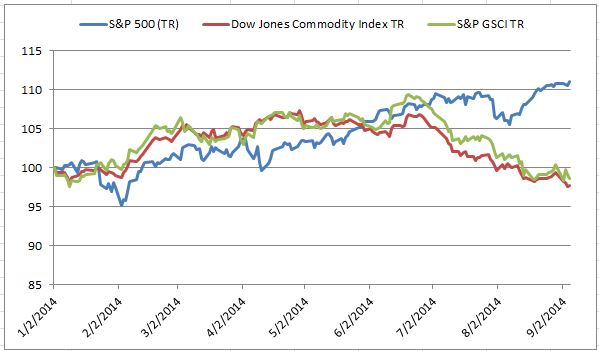

- The past 12 months have been quite a bullish ride for the domestic equity markets. The S&P 500®, S&P MidCap 400® and S&P SmallCap 600® returned 24.61%, 25.24% and 25.54%, respectively. During the same period, 59.78% of large-cap managers, 57.84% of mid-cap managers and 72.79% of small-cap managers underperformed the above-mentioned benchmarks.

- The past five years have been marked by the rare combination of a remarkable rebound in domestic equity markets and a low-volatility equity environment. Against that backdrop, over 75% of them across all capitalization and style categories failed to deliver returns higher than their respective benchmarks.

- On the international front, approximately 70% of global equity funds, 75% of international equity funds, 81% of international small-cap funds and 65% of emerging market funds underperformed their benchmarks over the past one year.

- For the first time since adding the International Equity category to the Scorecard, the report witnessed the majority of the international small cap managers underperforming the benchmark. The outcome was slightly more favorable when viewed over three- and five-year horizons, as over 50% of managers outperformed the benchmark.

The results unequivocally show the effectiveness of indexing in the U.S equity market. Together with the Persistence Scorecard, the results highlight that not only it is extremely difficult for active funds to outperform the benchmarks, it is near impossible to find that skillful manager who can effectively do so consistently year after year.

The posts on this blog are opinions, not advice. Please read our Disclaimers.