Harbouring year-end reviews and final accounts, the last weeks of December are infused with nostalgia. In this seasonal spirit, I’d like to draw your attention to an under-celebrated piece of work, completed in the year that Katharine Hepburn, Cary Grant and Shirley Temple saw their debuts on the silver screen. In 1932, Fred had not yet met Ginger, ground had just been broken on the Golden Gate Bridge, and on New Year’s Eve, a joint meeting of the Econometric Society and the American Statistical Association considered the results of an inquiry that opened the debate between active and passive management.

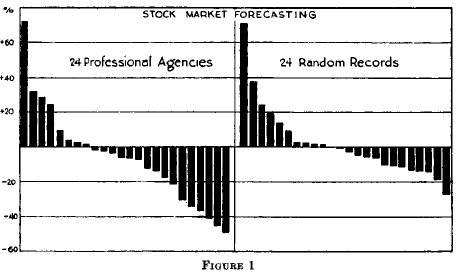

The question “Can Stock Market Forecasters Forecast?” is a natural one to ask. The economist Alfred Cowles III was probably the first to investigate this question empirically. In July 1927, he began collecting information on the equity investments made by financial institutions of the time as well as on the recommendations made by various “oracles” in contemporary financial media, embarking on a multi-year project to record and evaluate their performance. It was a heroic effort: over 7,500 recommendations and transactions tracked and tabulated, against hundreds of stocks prices and dividends collected by hand over 4 ½ years.

Importantly, Cowles didn’t just measure absolute performance. He also compared the returns to what “the market averages” (in his case, the Dow Jones Industrial Average) would have achieved. Using fairly modern statistical techniques1 combined with meticulously hand-drawn charts, Cowles expertly diagnosed contemporary active management: poor on average; appearing skilful most probably through sheer luck.

Source: Cowles ; “Can Stock Market Forecasters Forecast?” ; Econometrica, Volume 1 Issue 3 (1933)

Cowles presented his research on December 31st, rounding off a year in which he also established the Cowles Commission for Research in Economics, subsequently to become a veritable breeding ground for Nobel-prize winning ideas (Robert Shiller’s being the most recently recognised).

And his comparison of stock selection strategies to market averages and random portfolios is thoroughly modern. With almost identical methods and conclusions2, the progeny of Cowles’ research continue to stimulate debate.

_______________________________________________

- Cowles’ ideas are considerably ahead of their time. His use of playing cards to simulate random portfolios is a more than a decade prior to Stanislaw Ulam’s & Von Neuman’s celebrated first use of the “Monte Carlo” method at Los Alamos in work relating to the development of the hydrogen bomb.

- Today a market-cap weighted benchmark is usually seen as the bogey, but it would be more than 30 years before William F. Sharpe explained why.