After having risen 19 basis points the first week of July, the yield on the S&P/BGCantor Current 10 Year U.S. Treasury Bond Index dropped 20 basis points from the July 3rd 2.72% to its current 2.52%, offsetting the initial increase. The move up in yield to start July was the largest weekly jump since last August (8/16/2013), while last week’s rally moving yields downward was the largest weekly move in yield since a 31 basis point rally back on June 1st of 2012. Last week also brought news that the Fed plans to end its tapering activity by October of this year.

Not quite out of the news headlines yet, Puerto Rican municipal bond yields are at 8.13%, right where they began the week, as measured by the S&P Municipal Bond Puerto Rico Index. Performance of this index year-to-date has returned 0.43% after being as high as 10.65% on May 30th. Performance for the month the index is down -5.2%. The yield of the broader S&P Municipal Bond Index also remained unchanged on the week at a 2.67% though unlike Puerto Rico, the broad index is returning 5.59% year-to-date.

Investment grade bonds as measured by the S&P U.S. Issued Investment Grade Corporate Bond Index turned it up a notch as the index’s yield tightened by 9 basis points on the week to a 2.76%. Year-to-date this index is now returning more than its high yield counterpart with a year-to-date return of 5.68%. Last week’s performance added 0.81%, more than enough to offset the prior week’s negative 0.61% that started July.

As mentioned, the S&P U.S. Issued High Yield Corporate Bond Index has returned 5.38% year-to-date. Last week the index gave up 0.12% for total return after a relatively flat prior week and a string of positive weekly performance since March of this year. While the yield of the investment grade index moved down by 9 basis points last week, the yield of the high yield index moved the same 9 basis points but upward to a 5.04%.

Continuing to yield 4.34%, the S&P/LSTA U.S. Leveraged Loan 100 Index has returned +0.08% month-to-date while the similar credit of high yield was down -0.15%. Year-to-date the senior loan index has returned 2.56%.

The S&P U.S. Preferred Stock Index’stotal return is up 0.55% on the month while equities as measured by the S&P 500®are returning a very close 0.45%. Year-to-date total return performance is not even close as preferreds are outperforming the equity markets returning a total return of 11.64% compared to the equity markets total return of 7.62%

There are no Monday economic releases for this week, but the rest of the calendar should pack a punch. As the strength of the recovery is still in question, Tuesday’s release of the Empire Manufacturing Survey (17 expected, 19.28 prior) along with the June month-over-month Advance Retail Sales (0.6%exp., 0.3% prior) should shed some insight to the debate. The June Import Price Index (0.4% exp) is also set to be released for Tuesday. MBA Mortgage Applications (1.9% prior) along with June’s PPI (Producer Price Index (0.2% exp., -0.2% prior) and Industrial Production (0.3% exp., 0.6% prior) will make for a busy Wednesday. After the “hump-day”, Housing Starts (1020k exp.), Initial Jobless Claims (310k exp., 304k prior) and the Philadelphia Fed Business Outlook (16 vs. 17.8 prior) will follow. The week will close with the release of both the University of Michigan Confidence number (83 exp. vs. 82.5 prior) and the Conference Board of U.S. Leading Index which is expected to be unchanged from its prior release at a 0.5%. The Leading Index gives an indication of the future state of the economy.

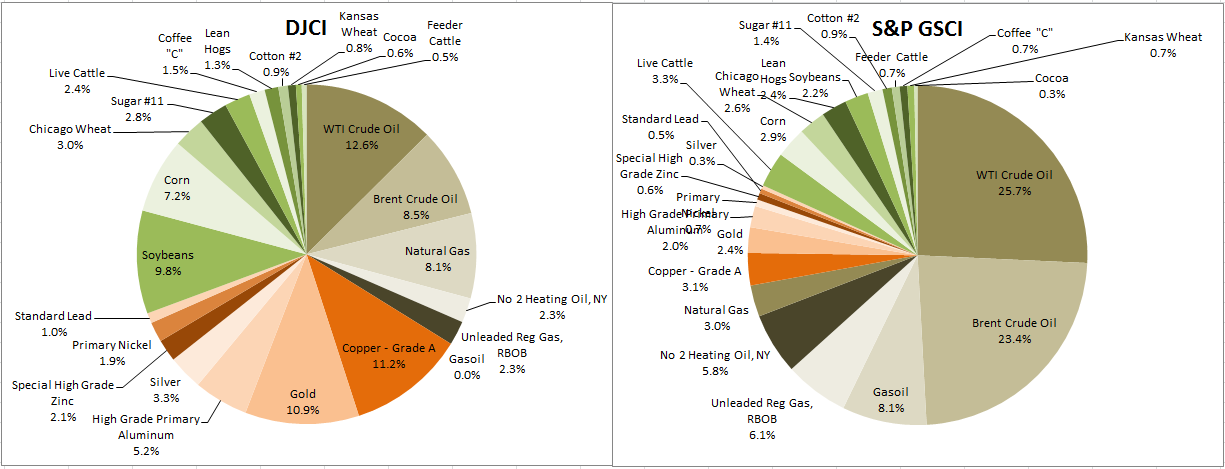

Source: S&P Dow Jones Indices, Data as of 7/11/2014, Leveraged Loan data as of 7/13/2014.

The posts on this blog are opinions, not advice. Please read our Disclaimers.