Effective prior to the market open on Sept. 24, 2018, the Telecommunication Services sector will be replaced with a new Communication Services sector, which will combine telecom with parts of the Information Technology and Consumer Discretionary sectors.

As a result, Telecom, the ugly duckling sector comprising three stodgy telephone companies, will now be joined by companies including Alphabet, Facebook, and Netflix. Given the addition of these younger juggernauts in the social media space, one might assume that the volatility of the new Communication Services sector would skyrocket. However, this is paradoxically not the case, and we can understand why using the lens of dispersion and correlation.

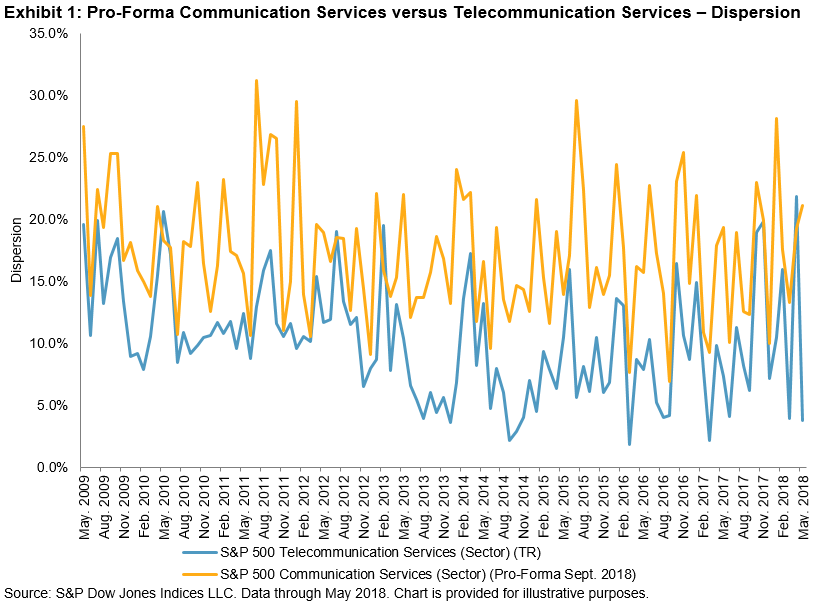

When comparing pro-forma indices with their current counterparts, we find that Consumer Discretionary and Info Tech’s historical dispersion and correlation levels are about the same. But when we look at Telecom versus the pro-forma Communication Services sector, as seen in Exhibit 1, we discover that the dispersion of Communication Services is consistently higher than that of Telecom. This is not a surprising outcome, given that the number of constituents increases from the current three and includes such names as Alphabet and Facebook, which have little in common with traditional telephone utilities.

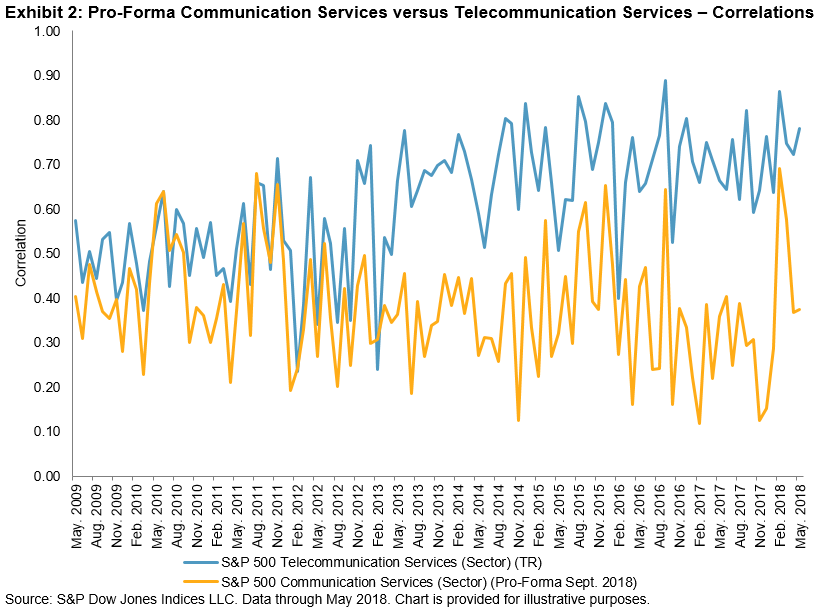

Moreover, as seen in Exhibit 2, the correlation of Communication Services is generally lower than that of Telecom. This result is again not surprising, given the fundamental differences between phone companies and the new names coming into the new sector.

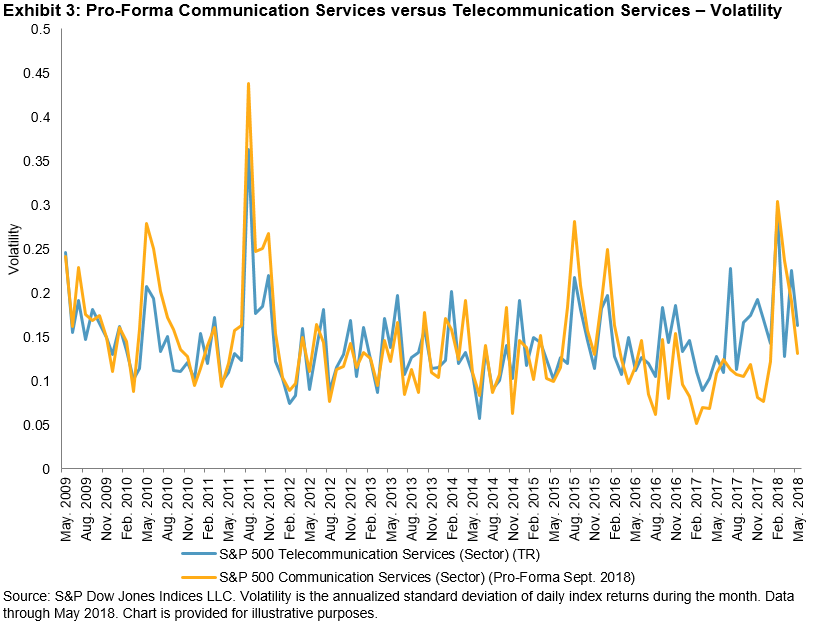

These findings have important implications for how the volatility of pro-forma Communication Services compares with that of Telecom, as volatility manifests itself in both dispersion and correlation. As shown by Exhibit 3, over time, the volatility of pro-forma Communication Services is roughly equal to that of Telecom. This results from the juxtaposition of two opposing forces: Communication Services’ higher dispersion, which drives volatility higher, is balanced by its lower correlations, which pull volatility lower. This is indeed an unexpected and notable outcome.