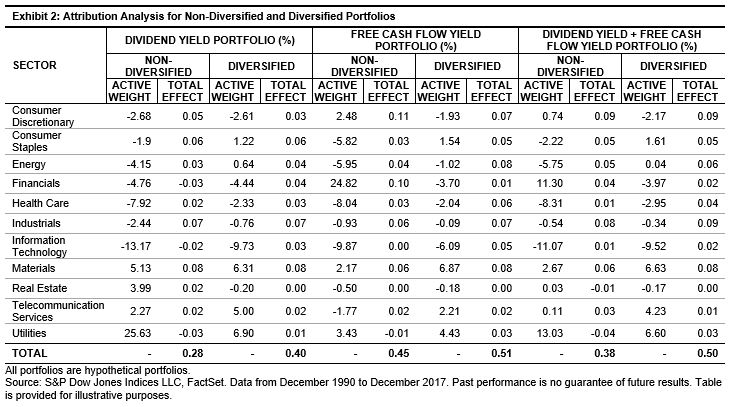

In recent years, the term “risk parity” has become a catch-all phrase to describe strategies that attempt to allocate based on risk. The launch of the S&P Risk Parity Indices last week is a testament to the proliferation and the popularity of the style. As we noted in a prior blog, there is a lack of proper benchmarks to measure the effectiveness of such strategies.

Therefore, it is worthwhile to take a step back and examine the empirical basis that gives rise to risk parity strategies (i.e., the notion of equal risk contribution). From there, we can dive deeper into the properties of risk parity strategies and the characteristics that one should be mindful of.

As a starting point, we looked at the historical correlations between different asset classes (see Exhibit 1).[1] [2] [3]

For the 18-year period, there were strong positive correlations between the equity regions, ranging from 0.75 to 0.87. Additionally, equities had moderately positive correlations to real estate, commodities, and high yield bonds. However, in contrast, equities were negatively correlated with investment grade bonds, which implies that adding investment grade bonds, particularly to an equity portfolio, could lower portfolio volatility and potentially deliver higher returns per unit of risk.

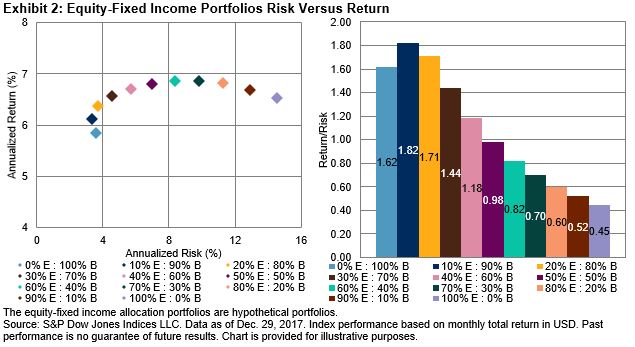

To evaluate the effect that asset-pair correlations have on portfolio volatility, we constructed a two-asset portfolio consisting of U.S. equity and investment grade bonds. In addition to the classic 60/40 equity/bond mix, additional portfolios were created in 10% weight increments, resulting in 11 total portfolios.

Equities outperformed bonds over the 18-year period, but that excess performance came with significantly higher volatility (left chart). The risk-adjusted return ratios (right chart) show the return per unit of risk for each portfolio—bonds had a significantly higher risk-adjusted ratio of 1.62 versus 0.45 for equities. Thus, on a risk efficiency basis, bonds fared better than equities. Given the low correlations and higher risk-adjusted return ratio for bonds, combining the two assets led to several allocation mixes with even higher risk-adjusted ratios (e.g., 10/90 equity/bond and 20/80 equity/bond). In fact, the 10/90 equity/bond portfolio had lower volatility relative to bonds along with higher returns—this led to the highest risk-adjusted return ratio (1.82) out of all the mixes. Starting from an initial 100/0 equity/bond portfolio and progressively increasing weight to bonds led to higher absolute returns (until 60/40) and higher risk-adjusted return ratios (until 10/90). These results show how effective combining low-correlated assets together in a portfolio could be.

In a future post, we will review the contribution to total risk of selected portfolio mixes, as the contribution to total portfolio risk for each asset class can be expected to be different from their portfolio weights.

[1] Markowitz, H. “Portfolio Selection.” The Journal of Finance, Vol. 7, No. 1. (March 1952), pp. 77-91.

[2] Modern Portfolio Theory states that non-perfect correlations between different assets underpins the notion of portfolio diversification—whereby increased diversification results in higher returns for a given level of risk.

[3] The S&P 500 represented U.S. Equities, the S&P Developed Ex.-U.S. BMI represented International Equities, the S&P Emerging BMI represented Emerging Market Equities, the Dow Jones U.S. Real Estate Index represented Real Estate, the Dow Jones Commodity Index represented Commodities, the S&P U.S. Treasury Bond Index represented Investment Grade Bonds from Dec. 31, 1999, to April 30, 2002, and then it was represented by the S&P U.S. Aggregate Bond Index, the S&P U.S. High Yield Corporate Bond Index represented High Yield Bonds, and the S&P Global Developed Sovereign Ex-US Bond Index represented International Sovereign Bonds.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

Source: S&P Dow Jones Indices

Source: S&P Dow Jones Indices