Last month, as in many this year, the majority of developed markets eked out respectable gains. The S&P 500® closed May at a new high, as did the S&P Global 1200 index of worldwide large cap equities. The S&P Europe 350 nudged up to levels not seen since 2007. All would appear to be going well.

Nonetheless, such calm markets prove fertile ground for speculation. Particularly of note is a swathe of articles and commentary pointing out that implied volatility (measured, for example, by the VIX) is low, and options prices are very, very low. Have the actions of central bankers made the equity markets become complacent? Or is the VIX somehow “broken?”

The first question is beyond us. We just don’t know if the average investor is currently guilty of irrational exuberance, and we would be suspicious of anyone who claimed to know just how exuberant we should be. Forecasting is no easier now than eighty years ago.

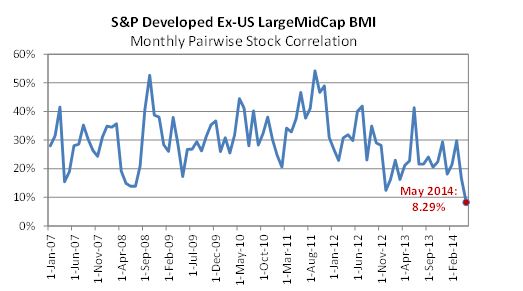

Most of the investors I’ve spoken to recently are in fact rather worried about what’s next, but there’s a wide spread of opinions as to what one’s primary worry should be. That speaks – perhaps – to a decrease in correlations as much as to a decrease in volatility. And there’s certainly evidence to support this, notably from an ex-U.S. perspective:

Source: S&P Dow Jones Indices Correlation & Dispersion Index Dashboard, June 2nd 2014

One of the features of volatility (measured at the level of whole markets) is that it’s very dependent on correlation, although the relationship is subtle. If stocks move independently, their aggregate impact on the market is diminished. If stocks move together, the market whips around with their combined movement.

As we’ve noted before, it is entirely possible that correlations will spike up in response to a macroeconomic crisis event. In the meantime, however, the prevalently low correlations are providing diversified investors with an unusually smooth ride.

The posts on this blog are opinions, not advice. Please read our Disclaimers.